1. What is the projected Compound Annual Growth Rate (CAGR) of the Automotive Polymer OLED Materials?

The projected CAGR is approximately 14.35%.

Automotive Polymer OLED Materials

Automotive Polymer OLED MaterialsAutomotive Polymer OLED Materials by Type (Luminous Layer Material, Electron Injection Layer Material, Electronic Transport Layer Material, Others), by Application (Dashboard Display, Smart Car Windows, Others), by North America (United States, Canada, Mexico), by South America (Brazil, Argentina, Rest of South America), by Europe (United Kingdom, Germany, France, Italy, Spain, Russia, Benelux, Nordics, Rest of Europe), by Middle East & Africa (Turkey, Israel, GCC, North Africa, South Africa, Rest of Middle East & Africa), by Asia Pacific (China, India, Japan, South Korea, ASEAN, Oceania, Rest of Asia Pacific) Forecast 2026-2034

MR Forecast provides premium market intelligence on deep technologies that can cause a high level of disruption in the market within the next few years. When it comes to doing market viability analyses for technologies at very early phases of development, MR Forecast is second to none. What sets us apart is our set of market estimates based on secondary research data, which in turn gets validated through primary research by key companies in the target market and other stakeholders. It only covers technologies pertaining to Healthcare, IT, big data analysis, block chain technology, Artificial Intelligence (AI), Machine Learning (ML), Internet of Things (IoT), Energy & Power, Automobile, Agriculture, Electronics, Chemical & Materials, Machinery & Equipment's, Consumer Goods, and many others at MR Forecast. Market: The market section introduces the industry to readers, including an overview, business dynamics, competitive benchmarking, and firms' profiles. This enables readers to make decisions on market entry, expansion, and exit in certain nations, regions, or worldwide. Application: We give painstaking attention to the study of every product and technology, along with its use case and user categories, under our research solutions. From here on, the process delivers accurate market estimates and forecasts apart from the best and most meaningful insights.

Products generically come under this phrase and may imply any number of goods, components, materials, technology, or any combination thereof. Any business that wants to push an innovative agenda needs data on product definitions, pricing analysis, benchmarking and roadmaps on technology, demand analysis, and patents. Our research papers contain all that and much more in a depth that makes them incredibly actionable. Products broadly encompass a wide range of goods, components, materials, technologies, or any combination thereof. For businesses aiming to advance an innovative agenda, access to comprehensive data on product definitions, pricing analysis, benchmarking, technological roadmaps, demand analysis, and patents is essential. Our research papers provide in-depth insights into these areas and more, equipping organizations with actionable information that can drive strategic decision-making and enhance competitive positioning in the market.

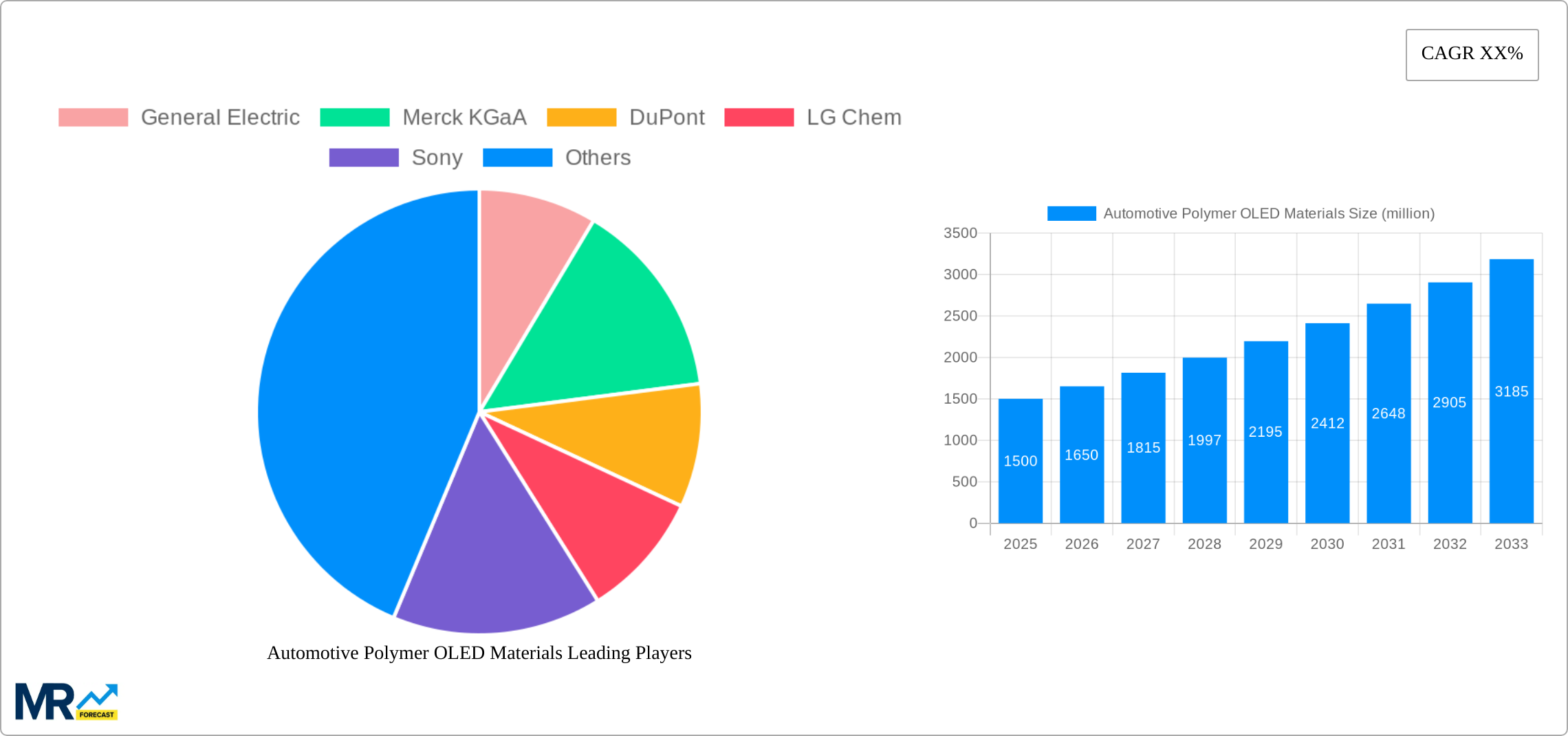

The global automotive polymer OLED materials market is projected to experience significant expansion, driven by the growing adoption of Advanced Driver-Assistance Systems (ADAS), sophisticated infotainment, and the rising prevalence of Electric Vehicles (EVs). This growth is underpinned by the superior visual performance of polymer OLEDs over traditional LCDs, offering enhanced contrast, wider viewing angles, and superior color accuracy. These attributes elevate the driver and passenger experience, making them increasingly sought after in premium vehicles and gradually penetrating the mass market. Key market segments include luminous layer materials, electron injection layer materials, and electron transport layer materials. Application areas are currently dominated by dashboard displays and smart car windows, aligning with the trend of integrating advanced displays throughout vehicle interiors and exteriors. Leading companies such as General Electric, Merck KGaA, DuPont, LG Chem, Sony, and Sumitomo Chemical are actively engaged in research and development, fostering innovation and market capabilities. Robust growth is anticipated across North America, Europe, and Asia-Pacific, spurred by increasing vehicle production, rising disposable incomes, and supportive government initiatives for automotive technology advancement.

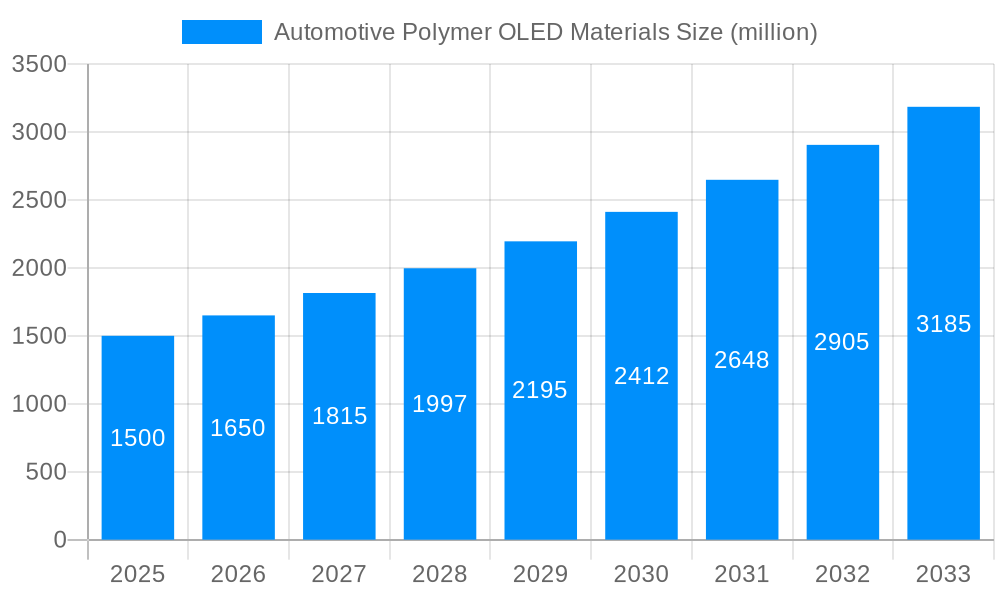

The forecast period from 2025 to 2033 anticipates robust expansion for the automotive polymer OLED materials market, with an estimated market size of 13.08 billion by 2033. The Compound Annual Growth Rate (CAGR) is projected at a strong 14.35% from the base year 2025. This expansion is fueled by the integration of these materials in new vehicle models and the continuous adoption of advanced automotive technologies. Market segmentation highlights dashboard displays and smart car windows as key application areas, reflecting the trend towards larger, higher-resolution displays in vehicles. The increasing adoption of ADAS and other driver-assistance features further necessitates higher-quality display technology, solidifying demand for polymer OLED materials. Competitive dynamics among key players are expected to intensify, driving innovation in material science and manufacturing, leading to cost reductions and performance enhancements for widespread industry adoption. Consistent global demand for these materials is anticipated, supported by sustained investment in research and development and escalating consumer expectations for advanced automotive technology.

The automotive industry is undergoing a dramatic transformation, driven by the increasing demand for advanced driver-assistance systems (ADAS) and infotainment features. This shift is significantly impacting the market for automotive polymer OLED materials. The global consumption value of these materials is experiencing robust growth, projected to reach several billion USD by 2033. This surge is fueled by the rising adoption of flexible and large-area displays in vehicles, surpassing the limitations of traditional LCD technology. The advantages offered by polymer OLEDs, such as superior image quality, thinner profiles, and lower power consumption, are proving irresistible to automakers striving for enhanced aesthetics and fuel efficiency. The market is witnessing a dynamic shift towards flexible displays, particularly for dashboard displays and smart car windows. This trend is creating new opportunities for material suppliers specializing in flexible substrates and high-performance polymer OLED materials. The historical period (2019-2024) showed a steady incline in consumption, with the estimated year (2025) marking a significant inflection point. The forecast period (2025-2033) promises even more substantial growth, driven by technological advancements and increased vehicle production, particularly in the electric vehicle segment. The market is characterized by intense competition among leading material suppliers, each vying for market share through innovation and strategic partnerships. This necessitates a deep understanding of evolving material specifications, manufacturing processes, and emerging application trends to maintain a competitive edge in this rapidly evolving sector. The adoption of polymer OLEDs is not solely driven by visual enhancements but also by safety concerns. The potential for integration with augmented reality and heads-up displays is further contributing to the market's expansion. The study period (2019-2033), encompassing historical, estimated, and forecast years, showcases a clear and compelling trajectory for automotive polymer OLED material growth.

Several key factors are propelling the growth of the automotive polymer OLED materials market. The relentless pursuit of enhanced in-vehicle experiences is a primary driver. Consumers increasingly expect sophisticated infotainment systems, seamlessly integrated displays, and intuitive user interfaces. Polymer OLEDs, with their vibrant colors, high contrast ratios, and wide viewing angles, perfectly meet this demand. Furthermore, the automotive industry's focus on lightweighting and fuel efficiency is contributing to the adoption of polymer OLEDs. Their thinner profiles compared to traditional LCDs contribute to weight reduction, positively impacting vehicle performance and fuel economy. The increasing integration of advanced driver-assistance systems (ADAS) requires high-resolution displays capable of presenting critical information clearly and effectively. Polymer OLEDs provide the ideal platform for these applications, enabling the development of clear, sharp, and easily readable displays for navigation, blind-spot monitoring, and other ADAS features. Government regulations and safety standards are also playing a role, pushing for the development of more advanced and safer vehicles, leading to increased demand for the high-quality displays that polymer OLEDs enable. Finally, the rise of electric vehicles (EVs) represents a significant growth opportunity. EV dashboards and infotainment systems frequently incorporate large, high-resolution displays, further boosting the demand for polymer OLED materials.

Despite the promising outlook, the automotive polymer OLED materials market faces several challenges. The high cost of manufacturing polymer OLED displays remains a significant barrier, especially when compared to traditional LCD technologies. This cost is reflected in the price of the materials themselves, potentially limiting their adoption in budget-conscious vehicle segments. The long-term stability and durability of polymer OLEDs under harsh automotive conditions (extreme temperatures, vibrations, and UV exposure) also present challenges. Extensive testing and development are crucial to ensure the reliability and longevity of these displays within vehicles. Furthermore, the complex manufacturing process involved in producing high-quality polymer OLEDs necessitates sophisticated equipment and skilled labor, contributing to increased production costs. Competition from alternative display technologies, such as microLEDs and advanced LCDs, also puts pressure on the market. These alternative technologies are continually improving, offering competitive features and potentially lower prices, impacting the market share of polymer OLEDs. Finally, the supply chain for specialized materials used in polymer OLED production can be fragile, potentially leading to shortages and price fluctuations. Addressing these challenges through ongoing research and development, optimization of manufacturing processes, and robust quality control measures is vital for the continued growth of the automotive polymer OLED materials market.

The dashboard display segment is poised to dominate the automotive polymer OLED materials market. This is due to the increasing complexity and size of in-vehicle infotainment systems. Modern dashboards often integrate multiple displays for navigation, instrument clusters, entertainment, and driver assistance, driving demand for high-quality polymer OLED materials. The ability to create curved and customizable dashboards further enhances their appeal.

High Growth Potential: The dashboard display segment is projected to experience the highest growth rate within the forecast period (2025-2033). This robust growth is driven by the integration of advanced functionalities, such as augmented reality (AR) overlays and driver monitoring systems, which rely on high-resolution polymer OLED displays.

Technological Advancements: Continuous improvements in material efficiency, brightness, and color gamut are enhancing the appeal of polymer OLEDs for dashboard applications. These advancements directly translate to higher demand and market share.

Luxury Vehicle Dominance: Initially, the adoption of polymer OLED dashboards will likely be concentrated in high-end vehicles. However, cost reductions and technological advancements are expected to gradually expand the market into mid-range and potentially even entry-level vehicles in the latter part of the forecast period.

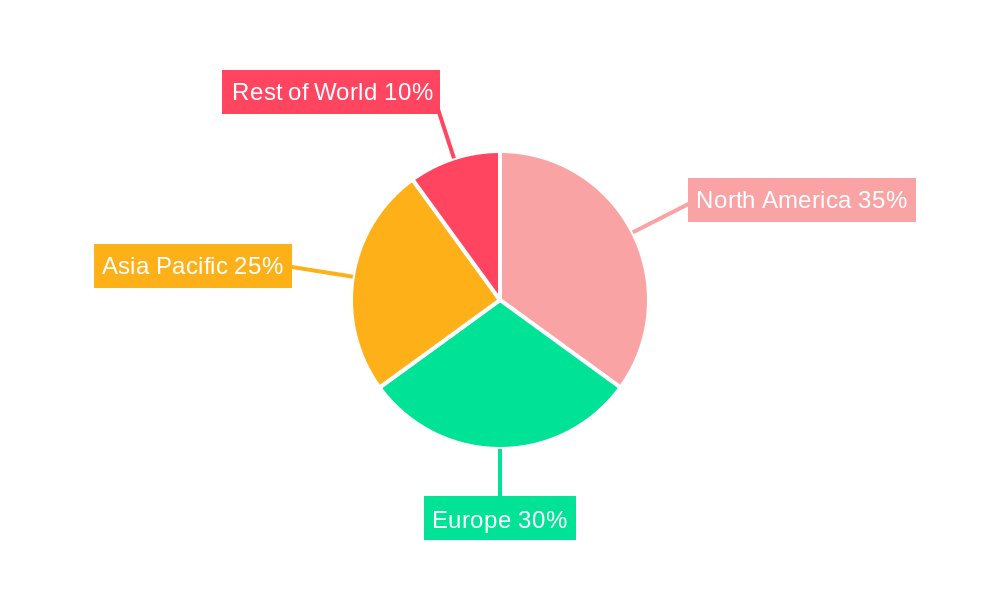

Geographic Dominance: Asia-Pacific (specifically, countries like China, Japan, South Korea) is expected to dominate the global automotive polymer OLED materials market due to the high concentration of automotive manufacturing and a rapidly growing EV market. The region's focus on technological advancement and increased consumer demand for premium vehicle features accelerates this segment's adoption. North America and Europe also hold significant market share, driven by their established automotive industries and high consumer adoption rates for advanced vehicle technologies. However, the rate of growth in the Asia-Pacific region is likely to surpass that of other regions during the forecast period. The growth is driven by factors including a rapidly expanding automobile production base, significant investments in automotive R&D and the accelerating acceptance of new technologies within the car market.

The convergence of several factors is fueling growth in the automotive polymer OLED materials industry. Firstly, the burgeoning demand for sophisticated infotainment systems and advanced driver-assistance features is driving adoption of high-performance displays. Secondly, the automotive industry's focus on lightweighting and fuel efficiency enhances the competitive advantage of polymer OLEDs over traditional displays. Finally, the rise of electric vehicles, with their large infotainment screens and digital instrument clusters, further fuels the market’s expansion. These interwoven factors contribute to a sustained period of significant growth for automotive polymer OLED materials.

This report provides a comprehensive analysis of the automotive polymer OLED materials market, covering historical data, current market conditions, and future projections. It offers in-depth insights into market trends, driving forces, challenges, key players, and significant developments. The report segments the market by material type, application, and geography, providing a granular understanding of market dynamics and growth opportunities. It also incorporates detailed financial forecasts, enabling stakeholders to make informed strategic decisions related to this rapidly evolving industry. By providing a clear picture of the current market landscape and anticipating future developments, this report serves as an invaluable resource for businesses and investors in the automotive industry.

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 14.35% from 2020-2034 |

| Segmentation |

|

Note*: In applicable scenarios

Primary Research

Secondary Research

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence

The projected CAGR is approximately 14.35%.

Key companies in the market include General Electric, Merck KGaA, DuPont, LG Chem, Sony, Sumitomo Chemical.

The market segments include Type, Application.

The market size is estimated to be USD 13.08 billion as of 2022.

N/A

N/A

N/A

N/A

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3480.00, USD 5220.00, and USD 6960.00 respectively.

The market size is provided in terms of value, measured in billion and volume, measured in K.

Yes, the market keyword associated with the report is "Automotive Polymer OLED Materials," which aids in identifying and referencing the specific market segment covered.

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

To stay informed about further developments, trends, and reports in the Automotive Polymer OLED Materials, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.