1. What is the projected Compound Annual Growth Rate (CAGR) of the Automotive New Materials?

The projected CAGR is approximately XX%.

MR Forecast provides premium market intelligence on deep technologies that can cause a high level of disruption in the market within the next few years. When it comes to doing market viability analyses for technologies at very early phases of development, MR Forecast is second to none. What sets us apart is our set of market estimates based on secondary research data, which in turn gets validated through primary research by key companies in the target market and other stakeholders. It only covers technologies pertaining to Healthcare, IT, big data analysis, block chain technology, Artificial Intelligence (AI), Machine Learning (ML), Internet of Things (IoT), Energy & Power, Automobile, Agriculture, Electronics, Chemical & Materials, Machinery & Equipment's, Consumer Goods, and many others at MR Forecast. Market: The market section introduces the industry to readers, including an overview, business dynamics, competitive benchmarking, and firms' profiles. This enables readers to make decisions on market entry, expansion, and exit in certain nations, regions, or worldwide. Application: We give painstaking attention to the study of every product and technology, along with its use case and user categories, under our research solutions. From here on, the process delivers accurate market estimates and forecasts apart from the best and most meaningful insights.

Products generically come under this phrase and may imply any number of goods, components, materials, technology, or any combination thereof. Any business that wants to push an innovative agenda needs data on product definitions, pricing analysis, benchmarking and roadmaps on technology, demand analysis, and patents. Our research papers contain all that and much more in a depth that makes them incredibly actionable. Products broadly encompass a wide range of goods, components, materials, technologies, or any combination thereof. For businesses aiming to advance an innovative agenda, access to comprehensive data on product definitions, pricing analysis, benchmarking, technological roadmaps, demand analysis, and patents is essential. Our research papers provide in-depth insights into these areas and more, equipping organizations with actionable information that can drive strategic decision-making and enhance competitive positioning in the market.

Automotive New Materials

Automotive New MaterialsAutomotive New Materials by Application (Passenger Cars, Light Commercial Vehicles, Heavy Commercial Vehicles), by Type (Metal Materials, Polymer Materials, Functional Materials), by North America (United States, Canada, Mexico), by South America (Brazil, Argentina, Rest of South America), by Europe (United Kingdom, Germany, France, Italy, Spain, Russia, Benelux, Nordics, Rest of Europe), by Middle East & Africa (Turkey, Israel, GCC, North Africa, South Africa, Rest of Middle East & Africa), by Asia Pacific (China, India, Japan, South Korea, ASEAN, Oceania, Rest of Asia Pacific) Forecast 2025-2033

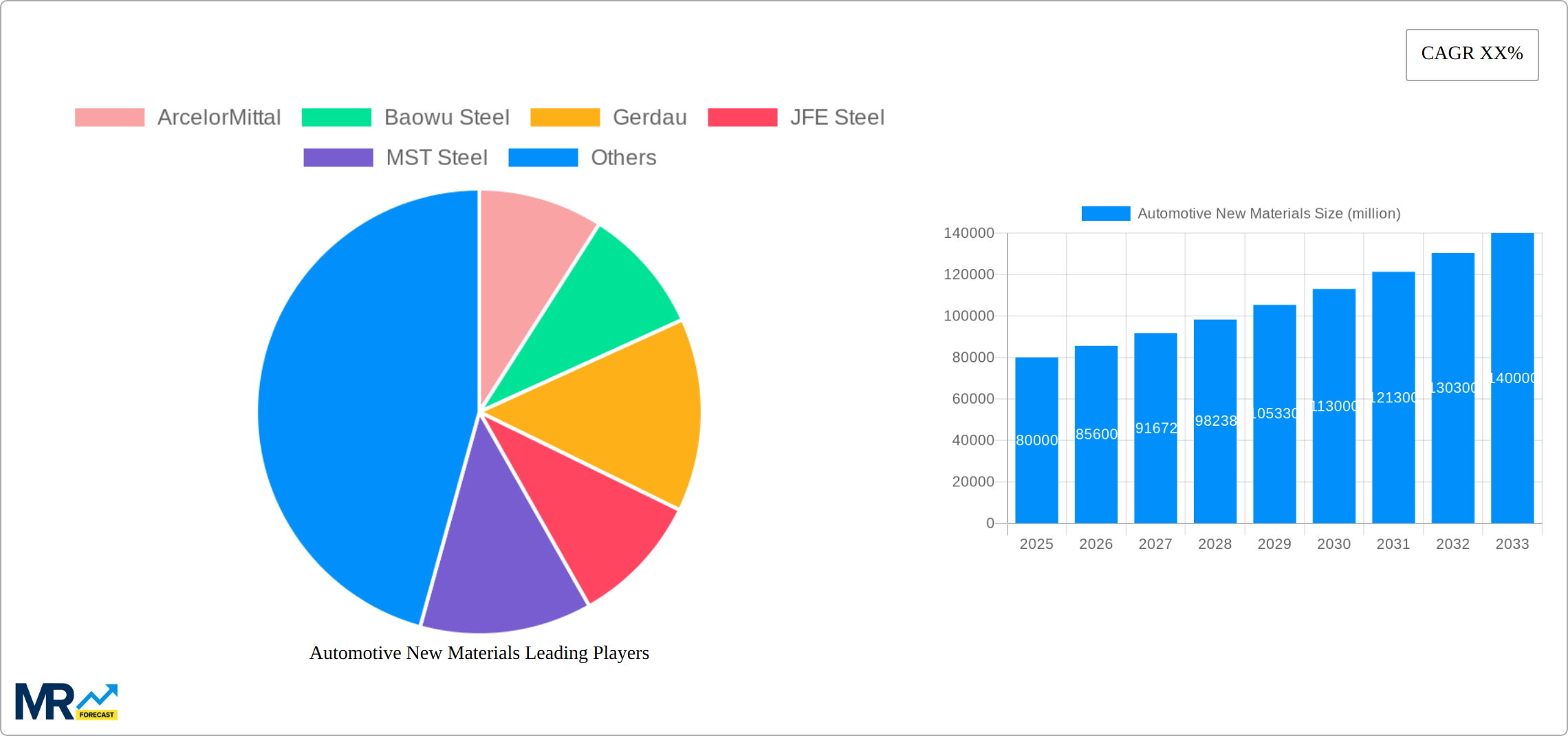

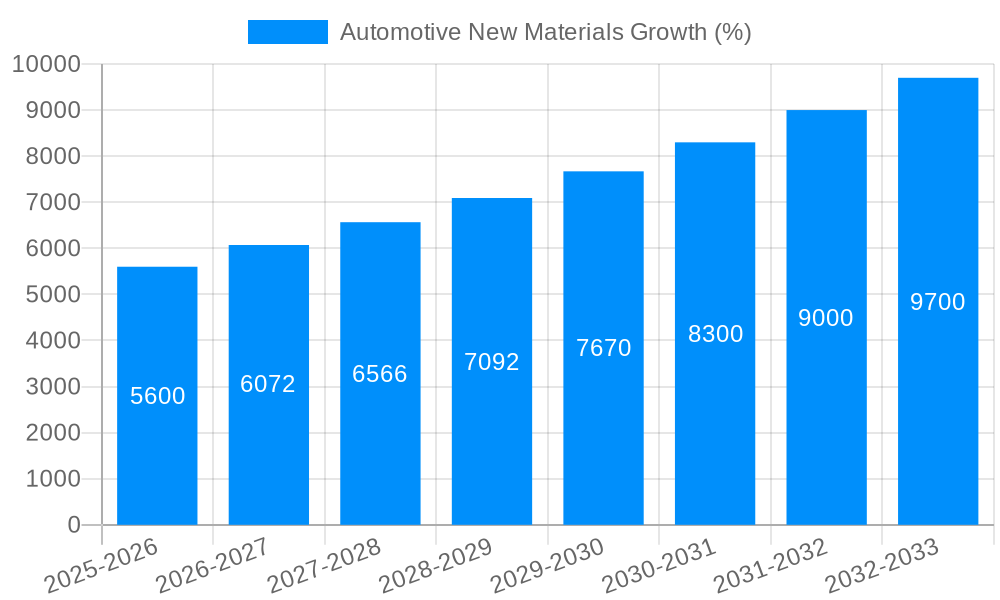

The automotive new materials market is experiencing robust growth, driven by the increasing demand for lightweight, high-strength, and sustainable materials in vehicle manufacturing. The shift towards electric vehicles (EVs) and stricter fuel efficiency regulations are key catalysts, necessitating the adoption of advanced materials like carbon fiber reinforced polymers (CFRP), aluminum alloys, and high-strength steel to reduce vehicle weight and improve performance. The market's expansion is further fueled by advancements in material science and manufacturing technologies, enabling the production of more cost-effective and high-performing materials. While the initial investment in new material adoption can be significant, the long-term benefits in terms of fuel efficiency, safety, and reduced emissions outweigh the costs, making it an attractive proposition for automotive manufacturers. We estimate the market size to be around $80 billion in 2025, growing at a Compound Annual Growth Rate (CAGR) of 7% between 2025 and 2033. This growth trajectory is underpinned by continuous innovation in material science and increasing governmental support for sustainable transportation solutions.

Major players like ArcelorMittal, Baowu Steel, and Nucor are at the forefront of innovation and production, actively investing in research and development to meet the evolving demands of the automotive industry. The market is segmented based on material type (steel, aluminum, polymers, etc.), vehicle type (passenger cars, commercial vehicles), and geographical region. Challenges such as the volatility of raw material prices and potential supply chain disruptions pose certain restraints. However, the ongoing focus on sustainability and the increasing adoption of advanced driver-assistance systems (ADAS) are expected to further propel the market's growth in the coming years. Regional variations exist, with North America and Europe currently holding significant market shares due to their established automotive industries and stricter emission regulations. However, rapidly developing economies in Asia-Pacific are expected to witness significant growth in the coming years.

The automotive industry is undergoing a dramatic transformation, driven by the increasing demand for lighter, stronger, and more sustainable vehicles. This shift is fueling significant growth in the automotive new materials market, projected to reach hundreds of billions of dollars by 2033. The historical period (2019-2024) witnessed a steady rise in adoption, primarily focused on materials offering improved fuel efficiency and enhanced safety features. The base year (2025) marks a critical juncture, with the market poised for exponential growth due to several converging factors. These include the escalating adoption of electric vehicles (EVs), the stringent emission regulations globally, and the growing emphasis on lightweighting to improve vehicle performance and range. The forecast period (2025-2033) anticipates substantial investments in research and development of advanced materials, such as high-strength steels, aluminum alloys, carbon fiber composites, and bio-based materials. This report provides a comprehensive analysis of these trends, focusing on market size and segmentation, examining the pivotal role played by key players like ArcelorMittal, Baowu Steel, and POSCO, whose strategic initiatives are shaping market dynamics. The market's evolution is not merely driven by technological advancements but also by consumer preferences for sustainable and environmentally friendly vehicles, further stimulating the growth of materials with a reduced carbon footprint. The estimated year (2025) data points to a significant surge in demand across various segments, driven by advancements in material science and innovative manufacturing processes. The study period (2019-2033) highlights the long-term trajectory of this dynamic market and its response to ongoing industry developments. The integration of new materials is not just a material science endeavor but also involves significant shifts in manufacturing processes and supply chains. This report unravels the complexities and the potential for disruptive innovations that will define the automotive new materials market in the coming years. The massive growth potential is underpinned by a confluence of technological leaps, regulatory pressures, and evolving consumer expectations. The market is witnessing a surge in the utilization of lightweight materials to enhance fuel efficiency and reduce emissions, significantly impacting the automotive landscape. This trend is likely to continue to shape the market’s trajectory in the years to come, contributing significantly to the overall expansion of the automotive new materials market. The projected growth is expected to create substantial opportunities for material suppliers, automotive manufacturers, and related businesses across the global value chain.

Several key factors are propelling the growth of the automotive new materials market. The most significant is the increasing demand for lighter vehicles to improve fuel efficiency and reduce emissions. This is particularly relevant in the context of stringent government regulations aimed at curbing greenhouse gas emissions and promoting sustainable transportation. The rise of electric vehicles (EVs) is another major driver, as EVs require specific materials with high energy density and lightweight properties to maximize range and performance. Furthermore, the growing focus on safety features in vehicles is leading to increased demand for high-strength and impact-resistant materials, enhancing occupant protection in the event of collisions. Advancements in material science and manufacturing processes are also contributing to the market's growth. The development of new materials with enhanced properties, such as higher strength-to-weight ratios and improved durability, is creating exciting opportunities for innovation in vehicle design and manufacturing. The cost-effectiveness of some of these new materials is also becoming increasingly competitive, making them more attractive to automotive manufacturers seeking to reduce production costs. Finally, growing consumer awareness of environmental concerns is pushing the demand for sustainable and recyclable materials, driving the adoption of bio-based and recycled materials in automotive manufacturing. These factors are collectively creating a powerful impetus for the growth of the automotive new materials market.

Despite the promising growth prospects, the automotive new materials market faces several challenges and restraints. One major hurdle is the high initial cost associated with the development and implementation of new materials. The research, development, and testing phases can be expensive, requiring significant investments from manufacturers and material suppliers. Another challenge lies in ensuring the consistent quality and performance of these new materials. The stringent quality standards and safety regulations within the automotive industry demand rigorous testing and verification processes, adding to the complexity and cost of adoption. The supply chain for these materials can also pose a challenge. Securing a stable and reliable supply of raw materials and components is critical, and disruptions in the supply chain can impact production timelines and overall costs. Furthermore, the integration of new materials into existing manufacturing processes can be complex and require significant modifications to existing equipment and infrastructure. Finally, the lack of awareness and understanding among automotive manufacturers about the benefits and applications of these new materials can hinder their widespread adoption. Overcoming these challenges requires collaborative efforts across the value chain, involving material suppliers, automotive manufacturers, and research institutions. Addressing these issues will be vital for unlocking the full potential of the automotive new materials market.

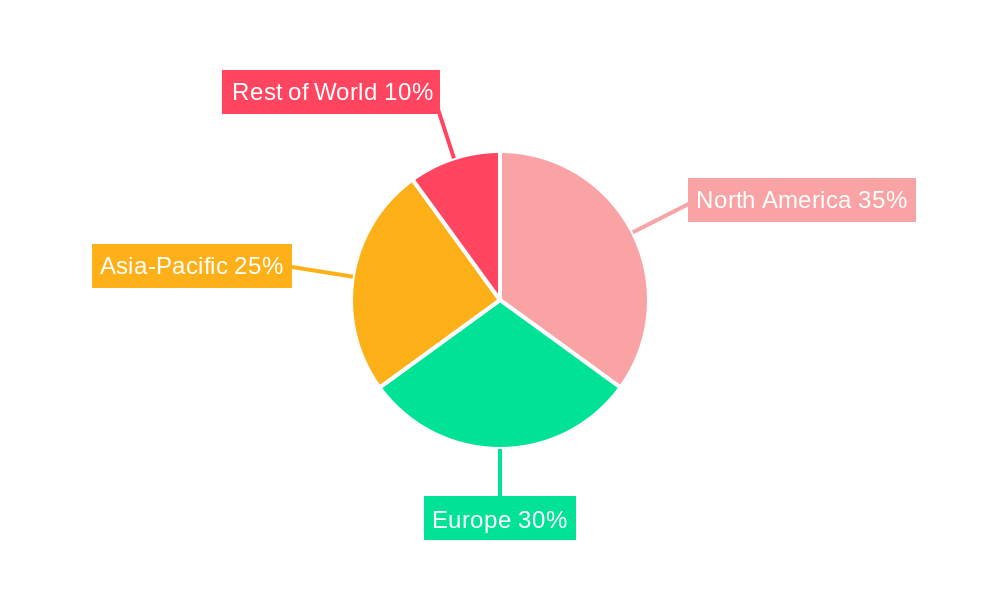

The automotive new materials market is characterized by significant regional variations in growth and adoption.

Asia Pacific: This region is anticipated to dominate the market due to the rapid growth of the automotive industry, particularly in countries like China, India, and Japan. The high volume of vehicle production and the increasing demand for fuel-efficient and environmentally friendly vehicles are driving the adoption of advanced materials in this region. Furthermore, significant government initiatives promoting the adoption of electric vehicles are also contributing to the growth of this market.

North America: North America holds a substantial market share, fueled by strong demand from the US and Canadian automotive industries. The region's focus on lightweighting and fuel efficiency, coupled with stringent emission regulations, is pushing the adoption of high-strength steels, aluminum alloys, and composites.

Europe: Europe exhibits robust growth potential, driven by its strong commitment to sustainability and stringent environmental regulations. The region is a frontrunner in the development and adoption of eco-friendly materials, including bio-based composites and recycled materials.

Segments:

High-Strength Steels: This segment is expected to hold a significant market share, driven by their cost-effectiveness and excellent mechanical properties. High-strength steels offer a good balance of strength, weight, and cost, making them suitable for various automotive applications.

Aluminum Alloys: Aluminum alloys are gaining traction due to their lightweight properties and excellent corrosion resistance. They are particularly favored in body panels and other structural components.

Carbon Fiber Composites: Despite their higher cost, carbon fiber composites are witnessing increasing demand due to their exceptional strength-to-weight ratio, enhancing vehicle performance and fuel efficiency. The development of cost-effective manufacturing processes is crucial to the expansion of this segment.

Magnesium Alloys: Magnesium alloys are gaining traction due to their extremely low density and high strength. However, their susceptibility to corrosion is a challenge that needs to be addressed.

Bio-Based Materials: The rising awareness of sustainability is boosting the market for bio-based materials. These materials offer reduced environmental impact and potentially improved recyclability.

The dominance of specific regions and segments is dynamically influenced by factors such as government policies, technological advancements, manufacturing capabilities, and consumer preferences. This dynamic interplay necessitates continuous monitoring and analysis to accurately forecast market trends.

The automotive new materials market is experiencing robust growth, primarily fueled by increasing demand for lightweight vehicles to enhance fuel efficiency and reduce emissions. Stringent government regulations promoting sustainable transportation further accelerate this trend. The rising popularity of electric vehicles (EVs) demands materials with high energy density and lightweight properties, driving innovation and adoption of new materials in this sector. Simultaneously, advances in material science and manufacturing processes continuously provide improved properties and cost-competitiveness for these new materials, making them increasingly attractive to the automotive industry.

This report offers a detailed analysis of the automotive new materials market, providing comprehensive insights into market trends, growth drivers, challenges, and opportunities. It covers key segments, regions, and leading players, offering valuable information for businesses involved in or interested in entering this dynamic market. The report encompasses historical data, current market size estimations, and future forecasts, enabling informed decision-making and strategic planning. The study utilizes a robust methodology, combining quantitative and qualitative data to provide a well-rounded and accurate representation of the market.

| Aspects | Details |

|---|---|

| Study Period | 2019-2033 |

| Base Year | 2024 |

| Estimated Year | 2025 |

| Forecast Period | 2025-2033 |

| Historical Period | 2019-2024 |

| Growth Rate | CAGR of XX% from 2019-2033 |

| Segmentation |

|

Note*: In applicable scenarios

Primary Research

Secondary Research

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence

The projected CAGR is approximately XX%.

Key companies in the market include ArcelorMittal, Baowu Steel, Gerdau, JFE Steel, MST Steel, NSSMC, Nucor, POSCO, Mohka, Impact Plastics, Hitachi, .

The market segments include Application, Type.

The market size is estimated to be USD XXX million as of 2022.

N/A

N/A

N/A

N/A

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3480.00, USD 5220.00, and USD 6960.00 respectively.

The market size is provided in terms of value, measured in million and volume, measured in K.

Yes, the market keyword associated with the report is "Automotive New Materials," which aids in identifying and referencing the specific market segment covered.

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

To stay informed about further developments, trends, and reports in the Automotive New Materials, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.