1. What is the projected Compound Annual Growth Rate (CAGR) of the Auto Parts Production Logistics?

The projected CAGR is approximately 8.1%.

Auto Parts Production Logistics

Auto Parts Production LogisticsAuto Parts Production Logistics by Type (Road Transport, Rail Transport, Waterway Transport, Airway Transport), by Application (Automotive Manufacturers, Auto Parts Supplier), by North America (United States, Canada, Mexico), by South America (Brazil, Argentina, Rest of South America), by Europe (United Kingdom, Germany, France, Italy, Spain, Russia, Benelux, Nordics, Rest of Europe), by Middle East & Africa (Turkey, Israel, GCC, North Africa, South Africa, Rest of Middle East & Africa), by Asia Pacific (China, India, Japan, South Korea, ASEAN, Oceania, Rest of Asia Pacific) Forecast 2026-2034

MR Forecast provides premium market intelligence on deep technologies that can cause a high level of disruption in the market within the next few years. When it comes to doing market viability analyses for technologies at very early phases of development, MR Forecast is second to none. What sets us apart is our set of market estimates based on secondary research data, which in turn gets validated through primary research by key companies in the target market and other stakeholders. It only covers technologies pertaining to Healthcare, IT, big data analysis, block chain technology, Artificial Intelligence (AI), Machine Learning (ML), Internet of Things (IoT), Energy & Power, Automobile, Agriculture, Electronics, Chemical & Materials, Machinery & Equipment's, Consumer Goods, and many others at MR Forecast. Market: The market section introduces the industry to readers, including an overview, business dynamics, competitive benchmarking, and firms' profiles. This enables readers to make decisions on market entry, expansion, and exit in certain nations, regions, or worldwide. Application: We give painstaking attention to the study of every product and technology, along with its use case and user categories, under our research solutions. From here on, the process delivers accurate market estimates and forecasts apart from the best and most meaningful insights.

Products generically come under this phrase and may imply any number of goods, components, materials, technology, or any combination thereof. Any business that wants to push an innovative agenda needs data on product definitions, pricing analysis, benchmarking and roadmaps on technology, demand analysis, and patents. Our research papers contain all that and much more in a depth that makes them incredibly actionable. Products broadly encompass a wide range of goods, components, materials, technologies, or any combination thereof. For businesses aiming to advance an innovative agenda, access to comprehensive data on product definitions, pricing analysis, benchmarking, technological roadmaps, demand analysis, and patents is essential. Our research papers provide in-depth insights into these areas and more, equipping organizations with actionable information that can drive strategic decision-making and enhance competitive positioning in the market.

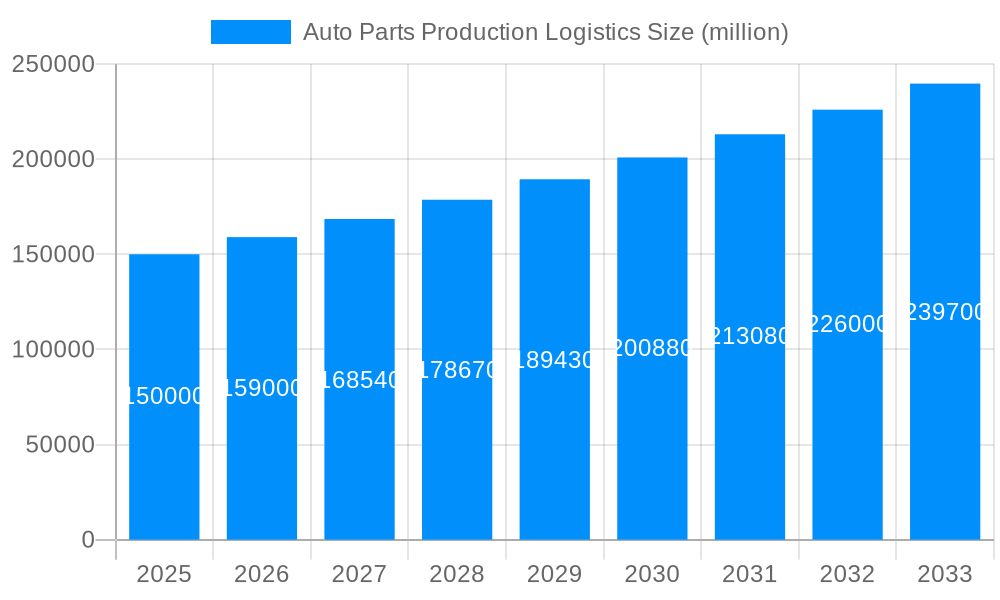

The global automotive parts production logistics market is poised for significant expansion, propelled by a thriving automotive sector and increasingly intricate worldwide supply chains. The market is projected to reach $249.2 billion by 2025, demonstrating a Compound Annual Growth Rate (CAGR) of 8.1% from a base year of 2025. This growth trajectory is underpinned by several pivotal factors. Foremost is the imperative of just-in-time (JIT) manufacturing, demanding agile and dependable logistics to ensure punctual component delivery to assembly facilities. Secondly, the escalating adoption of electric vehicles (EVs) and autonomous vehicles (AVs) introduces unique logistical requirements for specialized components. Thirdly, ongoing globalization necessitates advanced logistics networks for cross-continental part movement. The market is segmented by transportation mode (road, rail, sea, air) and application (automotive manufacturers, auto parts suppliers). While road transport currently leads due to its flexibility, rail and sea transport are gaining prominence for their sustainability and cost-effectiveness in long-haul operations. Emerging economies with burgeoning automotive industries, such as India and Southeast Asia, represent key geographic growth areas.

Notwithstanding a positive outlook, the market encounters challenges including volatile fuel prices, geopolitical uncertainties, and persistent semiconductor shortages, which can disrupt supply chains and escalate transportation expenditures. Heightened environmental regulations are also compelling investments in sustainable logistics technologies and infrastructure. Key industry participants are prioritizing advancements in automation, artificial intelligence, and blockchain to enhance supply chain efficiency, transparency, and traceability. The market is characterized by a fragmented competitive landscape with a mix of global and regional logistics providers. Strategic collaborations, mergers, acquisitions, and continuous innovation in logistics solutions will define the future of this market.

The global auto parts production logistics market is experiencing a period of significant transformation, driven by the burgeoning automotive industry and the increasing complexity of supply chains. Over the study period (2019-2033), the market witnessed a substantial upswing, exceeding 200 million units in 2024. This growth is projected to continue, with forecasts indicating a market value exceeding 300 million units by 2033. Key market insights reveal a strong preference for efficient, just-in-time delivery systems to minimize inventory holding costs and optimize production schedules. The rising adoption of advanced technologies like AI-powered route optimization and predictive analytics is streamlining logistics operations, leading to reduced transportation costs and improved delivery times. Furthermore, the increasing focus on sustainability is prompting the adoption of eco-friendly transportation modes and packaging solutions, adding another layer of complexity and cost to the overall logistics process. The market is also witnessing a shift towards greater collaboration between automotive manufacturers, parts suppliers, and logistics providers to enhance visibility and improve coordination across the supply chain. This collaborative approach is crucial for navigating the challenges posed by global trade uncertainties, fluctuating fuel prices, and increasing regulatory pressures. The ongoing trend towards electric vehicle (EV) production further influences the logistics landscape, requiring specialized handling and transportation solutions for batteries and other components. This shift necessitates flexible and adaptable logistics solutions that can respond effectively to the dynamic needs of the ever-evolving automotive industry. The base year for this analysis is 2025, with estimations for the same year and forecasts spanning 2025-2033. The historical period considered covers 2019-2024, providing a robust foundation for the projections.

Several factors are significantly propelling the growth of the auto parts production logistics market. The global expansion of the automotive industry, particularly in emerging markets, is creating a substantial demand for efficient and reliable logistics solutions. Manufacturers are increasingly outsourcing logistics functions to specialized third-party logistics (3PL) providers to focus on core competencies and leverage the expertise of experienced logistics operators. This outsourcing trend is further amplified by the rising adoption of lean manufacturing principles, which prioritize just-in-time inventory management and streamlined supply chains. Technological advancements, such as the Internet of Things (IoT), blockchain technology, and advanced analytics, are enhancing supply chain visibility, improving inventory management, and optimizing transportation routes. The increasing demand for customization and personalization in the automotive industry necessitates flexible and agile logistics solutions that can effectively handle diverse product configurations and delivery schedules. Moreover, the growing pressure to reduce environmental impact is driving the adoption of sustainable transportation modes and packaging solutions, pushing logistics providers to innovate and optimize their operations for improved efficiency and reduced carbon footprint. Finally, governmental regulations and trade policies are influencing the logistics landscape, requiring companies to adapt to changing requirements and optimize their supply chains for regulatory compliance.

The auto parts production logistics sector faces several challenges. Fluctuating fuel prices and geopolitical instability significantly impact transportation costs and lead times, making it difficult for companies to accurately forecast and manage their logistics budgets. The increasing complexity of global supply chains, coupled with rising regulatory requirements, creates operational hurdles and compliance challenges. Supply chain disruptions, such as natural disasters, pandemics, and port congestion, can severely impact the availability of parts and disrupt production schedules. The demand for just-in-time inventory management necessitates highly accurate forecasting and precise logistics execution; any deviations can lead to significant production delays and financial losses. Moreover, the shortage of skilled labor in the logistics sector hinders efficient operations and poses a significant challenge for companies seeking to expand their logistics capabilities. Furthermore, security concerns and the risk of theft or damage to valuable auto parts during transit require robust security measures and sophisticated tracking systems, adding to the overall cost and complexity of logistics operations. Finally, the need for sustainable and environmentally friendly practices necessitates investments in new technologies and infrastructure, representing a significant capital outlay for logistics providers.

Dominant Segment: Road Transport continues to be the dominant mode of transportation for auto parts due to its flexibility, accessibility, and relatively lower cost compared to other modes for shorter distances. This segment's dominance is expected to persist throughout the forecast period, although the share might decrease slightly due to the increased adoption of rail and waterway transport for long-distance hauls.

Dominant Application: Automotive Manufacturers represent the largest consumer of auto parts logistics services, driving a significant portion of the market demand. Their requirement for timely delivery of parts to assembly lines makes them highly reliant on efficient and reliable logistics providers. However, the Auto Parts Supplier segment is showing notable growth, fueled by the rising trend of outsourcing logistics operations.

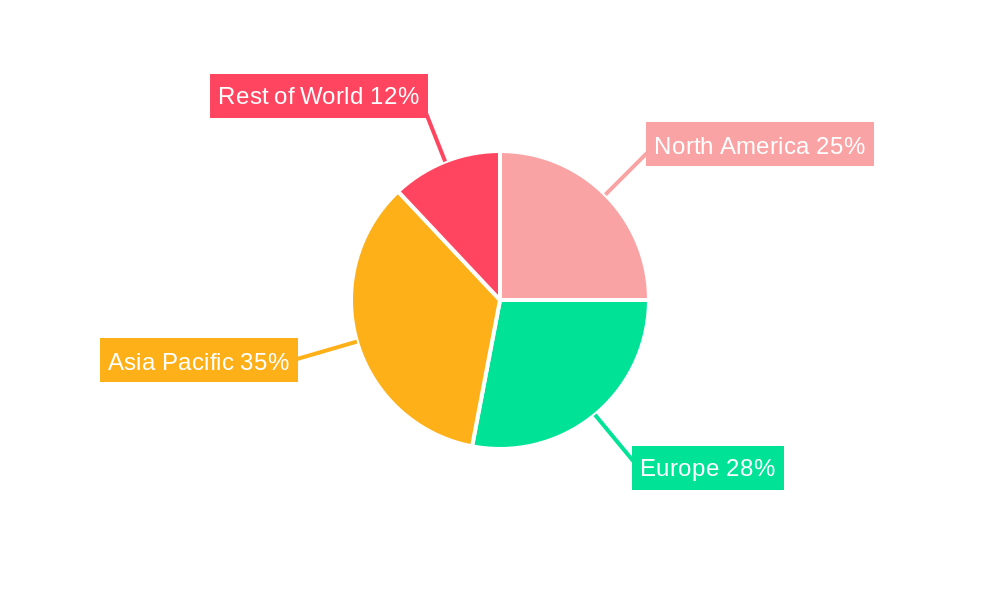

Dominant Region (Example): China, with its massive automotive manufacturing industry and extensive network of auto parts suppliers, is projected to maintain its leading position in the auto parts production logistics market. The vast scale of production and the expanding network of transportation infrastructure create favorable conditions for growth in this region. Similarly, other major automotive manufacturing hubs like North America and Europe are also expected to witness significant growth, albeit at a slightly slower pace compared to China. The growth in these regions is driven by robust automotive production and rising demand for efficient supply chain solutions.

The substantial growth within the road transport segment is driven primarily by the need for timely and flexible delivery solutions. Its versatility in handling different types of cargo and its extensive reach across various regions provide an edge over other transportation methods. In contrast, rail and waterway transport find more application in long-distance hauls, particularly for large-volume shipments. However, these modes often encounter challenges related to infrastructure limitations, accessibility, and transit times, resulting in a smaller overall market share. Airway transport finds its niche in the delivery of high-value, time-sensitive parts, where speed is paramount. However, its high cost limits its widespread adoption for large-scale auto part shipments.

The auto parts production logistics market is poised for robust growth, propelled by the increasing adoption of advanced technologies, heightened focus on supply chain optimization, and the growing demand for sustainable and eco-friendly logistics solutions. These combined factors create a fertile ground for innovation and expansion within the industry, leading to a surge in efficiency and cost-effectiveness. The global expansion of the automotive industry, especially in emerging markets, is creating new opportunities for logistics providers to capitalize on.

This report provides a comprehensive overview of the auto parts production logistics market, analyzing market trends, driving forces, challenges, key players, and significant developments. It offers detailed insights into the market dynamics, including segmentation analysis by transportation mode and application, regional market outlook, and growth catalysts. The report's findings are based on extensive research and data analysis, providing valuable insights for industry stakeholders seeking to navigate the complex and evolving landscape of auto parts logistics.

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 8.1% from 2020-2034 |

| Segmentation |

|

Note*: In applicable scenarios

Primary Research

Secondary Research

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence

The projected CAGR is approximately 8.1%.

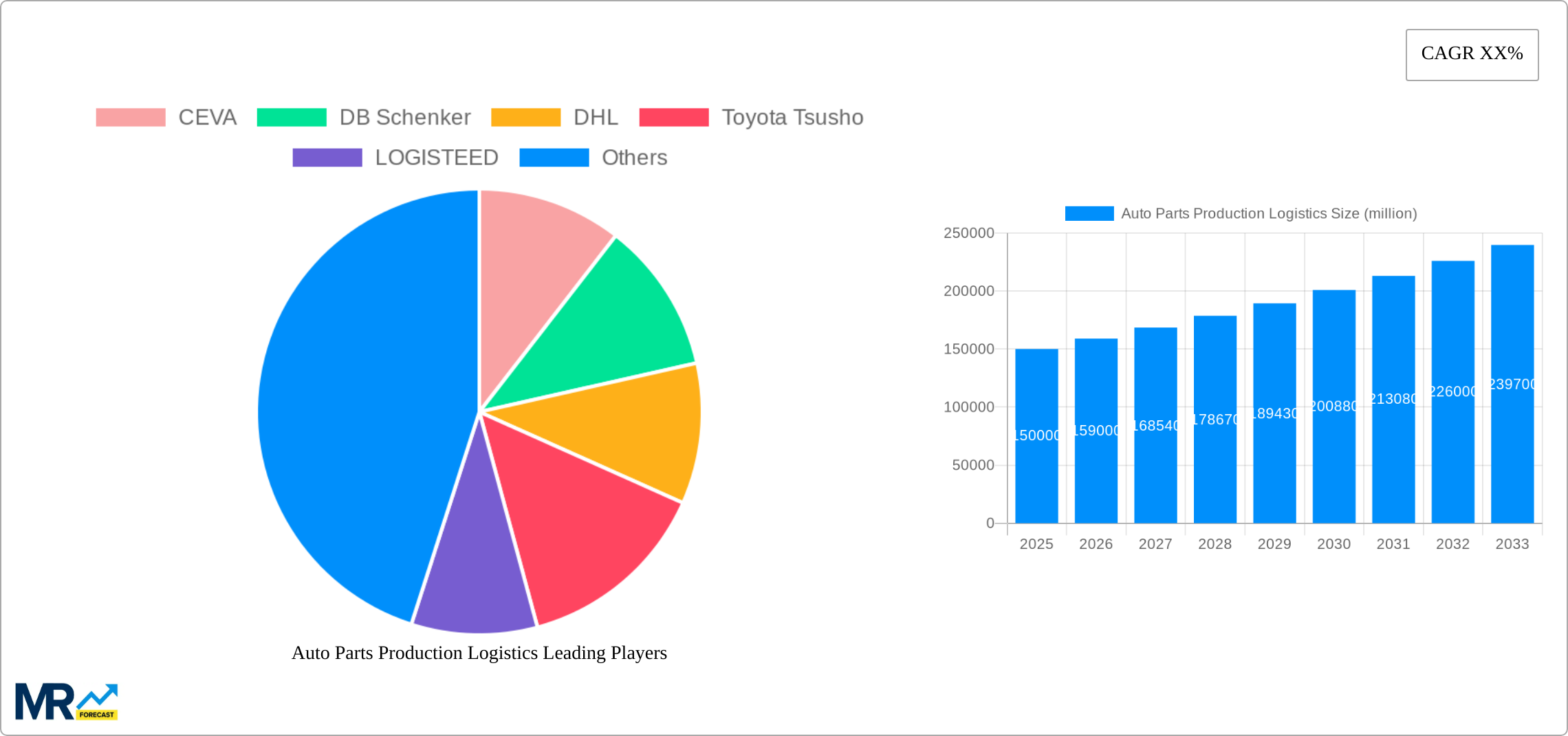

Key companies in the market include CEVA, DB Schenker, DHL, Toyota Tsusho, LOGISTEED, Expeditors International, UPS, Nippon Express, Ryder System, Bolloré Logistics, Kuehne+Nagel, A.P. Moller-Maersk Group, DSV, BLG LOGISTICS, C.H. Robinson, FAW Logistics, SAIC Anji Logistics, Changan Minsheng APLL Logistics, .

The market segments include Type, Application.

The market size is estimated to be USD 249.2 billion as of 2022.

N/A

N/A

N/A

N/A

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3480.00, USD 5220.00, and USD 6960.00 respectively.

The market size is provided in terms of value, measured in billion.

Yes, the market keyword associated with the report is "Auto Parts Production Logistics," which aids in identifying and referencing the specific market segment covered.

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

To stay informed about further developments, trends, and reports in the Auto Parts Production Logistics, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.