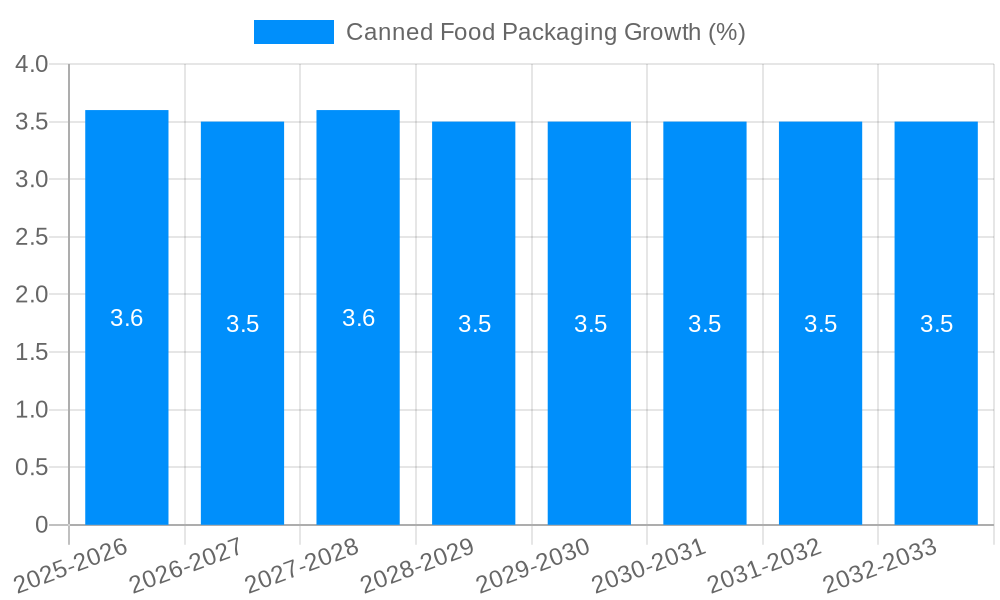

1. What is the projected Compound Annual Growth Rate (CAGR) of the Canned Food Packaging?

The projected CAGR is approximately XX%.

MR Forecast provides premium market intelligence on deep technologies that can cause a high level of disruption in the market within the next few years. When it comes to doing market viability analyses for technologies at very early phases of development, MR Forecast is second to none. What sets us apart is our set of market estimates based on secondary research data, which in turn gets validated through primary research by key companies in the target market and other stakeholders. It only covers technologies pertaining to Healthcare, IT, big data analysis, block chain technology, Artificial Intelligence (AI), Machine Learning (ML), Internet of Things (IoT), Energy & Power, Automobile, Agriculture, Electronics, Chemical & Materials, Machinery & Equipment's, Consumer Goods, and many others at MR Forecast. Market: The market section introduces the industry to readers, including an overview, business dynamics, competitive benchmarking, and firms' profiles. This enables readers to make decisions on market entry, expansion, and exit in certain nations, regions, or worldwide. Application: We give painstaking attention to the study of every product and technology, along with its use case and user categories, under our research solutions. From here on, the process delivers accurate market estimates and forecasts apart from the best and most meaningful insights.

Products generically come under this phrase and may imply any number of goods, components, materials, technology, or any combination thereof. Any business that wants to push an innovative agenda needs data on product definitions, pricing analysis, benchmarking and roadmaps on technology, demand analysis, and patents. Our research papers contain all that and much more in a depth that makes them incredibly actionable. Products broadly encompass a wide range of goods, components, materials, technologies, or any combination thereof. For businesses aiming to advance an innovative agenda, access to comprehensive data on product definitions, pricing analysis, benchmarking, technological roadmaps, demand analysis, and patents is essential. Our research papers provide in-depth insights into these areas and more, equipping organizations with actionable information that can drive strategic decision-making and enhance competitive positioning in the market.

Canned Food Packaging

Canned Food PackagingCanned Food Packaging by Type (Metal, Steel, Aluminum, Others), by Application (Readymade Meals, Meat, Sea Food, Others), by North America (United States, Canada, Mexico), by South America (Brazil, Argentina, Rest of South America), by Europe (United Kingdom, Germany, France, Italy, Spain, Russia, Benelux, Nordics, Rest of Europe), by Middle East & Africa (Turkey, Israel, GCC, North Africa, South Africa, Rest of Middle East & Africa), by Asia Pacific (China, India, Japan, South Korea, ASEAN, Oceania, Rest of Asia Pacific) Forecast 2025-2033

The global Canned Food Packaging market is projected for significant expansion, reaching an estimated value of $XXX million in 2025 and experiencing a robust Compound Annual Growth Rate (CAGR) of XX% through 2033. This growth is propelled by a confluence of factors, including the increasing demand for convenient and shelf-stable food options, particularly among busy urban populations and developing economies. The inherent advantages of canned packaging, such as its durability, extended shelf life, and protection against spoilage and contamination, continue to resonate with consumers and manufacturers alike. Furthermore, innovations in canning technology, leading to lighter materials, improved aesthetics, and enhanced product safety, are contributing to market momentum. The rising popularity of ready-to-eat meals, canned seafood, and other processed food categories is directly fueling the need for reliable and cost-effective packaging solutions.

The market is characterized by a dynamic interplay of drivers and restraints. Key growth drivers include the escalating global population, a growing middle class with increased disposable income, and the persistent trend towards processed and convenience foods. The expansion of retail infrastructure, especially in emerging markets, also plays a crucial role in making canned goods more accessible. However, certain restraints temper this growth. Environmental concerns regarding the recyclability and disposal of metal cans, coupled with the increasing preference for sustainable packaging alternatives like flexible pouches and glass, pose a challenge. Fluctuations in raw material prices, particularly for steel and aluminum, can also impact profitability and market competitiveness. Despite these challenges, the enduring appeal of canned food packaging, driven by its practicality and affordability, ensures its continued relevance and substantial market presence in the foreseeable future.

Here's a unique report description on Canned Food Packaging, incorporating your specified headings, word counts, values in millions, and company/segment information.

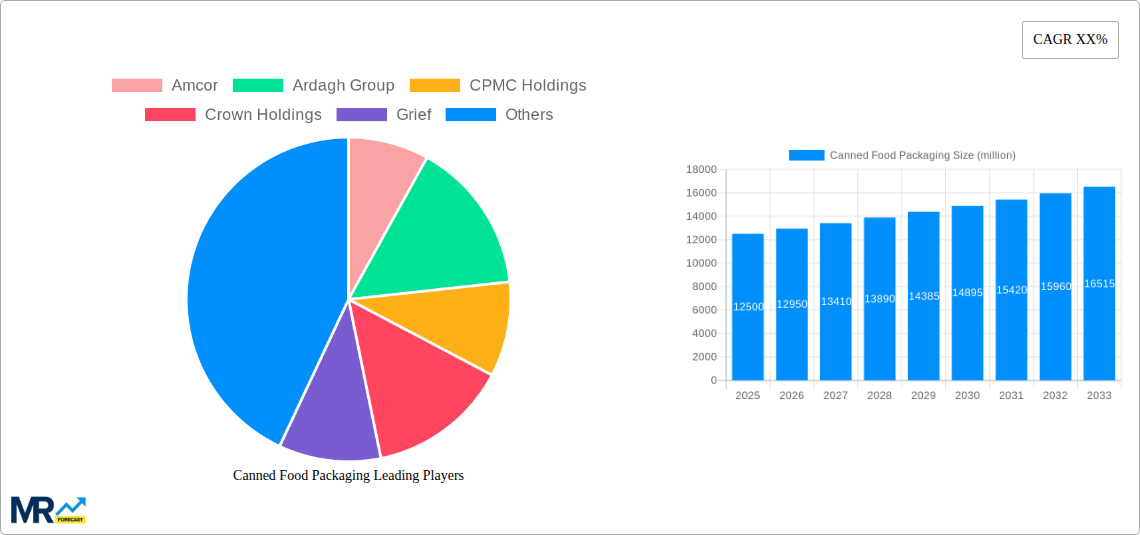

The global canned food packaging market, valued at an estimated 125,500 million units in the base year of 2025, is undergoing a dynamic transformation driven by evolving consumer preferences, technological advancements, and a growing emphasis on sustainability. During the historical period from 2019-2024, the market witnessed steady growth, primarily fueled by the convenience and extended shelf-life offered by canned goods. The study period from 2019-2033 is expected to see continued expansion, with the forecast period of 2025-2033 projecting robust CAGR. A significant trend observed is the increasing demand for innovative packaging designs that enhance consumer appeal and functionality. This includes the introduction of easy-open lids, resealable options, and multi-compartment cans, particularly for segments like readymade meals. Furthermore, the market is responding to the call for eco-friendly solutions. While metal, particularly steel and aluminum, remains the dominant material, there's a burgeoning interest in lighter-weight alloys and materials with higher recycled content. The aesthetic aspect of canned food packaging is also gaining traction. Manufacturers are investing in advanced printing techniques and vibrant graphics to differentiate their products on crowded retail shelves. The "other" segment in packaging types is anticipated to grow, encompassing novel materials and composite structures designed to meet specific product needs and sustainability targets. The seafood and meat segments are seeing innovations focused on preserving freshness and nutritional value, leading to specialized can linings and closures. The overall market sentiment points towards a more sophisticated and consumer-centric approach to canned food packaging, moving beyond mere containment to become an integral part of the product's value proposition. The estimated market size for 2025 reflects this continued reliance on canned food for its practicality and affordability, but also highlights the industry's adaptation to modern demands.

The canned food packaging industry is experiencing a significant surge in demand propelled by several interconnected factors. Foremost among these is the unwavering consumer demand for convenience and extended shelf-life. In today's fast-paced world, canned foods offer a readily available and long-lasting solution for meals, snacks, and ingredients, making them indispensable for busy households, single-person dwellings, and emergency preparedness kits. This inherent practicality ensures a baseline demand that sustains the market. Secondly, global population growth and urbanization are contributing to an increased need for accessible and affordable food options. Canned food packaging plays a crucial role in food security by enabling efficient storage, transportation, and distribution of food products to diverse and often remote populations. Furthermore, advancements in packaging technology are continually improving the quality, safety, and appeal of canned goods. Innovations such as enhanced barrier properties, improved corrosion resistance, and the development of more user-friendly opening mechanisms are making canned products more attractive to consumers. The increasing focus on health and wellness also presents an opportunity, with a growing availability of canned fruits, vegetables, and lean proteins, appealing to health-conscious consumers seeking convenient ways to incorporate nutritious foods into their diets. This confluence of convenience, accessibility, and technological enhancement creates a powerful upward trajectory for the canned food packaging market.

Despite its robust growth, the canned food packaging market encounters several challenges and restraints that can impact its trajectory. A primary concern is the increasing consumer preference for fresh and minimally processed foods, which can be perceived as healthier and more natural than their canned counterparts. This sentiment, amplified by social media trends and health advocacy, can lead to a decline in demand for certain canned categories. Furthermore, environmental concerns and the drive towards sustainability pose a significant hurdle. While metal cans are highly recyclable, the production process can be energy-intensive, and the perception of waste associated with single-use packaging remains a point of contention. Consumers are increasingly scrutinizing the environmental footprint of their purchases, putting pressure on manufacturers to adopt more sustainable materials and practices. Fluctuations in raw material prices, particularly for steel and aluminum, can directly affect the cost of production and impact profit margins for packaging manufacturers. Global supply chain disruptions and geopolitical events can further exacerbate these price volatilities. Competition from alternative packaging formats, such as pouches, cartons, and glass jars, which may offer perceived advantages in terms of weight, convenience, or aesthetics for specific applications, also presents a competitive pressure. Lastly, regulatory changes and evolving food safety standards can necessitate significant investment in new packaging technologies and materials, adding to the operational costs for businesses within the sector.

The global canned food packaging market is poised for significant dominance from specific regions and segments, driven by a confluence of economic, demographic, and consumer behavior factors.

Dominant Segments:

Type: Metal (Steel and Aluminum)

Application: Readymade Meals

Dominant Regions/Countries:

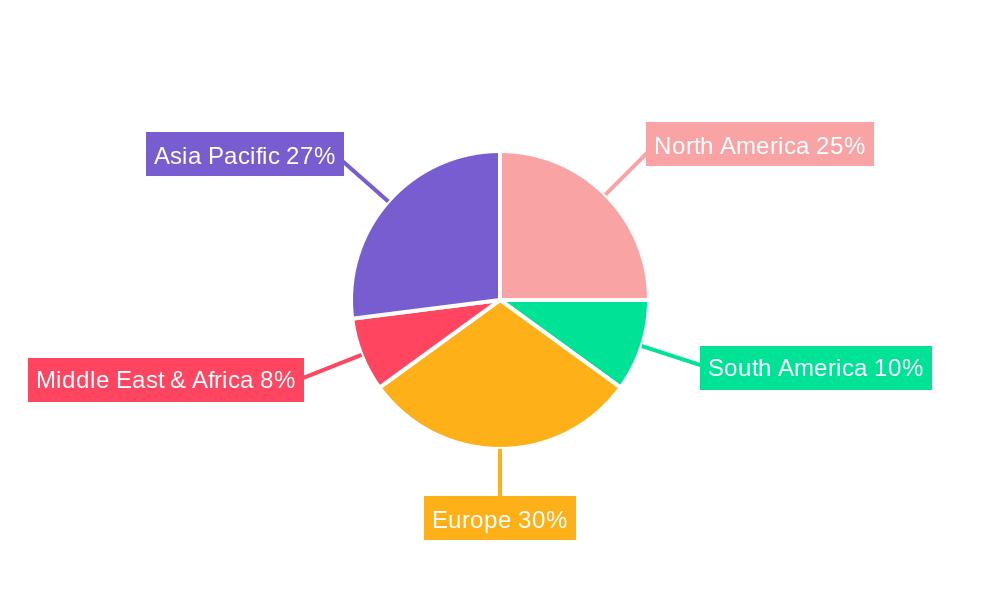

North America: This region, encompassing the United States and Canada, is a powerhouse in the canned food packaging market. Its large consumer base, well-established food processing industry, and high disposable incomes contribute to sustained demand. The strong emphasis on convenience and the presence of major food manufacturers drive innovation and market penetration. The estimated market size for canned food packaging in North America is projected to be around 40,000 million units in 2025.

Europe: With a diverse culinary landscape and a growing awareness of food preservation techniques, Europe presents a substantial market. Countries like the UK, Germany, and France are significant consumers of canned goods, spanning various applications from fruits and vegetables to meats and fish. The region's commitment to sustainability also fuels demand for recyclable and eco-friendly packaging solutions. The European market is estimated to account for approximately 35,000 million units in 2025.

Asia-Pacific: This region is expected to exhibit the highest growth rate in the coming years. Rapid urbanization, a burgeoning middle class, and increasing disposable incomes in countries like China, India, and Southeast Asian nations are driving the demand for processed and packaged foods, including canned items. The need for efficient food storage and distribution to cater to large populations further bolsters the market. The estimated market for canned food packaging in Asia-Pacific is projected to reach 30,000 million units by 2025 and is expected to be the fastest-growing region in the forecast period.

The synergy between the robust demand for metal packaging (steel and aluminum) due to their established benefits and the burgeoning application of canned solutions for readymade meals, coupled with the significant consumer base and evolving consumption patterns in North America, Europe, and the rapidly growing Asia-Pacific region, solidifies their positions as key drivers and dominators of the global canned food packaging market.

Several key catalysts are fueling the growth of the canned food packaging industry. The persistent global demand for convenience and long shelf-life remains a primary driver, especially among busy consumers and in regions with less developed cold chain infrastructure. Furthermore, advancements in packaging technology, such as improved metal alloys and innovative coating solutions, are enhancing product quality and consumer appeal. The increasing focus on food security and efficient supply chains across developing economies also creates significant opportunities for canned food packaging to play a vital role.

This comprehensive report offers an in-depth analysis of the global canned food packaging market, providing actionable insights for stakeholders. It delves into the intricate dynamics of market trends, driving forces, and challenges from the historical period of 2019-2024 through to the forecast period of 2025-2033, with the base year set at 2025. The report meticulously examines the market size in millions of units, detailing key segments like Metal (Steel, Aluminum, Others) and Applications such as Readymade Meals, Meat, Sea Food, and Others. Furthermore, it highlights significant industry developments and identifies leading players, offering a holistic view of the competitive landscape and future growth catalysts that will shape the industry's evolution.

| Aspects | Details |

|---|---|

| Study Period | 2019-2033 |

| Base Year | 2024 |

| Estimated Year | 2025 |

| Forecast Period | 2025-2033 |

| Historical Period | 2019-2024 |

| Growth Rate | CAGR of XX% from 2019-2033 |

| Segmentation |

|

Note*: In applicable scenarios

Primary Research

Secondary Research

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence

The projected CAGR is approximately XX%.

Key companies in the market include Amcor, Ardagh Group, CPMC Holdings, Crown Holdings, Grief, Silgan Holdings, Ball, Toyo Seikan Kaisha, Ball, Huber Packaging, .

The market segments include Type, Application.

The market size is estimated to be USD XXX million as of 2022.

N/A

N/A

N/A

N/A

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3480.00, USD 5220.00, and USD 6960.00 respectively.

The market size is provided in terms of value, measured in million and volume, measured in K.

Yes, the market keyword associated with the report is "Canned Food Packaging," which aids in identifying and referencing the specific market segment covered.

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

To stay informed about further developments, trends, and reports in the Canned Food Packaging, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.