1. What is the projected Compound Annual Growth Rate (CAGR) of the Car DVD Player?

The projected CAGR is approximately 3.6%.

Car DVD Player

Car DVD PlayerCar DVD Player by Type (Car Headrest DVD Player, Overhead DVD Players, Others, World Car DVD Player Production ), by Application (Passenger Car, Commercial Car, World Car DVD Player Production ), by North America (United States, Canada, Mexico), by South America (Brazil, Argentina, Rest of South America), by Europe (United Kingdom, Germany, France, Italy, Spain, Russia, Benelux, Nordics, Rest of Europe), by Middle East & Africa (Turkey, Israel, GCC, North Africa, South Africa, Rest of Middle East & Africa), by Asia Pacific (China, India, Japan, South Korea, ASEAN, Oceania, Rest of Asia Pacific) Forecast 2026-2034

MR Forecast provides premium market intelligence on deep technologies that can cause a high level of disruption in the market within the next few years. When it comes to doing market viability analyses for technologies at very early phases of development, MR Forecast is second to none. What sets us apart is our set of market estimates based on secondary research data, which in turn gets validated through primary research by key companies in the target market and other stakeholders. It only covers technologies pertaining to Healthcare, IT, big data analysis, block chain technology, Artificial Intelligence (AI), Machine Learning (ML), Internet of Things (IoT), Energy & Power, Automobile, Agriculture, Electronics, Chemical & Materials, Machinery & Equipment's, Consumer Goods, and many others at MR Forecast. Market: The market section introduces the industry to readers, including an overview, business dynamics, competitive benchmarking, and firms' profiles. This enables readers to make decisions on market entry, expansion, and exit in certain nations, regions, or worldwide. Application: We give painstaking attention to the study of every product and technology, along with its use case and user categories, under our research solutions. From here on, the process delivers accurate market estimates and forecasts apart from the best and most meaningful insights.

Products generically come under this phrase and may imply any number of goods, components, materials, technology, or any combination thereof. Any business that wants to push an innovative agenda needs data on product definitions, pricing analysis, benchmarking and roadmaps on technology, demand analysis, and patents. Our research papers contain all that and much more in a depth that makes them incredibly actionable. Products broadly encompass a wide range of goods, components, materials, technologies, or any combination thereof. For businesses aiming to advance an innovative agenda, access to comprehensive data on product definitions, pricing analysis, benchmarking, technological roadmaps, demand analysis, and patents is essential. Our research papers provide in-depth insights into these areas and more, equipping organizations with actionable information that can drive strategic decision-making and enhance competitive positioning in the market.

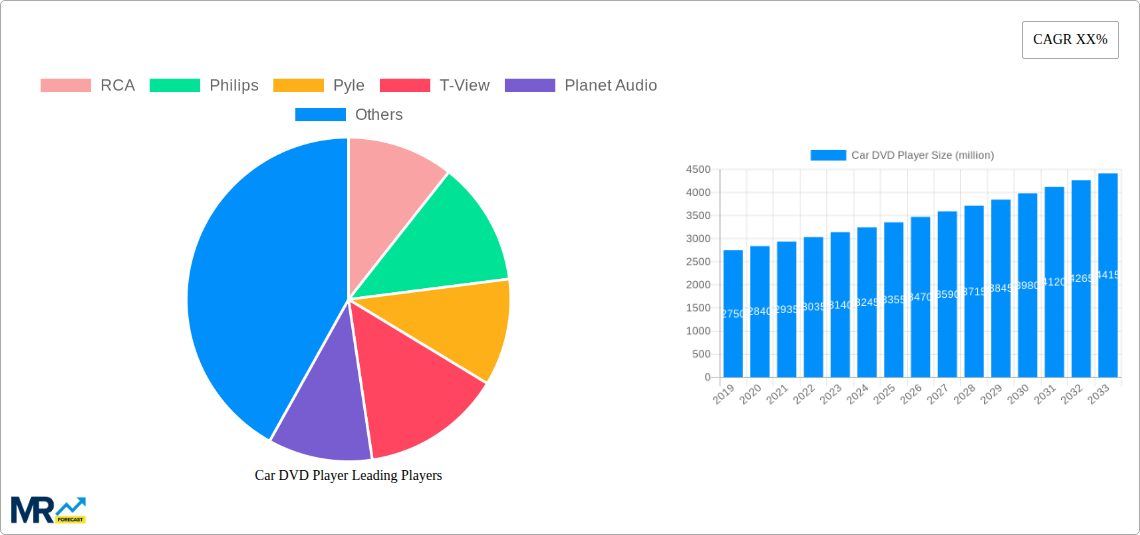

The global car DVD player market, while facing decline due to the rise of integrated infotainment systems and smartphones, still holds a niche market segment. The market size in 2025 is estimated at $250 million, reflecting a steady contraction from its peak years. This decline is primarily driven by the increasing prevalence of in-car entertainment solutions that are built directly into the vehicle's dashboard, offering superior functionality and integration. However, the demand for affordable aftermarket entertainment options, particularly in emerging markets, continues to provide some level of support. Factors such as cost-effectiveness compared to integrated systems and the ability to utilize existing car stereos contribute to this remaining demand. The market is segmented by product type (headrest, overhead, and others), application (passenger and commercial vehicles), and geography. Headrest DVD players remain the dominant segment due to their ease of installation and affordability. The Asia-Pacific region, particularly China and India, continues to show relatively stronger performance due to higher volumes of older vehicle sales and a larger price-sensitive consumer base. While the overall market displays a negative CAGR (let's assume -5% for this analysis), growth potential is observable in regions with a large existing fleet of older vehicles and a developing consumer market. Key players like RCA, Philips, and others focus on price competitiveness and improved features to maintain their market share. The future outlook for the market indicates continued contraction, with a gradual shift towards specialized applications, such as commercial vehicles where dedicated entertainment systems might still be preferred for larger fleets or long-distance haulage. This niche segment will likely be driven by innovation in durability and reliability, rather than technological advancements.

The competitive landscape is fragmented, with numerous players vying for market share. Established brands leverage their brand recognition and distribution networks, while newer companies compete based on price and innovative designs. The success of these players hinges on their ability to cater to specific needs within the niche market, understanding price sensitivity in developing markets and delivering cost-effective and reliable products. The focus on improving durability and reliability to mitigate maintenance costs becomes key for commercial applications. Regulatory changes concerning in-car electronics and safety standards in various regions will also impact market growth. Companies that adapt to the shifting landscape and meet the specific requirements of their target segments are most likely to succeed in this evolving market.

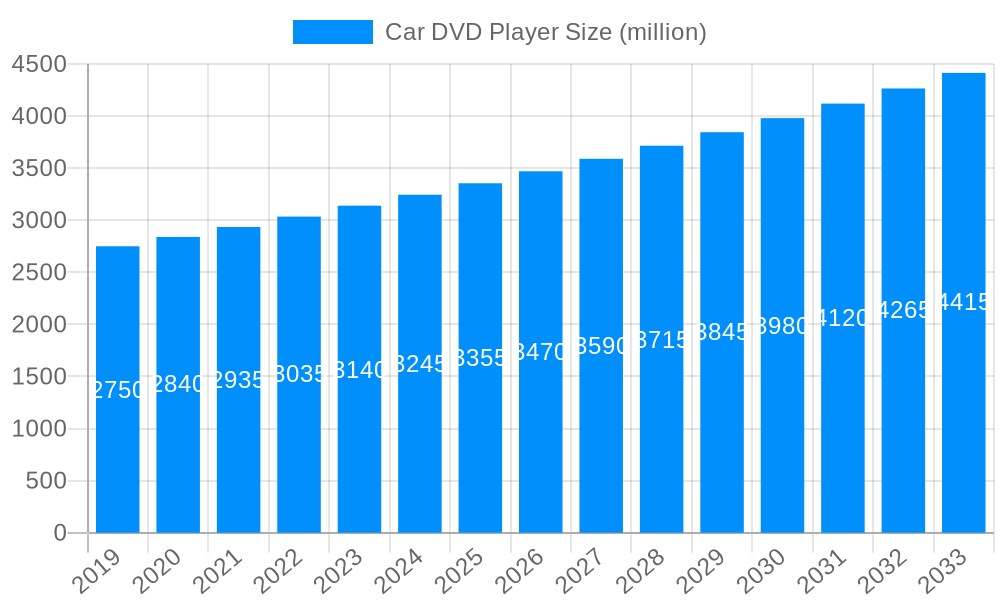

The global car DVD player market, while facing headwinds from the rise of streaming and integrated infotainment systems, continues to exhibit nuanced growth patterns. The study period from 2019 to 2033 reveals a complex market dynamic. While overall unit sales might not reach the astronomical figures seen in previous decades (peaking in the early 2010s at several tens of millions of units annually), certain segments and regions are showing surprising resilience. The historical period (2019-2024) witnessed a decline in overall production, primarily driven by the aforementioned technological shifts. However, the estimated year (2025) shows stabilization, indicating a leveling-off rather than a complete market collapse. The forecast period (2025-2033) projects modest growth, fueled largely by specific applications and geographical locations. This growth is not uniform; it's shaped by factors like affordability, reliability, and the persistent demand for dedicated entertainment solutions, particularly in emerging markets and for specific vehicle types. The millions of units sold annually during the peak years have significantly decreased, but a steady, albeit smaller, market segment continues to purchase these players for various reasons, from cost-effectiveness to the perceived reliability of physical media over streaming services in certain areas. The market is segmented not just by type (headrest, overhead, others) but also by application (passenger cars, commercial vehicles), creating a more intricate understanding of its ongoing evolution. This report delves into these specific trends, offering a granular picture of the car DVD player landscape.

Several factors continue to support the car DVD player market, albeit on a smaller scale than in the past. In developing nations and regions with limited or unreliable internet access, DVD players remain a cost-effective and reliable solution for in-car entertainment. The affordability of DVD players compared to integrated infotainment systems, especially in the used car market and for budget-conscious buyers, sustains demand. Furthermore, the robustness of DVD technology against network disruptions and data limitations makes it a dependable choice, especially for long journeys or areas with poor connectivity. The availability of a vast library of pre-recorded content, including children's programming and movies, continues to be a major draw for families. Specific segments like car headrest DVD players remain popular due to their ability to provide individual entertainment to rear passengers, minimizing distractions for the driver. These elements, while not generating the same high volume sales as in the past, contribute to a niche but sustainable market share for car DVD players. Finally, some commercial vehicle operators still prefer the simplicity and reliability of DVD players over more complex systems.

The primary challenge facing the car DVD player market is the overwhelming dominance of integrated infotainment systems and the rise of streaming services. Modern vehicles increasingly incorporate built-in screens with smartphone integration and access to streaming platforms like Netflix and Spotify. This integrated approach offers a more seamless user experience, often superior audio and video quality, and the convenience of on-demand content. The cost advantage of DVD players is diminishing as the price of integrated systems continues to fall. Furthermore, the technological gap is widening, with newer vehicles featuring significantly better screen resolution and functionality compared to even the latest DVD player models. The ongoing shift to digital distribution of content also weakens the appeal of physical media. The increasing focus on driver safety further reduces the market for distracting entertainment systems, especially if those lack modern safety features. These factors combine to exert considerable downward pressure on the car DVD player market.

Analyzing the car DVD player market reveals that certain segments and geographical regions are more resilient than others. While precise sales figures fluctuate based on many variables, the following patterns are observed across the study period (2019-2033):

Passenger Car Segment Dominance: The passenger car segment will continue to account for the vast majority of car DVD player sales globally. Commercial vehicles may have specific niche needs, but the sheer volume of passenger vehicles on the road ensures that this segment remains the primary driver of market growth, albeit at a reduced scale compared to peak years.

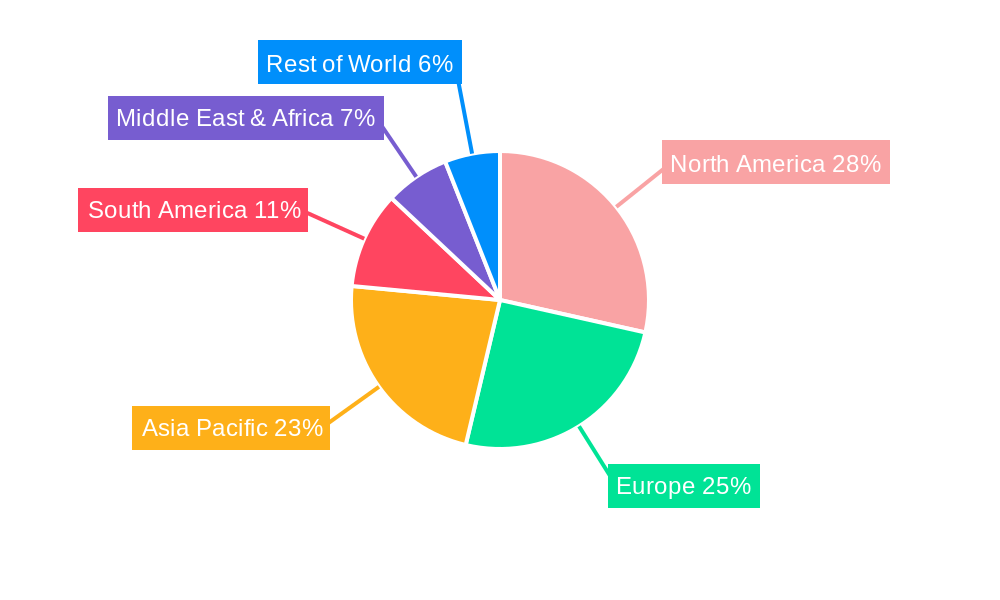

Emerging Markets: Developing economies and regions in Asia, Africa, and parts of Latin America continue to show a higher demand for car DVD players than mature markets. The factors cited earlier – affordability, reliability, and limited internet access – are crucial in these regions. This demand ensures a steady, albeit potentially smaller, volume of sales persists into the forecast period.

Car Headrest DVD Players: The preference for individual entertainment in the back seats for children and other passengers supports the sustained demand for headrest DVD players. Their modular nature and relative ease of integration (compared to full overhead units) contribute to their continued popularity.

In terms of specific countries, there isn’t a single dominant player in the way there might have been in previous years. However, countries in Southeast Asia and parts of Africa, where affordability and reliability of technology are paramount, offer significant market potential for car DVD players, though these sales figures are unlikely to reach the millions of units sold annually in prior years. The sheer size of these markets means that even a small market penetration translates into a noticeable overall volume. Conversely, mature markets like North America and Europe are witnessing a continued decline in sales, although the previously mentioned niche applications (e.g., used car sales) will continue to support minimal, steady sales.

Several factors could influence future growth in this sector. Continued innovation within the car DVD player industry, focusing on improved screen resolution, enhanced audio quality, and greater integration with modern vehicle systems, could attract new customers. A continued focus on affordability remains paramount for maintaining market share in developing regions. Furthermore, creating products that are more easily integrated with existing vehicles could help capture a segment of the aftermarket.

This report provides a detailed analysis of the car DVD player market, covering historical data, current trends, and future projections. It explores the market's various segments, key players, and geographical regions. The report aims to offer insights into the factors driving market growth, challenges hindering its progress, and opportunities for future development. It aims to deliver a comprehensive understanding of this evolving niche market segment.

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 3.6% from 2020-2034 |

| Segmentation |

|

Note*: In applicable scenarios

Primary Research

Secondary Research

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence

The projected CAGR is approximately 3.6%.

Key companies in the market include RCA, Philips, Pyle, T-View, Planet Audio, VOXX Electronics, Power Acoustik, Ematic, XTRONS, Epsilon Electronics, AAMP Global, XO Vision, Alpine, Rockville Audio, .

The market segments include Type, Application.

The market size is estimated to be USD 1.8 billion as of 2022.

N/A

N/A

N/A

N/A

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4480.00, USD 6720.00, and USD 8960.00 respectively.

The market size is provided in terms of value, measured in billion and volume, measured in K.

Yes, the market keyword associated with the report is "Car DVD Player," which aids in identifying and referencing the specific market segment covered.

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

To stay informed about further developments, trends, and reports in the Car DVD Player, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.