1. What is the projected Compound Annual Growth Rate (CAGR) of the Automotive & Vehicle Insurance?

The projected CAGR is approximately XX%.

Automotive & Vehicle Insurance

Automotive & Vehicle InsuranceAutomotive & Vehicle Insurance by Type (/> Liability Insurance, Collision Coverage, Comprehensive Coverage, Personal Injury Protection), by Application (/> Passenger Car, Commercial Vehicle), by North America (United States, Canada, Mexico), by South America (Brazil, Argentina, Rest of South America), by Europe (United Kingdom, Germany, France, Italy, Spain, Russia, Benelux, Nordics, Rest of Europe), by Middle East & Africa (Turkey, Israel, GCC, North Africa, South Africa, Rest of Middle East & Africa), by Asia Pacific (China, India, Japan, South Korea, ASEAN, Oceania, Rest of Asia Pacific) Forecast 2026-2034

MR Forecast provides premium market intelligence on deep technologies that can cause a high level of disruption in the market within the next few years. When it comes to doing market viability analyses for technologies at very early phases of development, MR Forecast is second to none. What sets us apart is our set of market estimates based on secondary research data, which in turn gets validated through primary research by key companies in the target market and other stakeholders. It only covers technologies pertaining to Healthcare, IT, big data analysis, block chain technology, Artificial Intelligence (AI), Machine Learning (ML), Internet of Things (IoT), Energy & Power, Automobile, Agriculture, Electronics, Chemical & Materials, Machinery & Equipment's, Consumer Goods, and many others at MR Forecast. Market: The market section introduces the industry to readers, including an overview, business dynamics, competitive benchmarking, and firms' profiles. This enables readers to make decisions on market entry, expansion, and exit in certain nations, regions, or worldwide. Application: We give painstaking attention to the study of every product and technology, along with its use case and user categories, under our research solutions. From here on, the process delivers accurate market estimates and forecasts apart from the best and most meaningful insights.

Products generically come under this phrase and may imply any number of goods, components, materials, technology, or any combination thereof. Any business that wants to push an innovative agenda needs data on product definitions, pricing analysis, benchmarking and roadmaps on technology, demand analysis, and patents. Our research papers contain all that and much more in a depth that makes them incredibly actionable. Products broadly encompass a wide range of goods, components, materials, technologies, or any combination thereof. For businesses aiming to advance an innovative agenda, access to comprehensive data on product definitions, pricing analysis, benchmarking, technological roadmaps, demand analysis, and patents is essential. Our research papers provide in-depth insights into these areas and more, equipping organizations with actionable information that can drive strategic decision-making and enhance competitive positioning in the market.

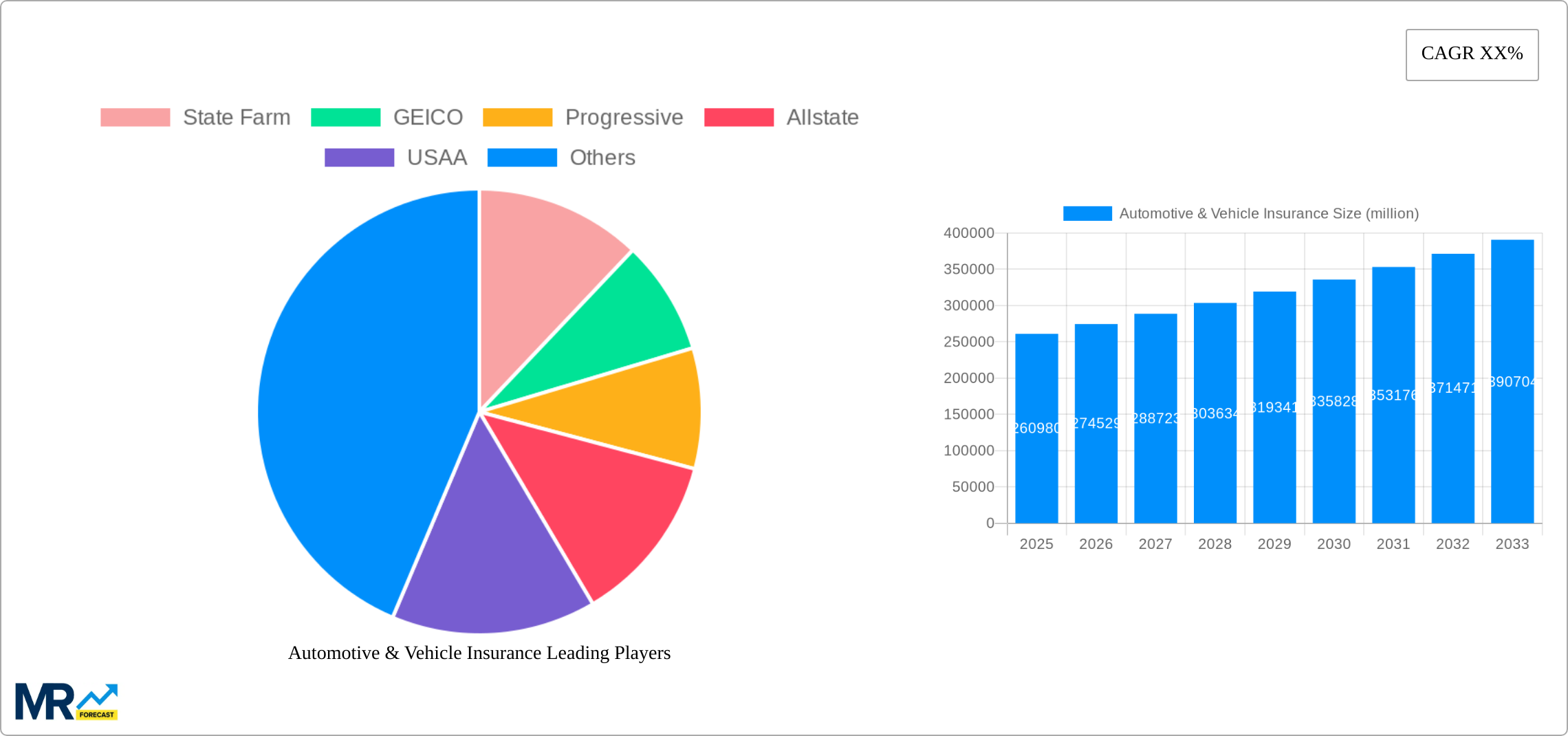

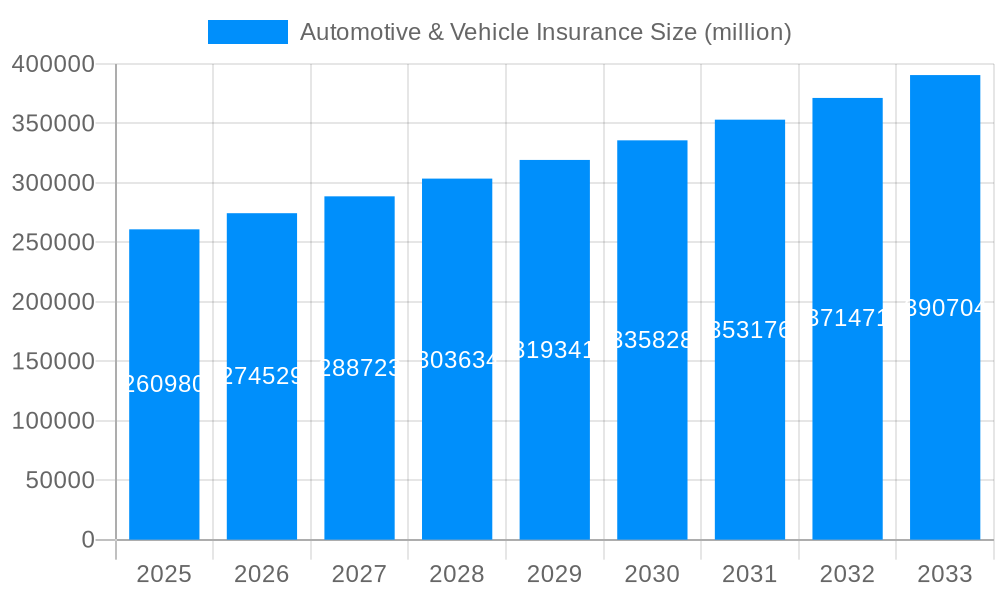

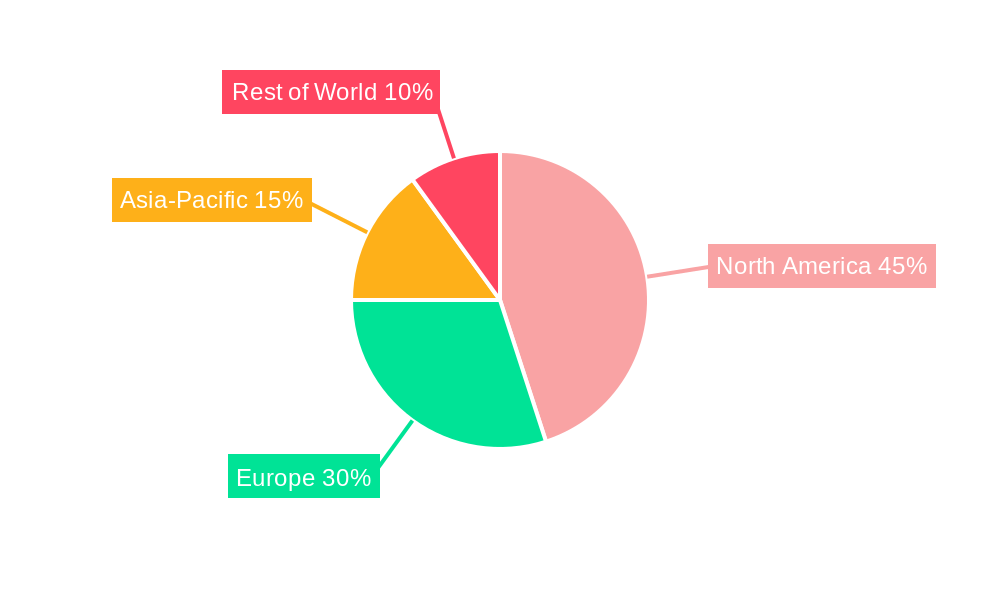

The automotive and vehicle insurance market, valued at $260.98 billion in 2025, is poised for significant growth over the next decade. This robust market is driven by several factors, including a rising number of vehicle registrations globally, increasing vehicle ownership in developing economies, and a growing awareness of the need for comprehensive insurance coverage. Stringent government regulations mandating minimum insurance coverage in many countries further bolster market expansion. Technological advancements, such as telematics and usage-based insurance (UBI), are transforming the industry, offering personalized premiums based on driving behavior and promoting safer driving practices. However, the market faces challenges such as fluctuating fuel prices, economic downturns impacting consumer spending, and increasing insurance fraud. Competitive pressures among established players like State Farm, GEICO, Progressive, Allstate, USAA, Liberty Mutual, Farmers, Nationwide, Travelers, and American Family, also influence market dynamics. The market is segmented based on various factors including vehicle type, coverage type (liability, collision, comprehensive), and distribution channels (direct, agents, brokers). While precise regional breakdowns are unavailable, it's reasonable to assume a significant share held by North America and Europe, reflecting high vehicle ownership and insurance penetration rates in these regions.

Projecting a conservative but realistic CAGR of 5% (a common range for mature insurance markets), the market is expected to reach approximately $365 billion by 2033. This projection accounts for both organic growth from expanding vehicle ownership and market penetration, as well as potential market disruptions from technological innovation. The competitive landscape will likely see consolidation and increased technological investment as insurers strive to offer innovative products and improve operational efficiency. Focus on personalized insurance packages and leveraging data analytics for risk assessment and fraud detection will be key to success in this evolving market.

The automotive and vehicle insurance market, valued at hundreds of millions of units in 2024, is experiencing a period of significant transformation driven by technological advancements, evolving consumer behavior, and shifting regulatory landscapes. The historical period (2019-2024) witnessed steady growth, largely fueled by increasing vehicle ownership, particularly in developing economies. However, the forecast period (2025-2033) promises even more dynamic change. The estimated market size in 2025 (our base year) reflects a consolidation of market share among leading players and a growing emphasis on data-driven risk assessment and personalized insurance products. We project continued growth throughout the study period (2019-2033), albeit at a potentially moderated pace compared to the previous five years, as market saturation in developed nations becomes a factor. The rise of telematics and connected car technology is fundamentally altering how risk is assessed, leading to usage-based insurance (UBI) models that reward safe driving behavior. This shift necessitates substantial investments in data analytics and infrastructure by insurers. Furthermore, the increasing prevalence of autonomous vehicles poses both opportunities and challenges, requiring insurers to adapt their underwriting models and product offerings to account for the unique risk profiles of self-driving technology. The competitive landscape is also intensifying, with traditional insurers facing increased pressure from insurtech startups offering innovative digital solutions and agile business models. This competitive pressure is pushing established players to innovate and invest in digital transformation to maintain their market positions. Finally, regulatory changes concerning data privacy, autonomous driving, and environmental sustainability are shaping the future of the industry, requiring insurers to navigate complex legal and ethical considerations.

Several key factors are driving the growth of the automotive and vehicle insurance market. The expansion of the global vehicle fleet, particularly in emerging markets experiencing rapid economic development and increasing car ownership, constitutes a major growth driver. Technological advancements, such as telematics and the Internet of Things (IoT), are revolutionizing risk assessment and enabling the development of personalized insurance products based on individual driving behavior. This shift towards usage-based insurance (UBI) is creating new opportunities for insurers to offer more competitive and customized policies. Furthermore, the increasing sophistication of data analytics allows insurers to better understand and manage risk, leading to improved underwriting practices and more accurate pricing models. The growing awareness of the need for comprehensive insurance coverage, especially in regions with stringent regulations, is contributing to market expansion. Lastly, regulatory changes aimed at enhancing consumer protection and promoting fair practices are also shaping the industry, driving demand for compliant and reliable insurance providers. These combined factors point towards a sustained period of growth for the automotive and vehicle insurance sector, though challenges remain.

Despite the positive growth outlook, several challenges and restraints impact the automotive and vehicle insurance market. Increasingly stringent regulations related to data privacy and consumer protection require significant investments in compliance measures, adding to operational costs. The rise of autonomous vehicles presents both opportunities and challenges, forcing insurers to adapt their underwriting models and develop new insurance products suited to the unique risk profiles of self-driving technology. The increasing penetration of insurtech startups offering innovative digital solutions disrupts the traditional insurance model, creating a highly competitive landscape that requires established players to digitally transform their operations to remain competitive. Economic downturns and fluctuations in fuel prices can impact consumer spending on insurance, potentially affecting demand. Finally, the rising frequency and severity of natural disasters and other catastrophic events increase claims costs, impacting insurers' profitability. These challenges necessitate proactive strategies from insurers to mitigate risks and maintain profitability in a dynamic and rapidly evolving market.

The North American market, particularly the United States, is expected to continue its dominance in the automotive and vehicle insurance sector throughout the forecast period. This is largely attributed to high vehicle ownership rates, robust economic conditions, and a mature insurance market with established players.

United States: The sheer size and density of the US automobile market make it a key driver of global growth. Strong regulatory frameworks also contribute to a well-developed insurance sector.

Regional Variations: Growth rates will vary across regions. Developing economies in Asia and Latin America will likely show higher growth rates, driven by rising vehicle sales and increased insurance penetration. However, these markets often face challenges related to infrastructure development and regulatory consistency.

Segment Dominance: The personal auto insurance segment remains the largest and most dominant segment of the market globally. This reflects the widespread ownership of personal vehicles and the associated need for liability and collision coverage. However, commercial auto insurance is also showing healthy growth, linked to increased business activity and fleet expansion.

Technological Impact: The commercial auto insurance segment stands to benefit particularly from telematics and IoT technologies. Fleet management tools and driver monitoring systems create opportunities for insurers to implement risk-based pricing and improve safety outcomes, potentially lowering claim costs.

Shifting Trends: While personal auto remains dominant, growth in segments like electric vehicle insurance (responding to the rise of EVs) and autonomous vehicle insurance (although still nascent) represent significant emerging opportunities requiring insurers to adapt their products and risk assessment models. This segmental diversification adds complexity but also offers strong future potential.

Market Consolidation: Consolidation amongst larger insurers is also anticipated, as smaller companies struggle to compete with the technological advancements and data-driven strategies of larger corporations.

In summary, while the US personal auto segment maintains the strongest position, substantial growth opportunities exist in emerging markets and developing segments. Insurers that effectively leverage technological advancements and adapt to evolving consumer needs are best positioned to thrive in this dynamic environment.

The growth of the automotive and vehicle insurance industry is being propelled by several key factors. The increasing adoption of telematics and connected car technologies allows for more accurate risk assessment and the development of usage-based insurance (UBI) models, driving efficiency and customized pricing. The expanding electric vehicle market creates a need for specialized insurance products tailored to the unique characteristics of EVs. Furthermore, growing awareness of the importance of comprehensive insurance coverage and favorable regulatory frameworks in several key markets are contributing to market expansion. These factors, along with robust economic growth in certain regions, contribute significantly to the market's positive trajectory.

This report provides a comprehensive analysis of the automotive and vehicle insurance market, covering market trends, driving forces, challenges, key players, and significant developments. It offers valuable insights into the evolving landscape of the industry, including the impact of technological advancements and regulatory changes. The report's detailed analysis allows stakeholders to make informed decisions and develop effective strategies to navigate the dynamic environment of the automotive and vehicle insurance sector. The data presented covers the historical period (2019-2024), base year (2025), estimated year (2025), and forecast period (2025-2033) providing a comprehensive view of market performance and future prospects.

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of XX% from 2020-2034 |

| Segmentation |

|

Note*: In applicable scenarios

Primary Research

Secondary Research

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence

The projected CAGR is approximately XX%.

Key companies in the market include State Farm, GEICO, Progressive, Allstate, USAA, Liberty Mutual, Farmers, Nationwide, Travelers, American Family, .

The market segments include Type, Application.

The market size is estimated to be USD 260980 million as of 2022.

N/A

N/A

N/A

N/A

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4480.00, USD 6720.00, and USD 8960.00 respectively.

The market size is provided in terms of value, measured in million.

Yes, the market keyword associated with the report is "Automotive & Vehicle Insurance," which aids in identifying and referencing the specific market segment covered.

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

To stay informed about further developments, trends, and reports in the Automotive & Vehicle Insurance, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.