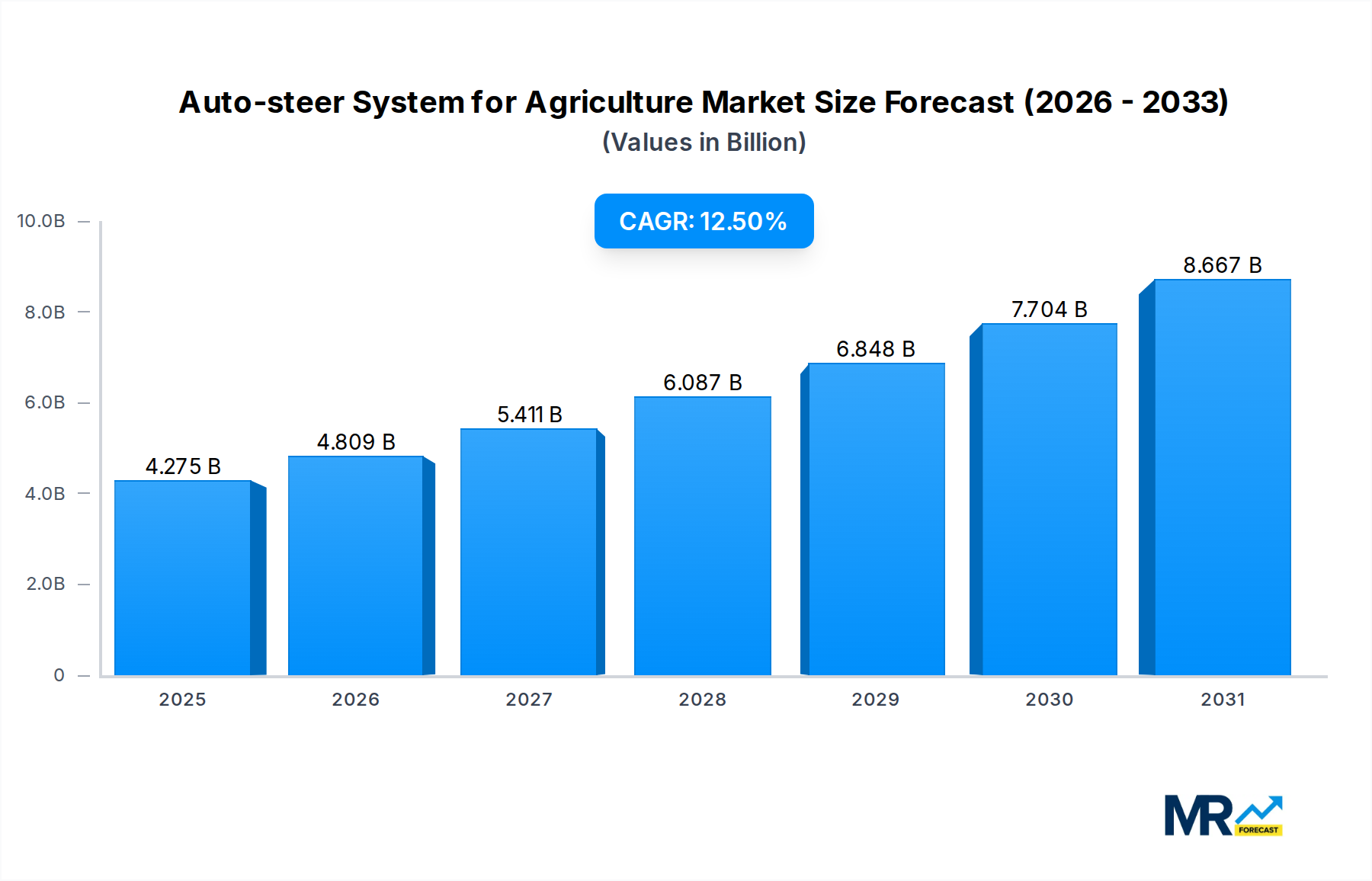

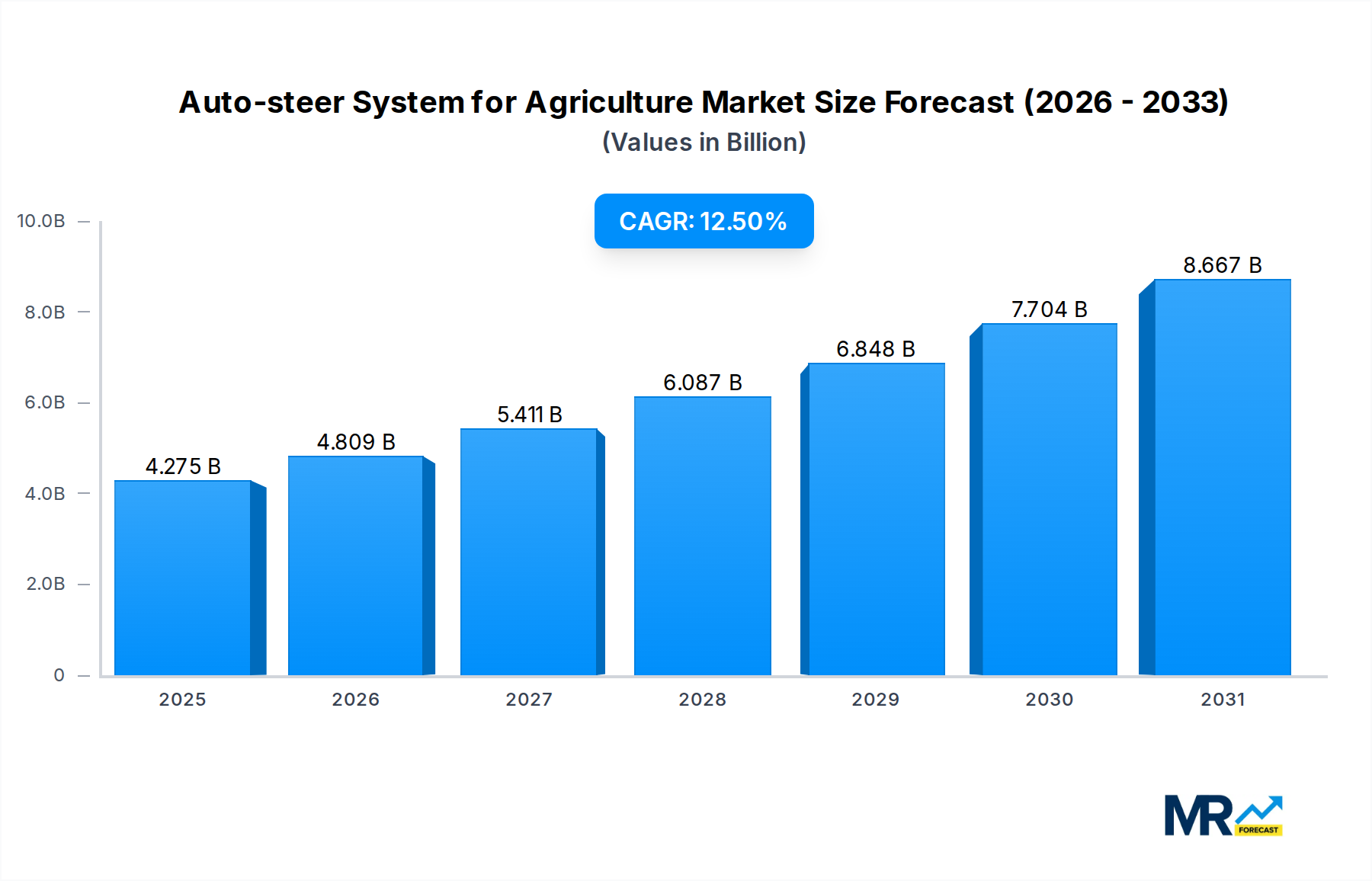

1. What is the projected Compound Annual Growth Rate (CAGR) of the Auto-steer System for Agriculture?

The projected CAGR is approximately 12.5%.

Auto-steer System for Agriculture

Auto-steer System for AgricultureAuto-steer System for Agriculture by Component (Hardware, Software), by Technology (GNSS-Based, RTK-Guided, Satellite-Based, Others), by Vehicle Type (Tractors, Harvesters, Sprayers, Seeders & Planters, Others), by Sales Channel (OEM, Aftermarket), by End User (Individual Farmers, Commercial Farming Enterprises, Agricultural Cooperatives, Others), by North America (United States, Canada, Mexico), by South America (Brazil, Argentina, Rest of South America), by Europe (United Kingdom, Germany, France, Italy, Spain, Russia, Benelux, Nordics, Rest of Europe), by Middle East & Africa (Turkey, Israel, GCC, North Africa, South Africa, Rest of Middle East & Africa), by Asia Pacific (China, India, Japan, South Korea, ASEAN, Oceania, Rest of Asia Pacific) Forecast 2026-2034

MR Forecast provides premium market intelligence on deep technologies that can cause a high level of disruption in the market within the next few years. When it comes to doing market viability analyses for technologies at very early phases of development, MR Forecast is second to none. What sets us apart is our set of market estimates based on secondary research data, which in turn gets validated through primary research by key companies in the target market and other stakeholders. It only covers technologies pertaining to Healthcare, IT, big data analysis, block chain technology, Artificial Intelligence (AI), Machine Learning (ML), Internet of Things (IoT), Energy & Power, Automobile, Agriculture, Electronics, Chemical & Materials, Machinery & Equipment's, Consumer Goods, and many others at MR Forecast. Market: The market section introduces the industry to readers, including an overview, business dynamics, competitive benchmarking, and firms' profiles. This enables readers to make decisions on market entry, expansion, and exit in certain nations, regions, or worldwide. Application: We give painstaking attention to the study of every product and technology, along with its use case and user categories, under our research solutions. From here on, the process delivers accurate market estimates and forecasts apart from the best and most meaningful insights.

Products generically come under this phrase and may imply any number of goods, components, materials, technology, or any combination thereof. Any business that wants to push an innovative agenda needs data on product definitions, pricing analysis, benchmarking and roadmaps on technology, demand analysis, and patents. Our research papers contain all that and much more in a depth that makes them incredibly actionable. Products broadly encompass a wide range of goods, components, materials, technologies, or any combination thereof. For businesses aiming to advance an innovative agenda, access to comprehensive data on product definitions, pricing analysis, benchmarking, technological roadmaps, demand analysis, and patents is essential. Our research papers provide in-depth insights into these areas and more, equipping organizations with actionable information that can drive strategic decision-making and enhance competitive positioning in the market.

The Auto-steer System for Agriculture Market is poised for substantial growth, driven by an escalating need for operational efficiency, enhanced precision, and optimized resource utilization within the global agricultural sector. Valued at an estimated $3.8 billion in 2024, the market is projected to expand at a robust Compound Annual Growth Rate (CAGR) of 12.5% over the forecast period, indicative of strong underlying demand and technological adoption. This growth trajectory is fundamentally supported by macro tailwinds such as increasing global food demand, diminishing availability of skilled agricultural labor, and rising input costs, which compel farmers to invest in advanced automation solutions.

Technological advancements, particularly in GNSS (Global Navigation Satellite System) accuracy and the integration of artificial intelligence (AI) and machine learning (ML), are significant drivers. The proliferation of RTK (Real-Time Kinematic) guided systems, offering sub-inch precision, is transforming farming practices from planting to harvesting. These systems enable farmers to minimize overlap, reduce fuel consumption, optimize fertilizer and pesticide application, and improve overall yield. The demand for these sophisticated solutions is further fueled by government initiatives and subsidies promoting sustainable farming practices and digital transformation in agriculture, contributing to the expansion of the broader Precision Agriculture Market.

The market landscape is characterized by intense competition among established agricultural machinery manufacturers and specialized technology providers. Key players are focusing on developing integrated platforms that offer seamless connectivity between different farm operations and data analytics capabilities. The adoption of auto-steer systems is not limited to large commercial farming enterprises; increasing affordability and ease of use are also expanding their reach to individual farmers and agricultural cooperatives. This democratization of advanced agricultural technology is a critical factor influencing market dynamics. Furthermore, the rising awareness regarding environmental sustainability and the pressure to reduce the ecological footprint of farming operations are accelerating the adoption of precision guidance systems. The synergy between auto-steer technology and other emerging solutions within the Agricultural Robotics Market and the Smart Farming Market is creating new avenues for innovation and growth, promising a future of increasingly autonomous and data-driven agricultural production.

The Hardware segment continues to hold a dominant share within the Auto-steer System for Agriculture Market, serving as the foundational infrastructure for all precision guidance operations. This segment encompasses critical components such as GPS/GNSS Receivers, Steering Controllers, Sensors, Displays & Monitors, and Antennas. The intrinsic nature of auto-steer technology, requiring robust physical components for accurate positioning, control, and user interface, ensures the hardware segment's significant revenue contribution. GPS/GNSS Receivers, for instance, are indispensable, providing the precise location data necessary for guiding agricultural machinery. Advancements in multi-constellation and multi-frequency GNSS receivers, capable of leveraging signals from GPS, GLONASS, Galileo, and BeiDou, have dramatically improved accuracy and reliability, even in challenging environments. The increasing demand for RTK-guided systems, which rely on base stations or network corrections to achieve centimeter-level accuracy, further solidifies the market position of high-precision GNSS Receivers Market products.

Steering Controllers are another vital hardware component, translating the positioning data into mechanical steering commands for the vehicle. These controllers range from assisted steering systems, which provide torque to the steering wheel, to fully integrated hydraulic control systems that directly manipulate the vehicle's steering mechanism. The sophistication and integration capabilities of these controllers are continuously evolving, driven by the need for seamless operation across diverse Farm Equipment Market types. Sensors, including accelerometers, gyroscopes, and terrain compensation sensors, play a crucial role in enhancing the accuracy and stability of auto-steer systems, particularly on uneven terrain or during turns. These Agricultural Sensors Market units provide real-time feedback, allowing the system to adjust steering inputs dynamically and maintain the desired path. Displays & Monitors serve as the human-machine interface, allowing operators to set parameters, monitor system performance, and visualize coverage maps. The trend towards larger, more intuitive touch-screen displays with advanced mapping and data logging capabilities further contributes to this segment's value.

The dominance of the hardware segment is also attributable to the high initial capital investment required for these sophisticated components. While software and service subscriptions represent recurring revenue streams, the upfront cost of physical hardware remains substantial. Key players such as John Deere, Trimble, and Topcon Positioning Systems are prominent in this segment, continually innovating to deliver more accurate, reliable, and integrated hardware solutions. Their ongoing R&D efforts focus on miniaturization, ruggedization, and seamless integration with existing farm machinery, enhancing the overall value proposition. As the Auto-steer System for Agriculture Market matures, there is a strong trend towards modular hardware designs that allow for upgrades and compatibility across different vehicle types, ensuring that the hardware segment will maintain its leading position due to its foundational role in enabling precision agricultural operations.

The Auto-steer System for Agriculture Market is propelled by several critical drivers, each substantiated by observable market trends and economic realities. A primary driver is the escalating global demand for enhanced operational efficiency and yield optimization. Farmers are increasingly under pressure to produce more food with fewer resources. For example, auto-steer systems can reduce overlap in field operations by 5-10%, translating directly into reduced fuel consumption, less wear and tear on machinery, and optimized use of inputs like seeds, fertilizers, and pesticides. This efficiency gain contributes significantly to higher crop yields and profitability per acre, making precision agriculture technologies an attractive investment despite initial costs.

Another significant driver is increasing labor scarcity and rising labor costs in the agricultural sector across many developed and rapidly developing economies. In regions like North America and Europe, the agricultural labor force has seen a steady decline, while wages for skilled farm workers have risen. Auto-steer systems mitigate this challenge by reducing the manual steering burden on operators, allowing them to focus on other tasks, enabling longer working hours with less fatigue, and potentially reducing the number of operators needed for certain tasks. This directly addresses a critical pain point for farm owners, where labor represents a substantial and often volatile operational cost.

Despite these compelling drivers, the market faces notable adoption hurdles. A significant constraint is the high initial investment associated with advanced auto-steer systems. While basic systems can be relatively affordable, RTK-guided systems offering sub-inch accuracy can cost tens of thousands of dollars, representing a substantial capital outlay for individual farmers. This high entry barrier can deter small and medium-sized farms, particularly in regions with limited access to agricultural credit or government subsidies. The return on investment, while substantial over time, may not be immediately apparent, requiring a longer payback period that some farmers are unwilling or unable to accommodate.

A further hurdle is the technical complexity and the requisite need for skilled personnel to operate, maintain, and troubleshoot these advanced systems. Integrating auto-steer technology with existing farm machinery, understanding GNSS correction signals, and calibrating sensors require a certain level of technical proficiency. The lack of adequate training and support infrastructure in some rural areas can create an adoption gap, as farmers may be hesitant to invest in technology they cannot fully utilize or maintain. Bridging this skill gap through comprehensive training programs and robust technical support networks is crucial for overcoming this adoption barrier and expanding the reach of the Auto-steer System for Agriculture Market.

The Auto-steer System for Agriculture Market is characterized by a mix of established agricultural machinery giants and specialized technology firms, all vying for market share through innovation, strategic partnerships, and robust service offerings.

Q4 2023: John Deere announced the expansion of its See & Spray Ultimate technology, integrating advanced computer vision and machine learning with auto-steer systems to target individual weeds with greater precision, significantly reducing herbicide use. This innovation further solidifies their position in the Precision Agriculture Market. Q3 2023: Trimble introduced its new GFX-1060 and GFX-1260 displays, enhancing the user interface and processing power for auto-steer operations. These displays offer improved compatibility with third-party implements and support advanced guidance patterns, aiming to streamline farm operations. Q2 2023: Topcon Positioning Systems partnered with a leading agricultural equipment manufacturer to integrate its AGI-4 GNSS receiver and AES-35 electric steering system as an OEM factory-fit option, expanding the reach of its high-accuracy solutions directly into new machinery lines. Q1 2023: Ag Leader Technology released an update to its InCommand displays and SteerCommand Z2 auto-steer system, introducing new features for headland management and enhanced RTK signal stability, providing farmers with more reliable and efficient guidance. Q4 2022: Raven Industries unveiled new enhancements to its Slingshot RTK correction services, aiming to provide broader coverage and improved signal reliability across North America, which is critical for maintaining sub-inch accuracy for auto-steer applications. Q3 2022: CNH Industrial's Case IH brand launched new upgrades for its AFS AccuGuide auto-steer system, focusing on tighter integration with their combine harvesters and sprayers, enabling autonomous steering during more complex field operations. This development contributes to the expansion of the Tractor Automation Market beyond just tractors. Q2 2022: FJDynamics, an emerging player, expanded its distribution network across Europe and South America, making its cost-effective auto-steer retrofit kits more accessible to a wider range of farmers looking to adopt precision agriculture technologies without major capital expenditure. Q1 2022: Hexagon Agriculture launched a new cloud-based data management platform designed to seamlessly integrate data from auto-steer systems, offering enhanced analytics and decision-making tools for farmers. This platform highlights the growing importance of Agricultural Software Market solutions in the ecosystem.

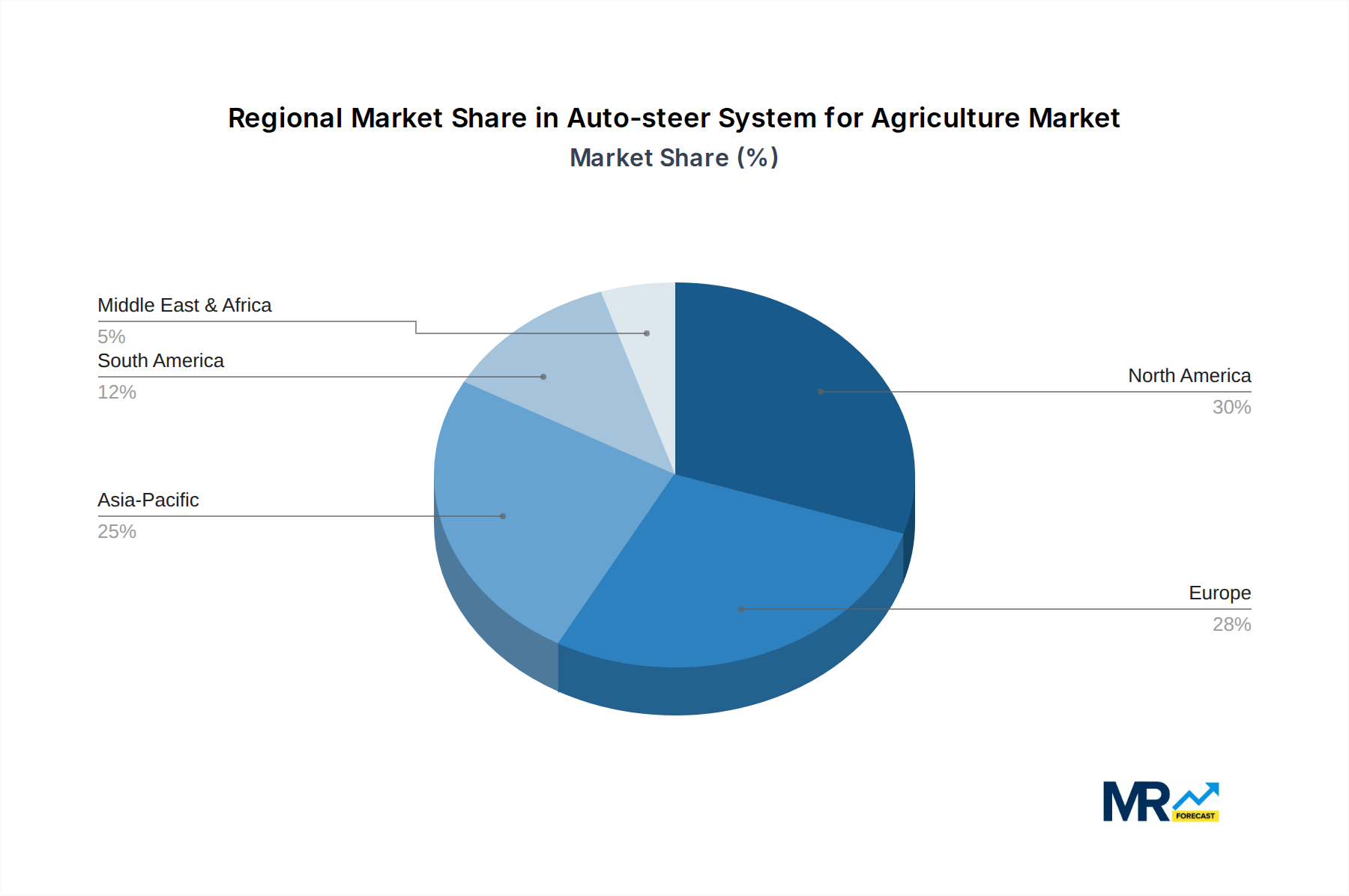

The global Auto-steer System for Agriculture Market exhibits distinct regional dynamics, influenced by varying levels of agricultural modernization, farm sizes, labor costs, and government support. North America currently holds the largest revenue share in the market, primarily driven by the presence of large commercial farming enterprises, high adoption rates of precision agriculture technologies, and significant investments in smart farming solutions. Farmers in the United States and Canada benefit from advanced infrastructure for GNSS correction services and a proactive approach to adopting efficiency-enhancing technologies. The region's focus on maximizing yields and combating rising labor costs acts as a major demand driver, with a mature but continuously innovating market. The region is expected to maintain its leadership, albeit with a slightly slower CAGR compared to emerging regions, as adoption reaches saturation in some segments.

Europe represents another significant market, characterized by stringent environmental regulations, a strong emphasis on sustainable agriculture, and government subsidies promoting precision farming techniques. Countries like Germany, France, and the UK are rapid adopters, driven by the need to optimize input usage and comply with ecological mandates. The market here is mature, similar to North America, with a consistent demand for advanced RTK-guided systems to enhance operational precision and reduce environmental impact. The fragmented nature of European farms, however, sometimes necessitates more tailored, scalable solutions.

Asia Pacific is projected to be the fastest-growing region in the Auto-steer System for Agriculture Market, exhibiting a high CAGR over the forecast period. This growth is fueled by the rapid modernization of agriculture in countries like China, India, and Australia, coupled with increasing government support for agricultural mechanization and the rising awareness among farmers about the benefits of precision farming. The region's vast agricultural land, growing population, and increasing labor costs are strong incentives for adopting auto-steer systems. While still developing in terms of overall market size compared to North America and Europe, the tremendous potential for new adoption and expansion makes Asia Pacific a key growth engine for the market. The burgeoning IoT in Agriculture Market in this region is also contributing to the demand for connected auto-steer solutions.

South America, particularly Brazil and Argentina, is emerging as another high-growth region. The extensive land available for cultivation, the presence of large-scale commercial farms, and the focus on increasing agricultural productivity for export are driving the adoption of auto-steer systems. As the region continues to invest in modernizing its agricultural infrastructure and improving efficiency, the demand for precision guidance technologies is expected to rise sharply, making it a critical market for future expansion. The drive to boost competitiveness in the global commodities market is a key demand driver here, contributing to the growth of the broader Agricultural Robotics Market.

The supply chain for the Auto-steer System for Agriculture Market is complex, relying heavily on specialized electronic components and refined raw materials. Upstream dependencies include manufacturers of semiconductors, particularly for GNSS receivers, steering controllers, and displays. The global semiconductor shortage, a recent historical disruption, significantly impacted the production timelines and costs of auto-steer systems, leading to extended lead times for agricultural machinery and component availability. This highlights a critical sourcing risk associated with concentrated manufacturing bases and geopolitical stability in key semiconductor-producing regions.

Key raw materials include rare earth elements for advanced magnet motors used in electric steering systems, specialized plastics and composites for housings and protective casings, and various metals such as copper for wiring and circuit boards, and aluminum for chassis and mounting hardware. The price volatility of these inputs, particularly rare earth elements and silicon, can directly influence the manufacturing costs and, consequently, the final pricing of auto-steer solutions. For example, fluctuations in the market price of neodymium (a rare earth element) can impact the cost of high-torque electric motors essential for retrofit auto-steer kits. Similarly, the trend in silicon prices directly affects the cost of microprocessors and memory components, which are integral to the system's processing capabilities.

Geopolitical tensions and trade tariffs can also disrupt the flow of these critical materials, adding to supply chain risks. Manufacturers in the Auto-steer System for Agriculture Market must navigate a delicate balance between cost-effectiveness and supply chain resilience, often leading to dual-sourcing strategies or vertical integration where feasible. Historically, disruptions have led to increased inventory holding costs, production delays, and upward pressure on component prices. The drive towards more robust and ruggedized systems for the agricultural environment also places specific demands on material properties, requiring advanced alloys and polymers that can withstand harsh conditions, further influencing sourcing decisions and material costs. Moreover, the increasing sophistication of Agricultural Sensors Market components introduces dependencies on specialized MEMS (Micro-Electro-Mechanical Systems) and other advanced sensing technologies, often produced by a limited number of global suppliers.

Customer segmentation in the Auto-steer System for Agriculture Market primarily revolves around farm size, operational scope, and technological readiness, influencing buying behavior and procurement channels. Individual Farmers, often operating smaller to medium-sized farms, represent a segment that is typically more price-sensitive and seeks solutions that offer a clear and rapid return on investment. Their purchasing criteria often prioritize ease of use, compatibility with existing machinery, and robust after-sales support. They tend to favor aftermarket solutions or entry-level OEM systems that can be retrofitted. Price sensitivity here is moderate to high, often leading to decisions based on direct cost savings on fuel, inputs, and labor. They also show growing interest in the IoT in Agriculture Market for integrated farm management.

Commercial Farming Enterprises, encompassing large-scale corporate farms or vertically integrated agricultural businesses, constitute a major segment with distinct buying behaviors. These enterprises prioritize accuracy, reliability, and seamless integration of auto-steer systems with comprehensive farm management platforms. Their purchasing criteria include advanced features like multi-machine coordination, remote monitoring, and sophisticated data analytics capabilities provided by the Agricultural Software Market. Price sensitivity is lower compared to individual farmers, as the investment is seen as a strategic operational enhancement with long-term benefits for efficiency and scalability. They predominantly procure through OEM channels, seeking fully integrated solutions and often negotiating bulk purchase agreements or fleet discounts. This segment is a significant driver for the high-end Precision Agriculture Market.

Agricultural Cooperatives represent another segment, pooling resources and expertise for their members. Their buying behavior is often influenced by collective benefits, seeking cost-effective solutions that can be shared or utilized across multiple member farms. Procurement decisions often balance performance with affordability and ease of maintenance across a diverse range of Farm Equipment Market types. They might opt for a mix of OEM and aftermarket solutions, prioritizing training and technical support for their member base. These cooperatives are also keen on solutions that contribute to overall regional productivity and sustainability goals, driving demand for innovations within the Smart Farming Market.

Notable shifts in buyer preference in recent cycles include a growing demand for subscription-based models for RTK correction services and Agricultural Software Market, reducing the upfront cost of ownership. There's also an increasing preference for integrated solutions that offer interoperability between different farm implements and data platforms, moving away from siloed technologies. The emphasis on user-friendly interfaces and robust connectivity, often via telematics, has also become a stronger purchasing criterion across all segments, reflecting the broader digital transformation in agriculture.

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 12.5% from 2020-2034 |

| Segmentation |

|

Note*: In applicable scenarios

Primary Research

Secondary Research

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence

The projected CAGR is approximately 12.5%.

Key companies in the market include John Deere, Trimble, Topcon Positioning Systems, Ag Leader Technology, Raven Industries, AgJunction, Patchwork, CNH Industrial, AGCO Corporation, FieldBee, ARAG, Homburg Holland, Sveaverken Svea Agri, Geometer International, Hexagon Agriculture, Reichhardt, Rostselmash, FJDynamics, SMAJAYU(SHENZHEN), ComNav Technology, CP Device.

The market segments include Component, Technology, Vehicle Type, Sales Channel, End User.

The market size is estimated to be USD 3.8 billion as of 2022.

N/A

N/A

N/A

N/A

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4480.00, USD 6720.00, and USD 8960.00 respectively.

The market size is provided in terms of value, measured in billion and volume, measured in K.

Yes, the market keyword associated with the report is "Auto-steer System for Agriculture," which aids in identifying and referencing the specific market segment covered.

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

To stay informed about further developments, trends, and reports in the Auto-steer System for Agriculture, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.