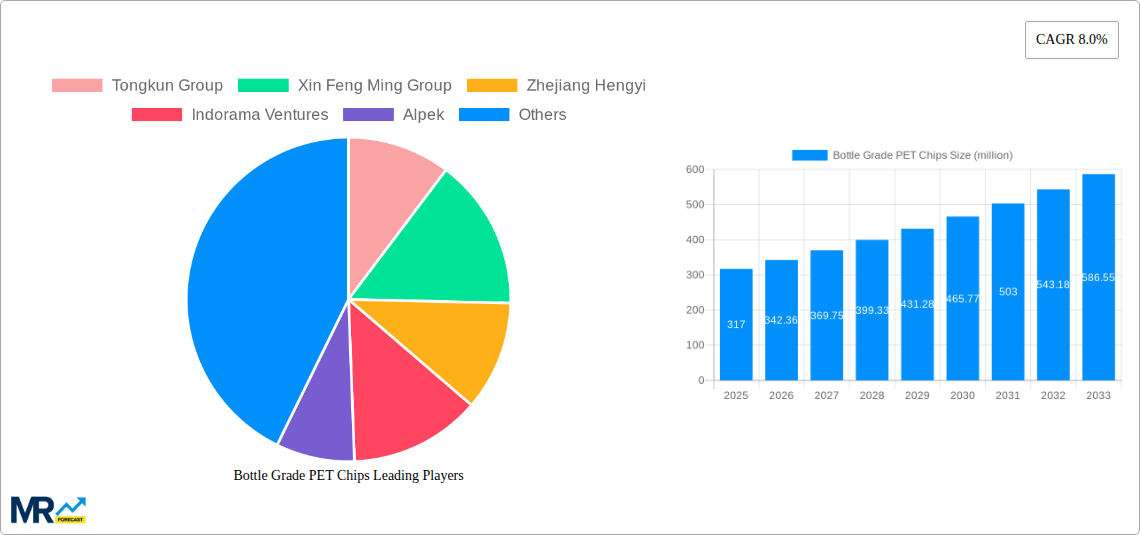

1. What is the projected Compound Annual Growth Rate (CAGR) of the Bottle Grade PET Chips?

The projected CAGR is approximately 8.0%.

MR Forecast provides premium market intelligence on deep technologies that can cause a high level of disruption in the market within the next few years. When it comes to doing market viability analyses for technologies at very early phases of development, MR Forecast is second to none. What sets us apart is our set of market estimates based on secondary research data, which in turn gets validated through primary research by key companies in the target market and other stakeholders. It only covers technologies pertaining to Healthcare, IT, big data analysis, block chain technology, Artificial Intelligence (AI), Machine Learning (ML), Internet of Things (IoT), Energy & Power, Automobile, Agriculture, Electronics, Chemical & Materials, Machinery & Equipment's, Consumer Goods, and many others at MR Forecast. Market: The market section introduces the industry to readers, including an overview, business dynamics, competitive benchmarking, and firms' profiles. This enables readers to make decisions on market entry, expansion, and exit in certain nations, regions, or worldwide. Application: We give painstaking attention to the study of every product and technology, along with its use case and user categories, under our research solutions. From here on, the process delivers accurate market estimates and forecasts apart from the best and most meaningful insights.

Products generically come under this phrase and may imply any number of goods, components, materials, technology, or any combination thereof. Any business that wants to push an innovative agenda needs data on product definitions, pricing analysis, benchmarking and roadmaps on technology, demand analysis, and patents. Our research papers contain all that and much more in a depth that makes them incredibly actionable. Products broadly encompass a wide range of goods, components, materials, technologies, or any combination thereof. For businesses aiming to advance an innovative agenda, access to comprehensive data on product definitions, pricing analysis, benchmarking, technological roadmaps, demand analysis, and patents is essential. Our research papers provide in-depth insights into these areas and more, equipping organizations with actionable information that can drive strategic decision-making and enhance competitive positioning in the market.

Bottle Grade PET Chips

Bottle Grade PET ChipsBottle Grade PET Chips by Type (Intrinsic Viscosity 0.80-0.85, Intrinsic Viscosity 0.85-0.90), by Application (Drinking Water Bottles, Mineral Water Bottles, Carbonated Drink Bottles, Big Water Bottles, Others), by North America (United States, Canada, Mexico), by South America (Brazil, Argentina, Rest of South America), by Europe (United Kingdom, Germany, France, Italy, Spain, Russia, Benelux, Nordics, Rest of Europe), by Middle East & Africa (Turkey, Israel, GCC, North Africa, South Africa, Rest of Middle East & Africa), by Asia Pacific (China, India, Japan, South Korea, ASEAN, Oceania, Rest of Asia Pacific) Forecast 2025-2033

The global Bottle Grade PET Chips market is poised for robust expansion, estimated at USD 317 million in 2025 and projected to grow at a Compound Annual Growth Rate (CAGR) of 8.0% through 2033. This significant growth is primarily propelled by the escalating demand for packaged beverages, including drinking water, mineral water, and carbonated soft drinks, driven by increasing urbanization, changing lifestyles, and a growing global population. The convenience and portability offered by PET packaging make it a preferred choice for consumers worldwide. Furthermore, advancements in PET recycling technologies and a rising consumer preference for sustainable packaging solutions are creating new avenues for market development. The intrinsic viscosity (IV) segments, particularly 0.80-0.85 and 0.85-0.90, are anticipated to witness substantial demand as manufacturers optimize resin properties for diverse bottle applications, ensuring enhanced performance and product integrity.

The market's dynamism is further shaped by several key drivers and emerging trends. A growing emphasis on food-grade and safe packaging materials, coupled with stringent regulatory frameworks governing plastic usage and recycling, is fostering innovation in PET chip formulations and production processes. The expansion of e-commerce platforms for beverage delivery also indirectly fuels demand for reliable and durable PET bottles. While the market benefits from these positive factors, it also faces certain restraints. Fluctuations in raw material prices, primarily derived from crude oil, can impact manufacturing costs and profit margins for key players. Additionally, increasing global efforts to reduce single-use plastics and promote alternative packaging materials could pose a long-term challenge. However, the inherent recyclability and energy-efficient production of PET chips position them favorably to address these concerns through continuous innovation and a focus on circular economy principles. The competitive landscape is characterized by the presence of major global players, including Tongkun Group, Xin Feng Ming Group, and Indorama Ventures, who are actively investing in capacity expansion and technological advancements to capture market share.

Here's a comprehensive report description for Bottle Grade PET Chips, incorporating your specified details and formatting:

XXX paints a vivid picture of the bottle grade PET chips market, projecting robust growth and significant shifts during the study period of 2019-2033. The base year of 2025 marks a pivotal point, with the estimated year also being 2025, providing a solid foundation for the forecast period of 2025-2033. The historical period of 2019-2024 offers crucial insights into past performance, highlighting steady expansion driven by increasing global beverage consumption and evolving packaging preferences. A key trend emerging is the sustained demand for high-quality PET chips that offer superior clarity, strength, and barrier properties essential for the safe and appealing packaging of a wide array of beverages, from still water to carbonated drinks.

The market is witnessing a continuous push towards innovation in PET chip technology. Manufacturers are increasingly focusing on developing grades with enhanced recyclability and a reduced environmental footprint. This includes exploring advanced polymerization techniques and additive packages that facilitate closed-loop recycling systems. The intrinsic viscosity (IV) of PET chips is a critical determinant of their suitability for different bottle applications. The market is showing a significant preference for IV ranges of 0.80-0.85 and 0.85-0.90, as these offer the optimal balance of processability and mechanical strength required for demanding bottle manufacturing. The rising consumer awareness regarding sustainable packaging solutions is acting as a powerful tailwind, encouraging brands to opt for PET that can be effectively recycled and reused. Furthermore, the shift towards lightweighting in packaging design continues to influence the demand for PET chips that can deliver comparable performance with reduced material usage. The global beverage industry's ongoing expansion, coupled with the growing middle class in emerging economies, is expected to fuel the demand for bottled beverages, thereby directly impacting the bottle grade PET chips market positively. The estimated market size, measured in millions, is projected to witness a considerable upward trajectory as these trends converge.

The bottle grade PET chips market is being propelled by a confluence of powerful factors that are fundamentally reshaping the packaging landscape. Foremost among these is the ever-increasing global demand for packaged beverages. As populations grow and urbanization accelerates, particularly in emerging economies, the consumption of bottled water, soft drinks, and other beverages continues to rise. This escalating demand directly translates into a higher requirement for PET chips, the primary material for producing these ubiquitous plastic bottles. The inherent advantages of PET – its lightweight nature, excellent clarity, good barrier properties against oxygen and carbon dioxide, and shatter resistance – make it the material of choice for a vast majority of beverage applications.

Furthermore, the ongoing evolution of the beverage industry itself plays a crucial role. The proliferation of new beverage categories, including functional drinks, premium waters, and ready-to-drink (RTD) beverages, each requiring specific packaging attributes, further diversifies the demand for PET chips with tailored properties. The industry's focus on product safety and shelf-life extension also favors PET, which offers a robust barrier against spoilage. Moreover, significant investments in production capacity by major PET chip manufacturers globally are ensuring a steady supply to meet this burgeoning demand. The drive towards cost-effectiveness in packaging also benefits PET, as it generally offers a competitive price point compared to alternative materials for many applications. The growing adoption of advanced manufacturing technologies in bottle production also allows for the efficient utilization of PET chips, further solidifying its market position.

Despite the robust growth trajectory, the bottle grade PET chips market is not without its challenges and restraints, which could temper its expansion. Paramount among these is the increasing scrutiny and regulatory pressure surrounding single-use plastics. Growing environmental consciousness among consumers and governments has led to a surge in plastic waste concerns, prompting calls for reduced plastic consumption and the implementation of stricter regulations on plastic packaging. This can manifest in bans or taxes on certain types of plastic products, potentially impacting the demand for PET. The negative perception of plastic pollution, often amplified by media coverage, can also influence consumer choices and brand preferences, leading to a preference for alternative, perceived as more sustainable, packaging materials.

Moreover, the market faces significant volatility in raw material prices. PET chips are derived from petrochemical feedstocks like PTA (purified terephthalic acid) and MEG (monoethylene glycol). Fluctuations in crude oil prices and the availability of these precursors can directly impact the production costs and pricing of PET chips, leading to uncertainty and potential margin pressures for manufacturers. The development and widespread adoption of viable and cost-effective alternatives to PET, such as advanced bioplastics or innovative paper-based packaging solutions, also pose a potential long-term threat. While currently not as widespread or cost-competitive for all applications, continuous advancements in these alternative materials could erode PET's market share over time. The logistics and infrastructure for collecting, sorting, and recycling PET bottles are also crucial. In regions with underdeveloped recycling systems, the overall sustainability of PET packaging is compromised, creating a perception issue and hindering market growth.

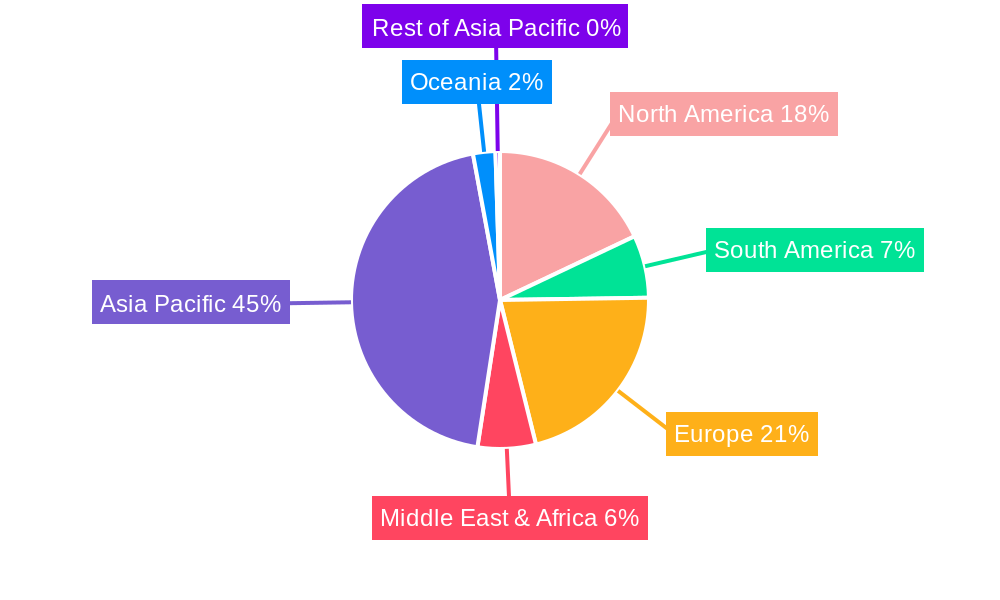

The Asia-Pacific region, particularly China, is poised to dominate the bottle grade PET chips market, driven by a potent combination of factors that underpin both production and consumption. This dominance is further amplified by the exceptional performance of the Drinking Water Bottles and Mineral Water Bottles segments within the broader Application category.

Asia-Pacific's Dominance:

Dominant Segments:

The synergy between the manufacturing prowess and massive consumer base of the Asia-Pacific region, coupled with the enduring demand for fundamental beverage applications like drinking water and mineral water bottles, firmly establishes this region and these segments as the dominant forces in the global bottle grade PET chips market.

The bottle grade PET chips industry is experiencing significant growth catalysts that are shaping its future trajectory. A primary driver is the increasing global demand for packaged beverages, fueled by population growth, urbanization, and rising disposable incomes, particularly in emerging economies. This directly translates to a higher need for PET bottles. Furthermore, advancements in recycling technologies and the growing emphasis on a circular economy are bolstering the sustainability credentials of PET, encouraging its continued use and driving investment in recycled PET (rPET) content. The development of lightweighting technologies in bottle design, allowing for the production of stronger yet thinner bottles, also enhances PET's appeal by reducing material consumption and transportation costs.

This comprehensive report delves deep into the intricacies of the bottle grade PET chips market, offering an unparalleled 360-degree view. It meticulously analyzes market dynamics, providing granular insights into historical trends (2019-2024) and projecting future growth through the estimated year of 2025 and a detailed forecast period extending to 2033. The report scrutinizes the key drivers propelling the market forward, such as the burgeoning global demand for beverages and the growing adoption of circular economy principles in packaging. Simultaneously, it sheds light on the significant challenges and restraints, including regulatory pressures on single-use plastics and raw material price volatility. The analysis extends to identifying dominant regions and countries, with a specific focus on the Asia-Pacific and the crucial role of China. Furthermore, it dissects market segmentation by intrinsic viscosity (0.80-0.85 and 0.85-0.90) and application (Drinking Water Bottles, Mineral Water Bottles, Carbonated Drink Bottles, Big Water Bottles, Others), highlighting their respective growth trajectories and market shares. The report also profiles leading players and discusses their strategic initiatives and recent developments, offering valuable intelligence for stakeholders to navigate this dynamic market.

| Aspects | Details |

|---|---|

| Study Period | 2019-2033 |

| Base Year | 2024 |

| Estimated Year | 2025 |

| Forecast Period | 2025-2033 |

| Historical Period | 2019-2024 |

| Growth Rate | CAGR of 8.0% from 2019-2033 |

| Segmentation |

|

Note*: In applicable scenarios

Primary Research

Secondary Research

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence

The projected CAGR is approximately 8.0%.

Key companies in the market include Tongkun Group, Xin Feng Ming Group, Zhejiang Hengyi, Indorama Ventures, Alpek, FENC, Reliance Industries, Sheng Hong Group, Hengli Group, Billion Industrial, Rongsheng Petrochemical, Sanfangxiang Group, Sinopec Yizheng, Since CR Chemicals, JBF, Octal, NanYa, Wankai New Materials, Dhunseri Petrochem & Tea, SABIC, NEO GROUP, .

The market segments include Type, Application.

The market size is estimated to be USD 317 million as of 2022.

N/A

N/A

N/A

N/A

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3480.00, USD 5220.00, and USD 6960.00 respectively.

The market size is provided in terms of value, measured in million and volume, measured in K.

Yes, the market keyword associated with the report is "Bottle Grade PET Chips," which aids in identifying and referencing the specific market segment covered.

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

To stay informed about further developments, trends, and reports in the Bottle Grade PET Chips, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.