1. What is the projected Compound Annual Growth Rate (CAGR) of the Antirust Paint?

The projected CAGR is approximately XX%.

Antirust Paint

Antirust PaintAntirust Paint by Application (Shipping Business, Oil & Gas Industry, Power Industry, Architectural, Petrochemicals or Chemicals Industry, Others), by Type (Physical Antirust Paint, Chemical Antirust Paint), by North America (United States, Canada, Mexico), by South America (Brazil, Argentina, Rest of South America), by Europe (United Kingdom, Germany, France, Italy, Spain, Russia, Benelux, Nordics, Rest of Europe), by Middle East & Africa (Turkey, Israel, GCC, North Africa, South Africa, Rest of Middle East & Africa), by Asia Pacific (China, India, Japan, South Korea, ASEAN, Oceania, Rest of Asia Pacific) Forecast 2026-2034

MR Forecast provides premium market intelligence on deep technologies that can cause a high level of disruption in the market within the next few years. When it comes to doing market viability analyses for technologies at very early phases of development, MR Forecast is second to none. What sets us apart is our set of market estimates based on secondary research data, which in turn gets validated through primary research by key companies in the target market and other stakeholders. It only covers technologies pertaining to Healthcare, IT, big data analysis, block chain technology, Artificial Intelligence (AI), Machine Learning (ML), Internet of Things (IoT), Energy & Power, Automobile, Agriculture, Electronics, Chemical & Materials, Machinery & Equipment's, Consumer Goods, and many others at MR Forecast. Market: The market section introduces the industry to readers, including an overview, business dynamics, competitive benchmarking, and firms' profiles. This enables readers to make decisions on market entry, expansion, and exit in certain nations, regions, or worldwide. Application: We give painstaking attention to the study of every product and technology, along with its use case and user categories, under our research solutions. From here on, the process delivers accurate market estimates and forecasts apart from the best and most meaningful insights.

Products generically come under this phrase and may imply any number of goods, components, materials, technology, or any combination thereof. Any business that wants to push an innovative agenda needs data on product definitions, pricing analysis, benchmarking and roadmaps on technology, demand analysis, and patents. Our research papers contain all that and much more in a depth that makes them incredibly actionable. Products broadly encompass a wide range of goods, components, materials, technologies, or any combination thereof. For businesses aiming to advance an innovative agenda, access to comprehensive data on product definitions, pricing analysis, benchmarking, technological roadmaps, demand analysis, and patents is essential. Our research papers provide in-depth insights into these areas and more, equipping organizations with actionable information that can drive strategic decision-making and enhance competitive positioning in the market.

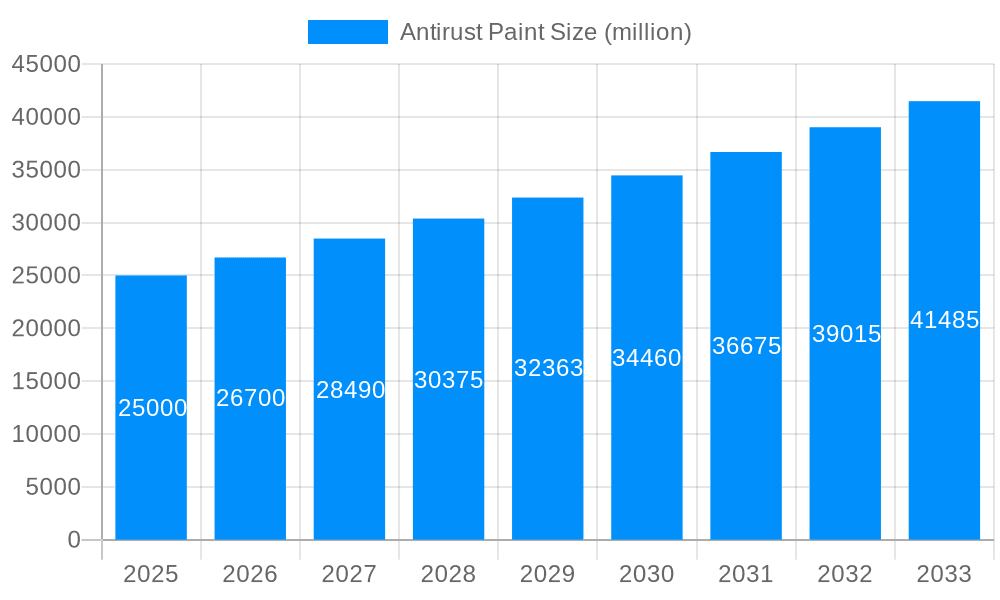

The global Antirust Paint market is poised for substantial growth, projected to reach an estimated market size of USD 25,000 million by 2025, expanding at a robust Compound Annual Growth Rate (CAGR) of 6.8% through 2033. This expansion is primarily fueled by increasing industrialization and infrastructure development across emerging economies, coupled with the growing demand for durable and protective coatings in key sectors like Shipping Business, Oil & Gas Industry, and Power Industry. The rising awareness regarding asset protection and the extended lifespan of structures due to effective corrosion prevention further bolster market demand. Advances in coating technology, leading to the development of more efficient and environmentally friendly antirust paints, are also significant growth drivers. The petrochemical and chemical industries, with their inherent corrosive environments, continue to be major consumers, demanding high-performance solutions. Architectural applications, driven by new construction and renovation projects, also represent a growing segment.

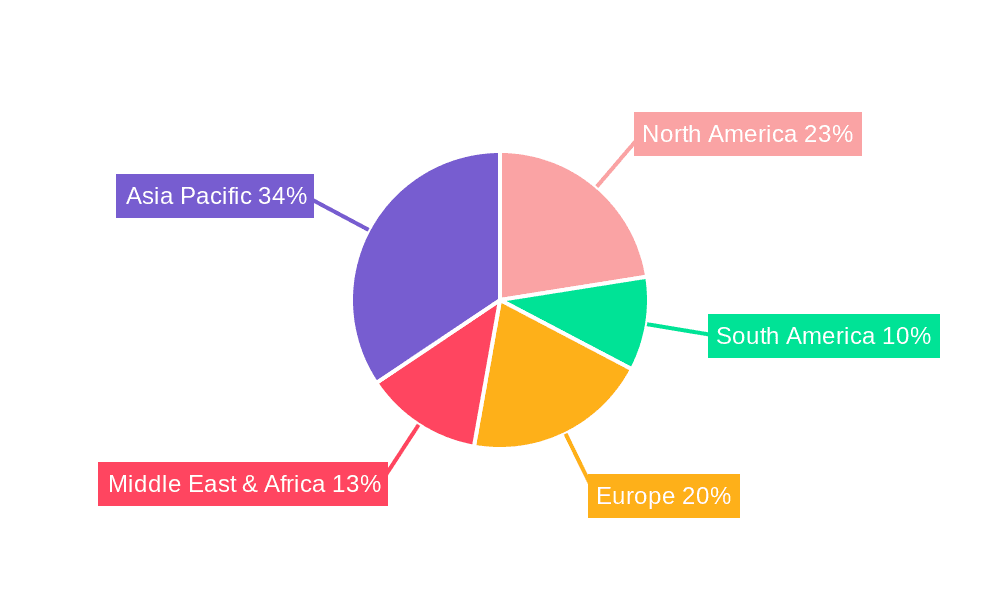

The market dynamics are shaped by the interplay of key drivers and restraints. While the drivers include escalating infrastructure investments, stringent regulations for asset longevity and safety, and technological innovations in paint formulations, the restraints are primarily associated with the volatility of raw material prices and increasing environmental concerns regarding VOC emissions from certain paint types. Chemical antirust paints are expected to witness higher demand due to their superior performance in harsh environments, while physical antirust paints offer cost-effectiveness for less demanding applications. Geographically, the Asia Pacific region is anticipated to lead the market, driven by rapid industrial expansion in China and India, followed by North America and Europe, where significant investments in infrastructure modernization and maintenance are ongoing.

This report provides an in-depth analysis of the global Antirust Paint market, offering insights into its growth trajectory, key drivers, prevailing challenges, and dominant market segments. Spanning the Study Period of 2019-2033, with the Base Year and Estimated Year at 2025, and a detailed Forecast Period from 2025-2033, the report leverages historical data from 2019-2024 to establish a robust market understanding. We project a significant market valuation in the hundreds of millions, driven by increasing industrialization and infrastructure development worldwide. The report aims to equip stakeholders with strategic intelligence to navigate the evolving landscape of anticorrosive coatings.

The global Antirust Paint market is poised for substantial growth, driven by an escalating need for asset protection across diverse industries. The market is projected to reach a valuation in the hundreds of millions by the end of the forecast period, reflecting a steady compound annual growth rate. A key trend observed is the increasing demand for high-performance, long-lasting anticorrosive solutions that can withstand harsh environmental conditions. This is particularly evident in sectors such as shipping, oil & gas, and petrochemicals, where infrastructure is constantly exposed to corrosive elements like saltwater, chemicals, and extreme temperatures. The shift towards sustainable and environmentally friendly coatings is another significant trend. Manufacturers are investing heavily in research and development to create low-VOC (Volatile Organic Compounds) and water-based antirust paints, aligning with global environmental regulations and increasing consumer preference for green products. Furthermore, technological advancements are leading to the development of smart antirust paints with self-healing properties and enhanced adhesion capabilities, offering superior protection and extending the lifespan of coated assets. The market is also witnessing a growing adoption of advanced application techniques, including electrostatic spraying and robotic application, which improve efficiency and ensure uniform coating coverage. The increasing focus on infrastructure development and maintenance in emerging economies is a significant tailwind, creating new avenues for market expansion. The demand for specialized antirust paints tailored to specific industrial needs, such as those offering exceptional chemical resistance or high-temperature performance, is also on the rise. This segmentation allows for niche market penetration and caters to the unique demands of various industrial applications. The competitive landscape is characterized by the presence of both established global players and emerging regional manufacturers, fostering innovation and price competition. The market's expansion is intrinsically linked to the health of global industrial output and construction activities, making it a bellwether for economic progress. Overall, the antirust paint market is characterized by innovation, sustainability, and a strong demand for protective coatings that ensure the longevity and integrity of critical infrastructure.

The growth of the antirust paint market is propelled by several interconnected factors, primarily stemming from the critical need to protect valuable industrial assets from the ravages of corrosion. A fundamental driver is the continuous expansion of global industrial infrastructure. Sectors like Oil & Gas Industry, Petrochemicals or Chemicals Industry, and Power Industry are consistently investing in new facilities and maintaining existing ones, all of which require robust anticorrosive coatings to prevent degradation, ensure operational safety, and minimize costly downtime. The Shipping Business also represents a significant demand driver, as vessels operate in highly corrosive marine environments, necessitating regular application of high-performance antirust paints to protect hulls and cargo holds. Furthermore, the increasing emphasis on extending the lifespan of infrastructure and equipment, driven by economic considerations and sustainability goals, fuels the demand for durable and effective antirust solutions. Governments worldwide are also investing heavily in infrastructure development and maintenance projects, particularly in transportation networks and urban development, which in turn boosts the demand for architectural and industrial coatings, including antirust paints. The rising awareness among industries about the long-term cost savings associated with proactive corrosion prevention, compared to the exorbitant expenses of repair and replacement, is another crucial catalyst.

Despite the promising growth trajectory, the Antirust Paint market faces certain challenges and restraints that can impact its expansion. One of the primary concerns is the fluctuating raw material prices. The production of antirust paints relies on various chemicals and pigments, the cost of which can be volatile due to global supply chain disruptions, geopolitical events, and changes in commodity prices. This volatility can affect manufacturing costs and ultimately impact the profitability of paint manufacturers, potentially leading to price increases for end-users. Another significant restraint is the stringent environmental regulations. Governments globally are imposing stricter rules on the composition and emission of volatile organic compounds (VOCs) in paints and coatings. While this drives innovation towards eco-friendly alternatives, it also necessitates significant investment in research and development for manufacturers to comply with these regulations, which can be a barrier, especially for smaller players. The availability of skilled labor for proper application of specialized antirust paints can also be a challenge in certain regions. Incorrect application can lead to premature coating failure, negating the benefits of high-quality products. Moreover, the initial high cost of premium antirust paints compared to conventional alternatives can deter some budget-conscious customers, particularly in price-sensitive markets, even though the long-term benefits are substantial. Finally, the economic slowdowns and recessions in various regions can lead to a reduction in industrial spending and construction activities, consequently impacting the demand for antirust paints.

The Petrochemicals or Chemicals Industry is projected to be a dominant application segment in the global Antirust Paint market, driven by the inherent corrosive nature of the materials handled in these facilities and the stringent safety requirements. These industries often involve complex processes with exposure to a wide range of aggressive chemicals, high temperatures, and pressures, necessitating advanced anticorrosive protection for pipelines, storage tanks, reactors, and structural components. The demand for specialized chemical-resistant paints, formulated to withstand specific corrosive agents, is particularly high in this sector. The continuous expansion and modernization of petrochemical and chemical plants, especially in emerging economies, further fuels the demand for high-performance antirust coatings.

Regionally, Asia Pacific is anticipated to emerge as the leading market for antirust paints. This dominance is attributed to several key factors:

In addition to the Petrochemicals or Chemicals Industry, the Shipping Business is also a critical application segment, consistently driving demand for specialized marine coatings. The harsh saline environment and constant exposure to water necessitate highly durable and effective antirust paints to protect vessel hulls, decks, and superstructures from corrosion, ensuring the longevity and safety of maritime assets. The Oil & Gas Industry, both upstream and downstream, also remains a key consumer, with extensive requirements for protecting offshore platforms, pipelines, refineries, and storage facilities from corrosive hydrocarbons, saltwater, and atmospheric elements.

Considering the Type of antirust paint, both Physical Antirust Paint and Chemical Antirust Paint are crucial. Physical antirust paints offer a barrier against corrosive agents, while chemical antirust paints actively react with the metal surface to prevent corrosion. The choice between them often depends on the specific application, environmental conditions, and desired longevity, with a growing trend towards hybrid formulations that combine the benefits of both.

The Antirust Paint industry's growth is significantly catalyzed by increasing global infrastructure development and the imperative to protect existing assets from corrosion. This includes major projects in the Oil & Gas Industry, Power Industry, and transportation networks, all of which demand durable anticorrosive coatings. Furthermore, the rising demand for sustainable and eco-friendly coatings is pushing innovation in low-VOC and water-based formulations, opening new market opportunities. The focus on extending the lifespan of industrial equipment and structures, driven by economic prudence and environmental consciousness, also acts as a powerful growth stimulant.

This report offers a holistic examination of the Antirust Paint market, encompassing its current trends, future projections, and strategic imperatives. It delves into the intricate interplay of market drivers, such as escalating industrial expansion and the relentless pursuit of asset longevity, alongside the restraining forces of raw material volatility and stringent environmental regulations. The report meticulously analyzes the market's segmentation across diverse applications like the Shipping Business and Petrochemicals or Chemicals Industry, as well as by paint type, including Physical Antirust Paint and Chemical Antirust Paint. With a comprehensive outlook from 2019 to 2033, and specific financial estimations for 2025, this report is an indispensable tool for stakeholders seeking to understand and capitalize on the dynamic evolution of the global antirust paint landscape.

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of XX% from 2020-2034 |

| Segmentation |

|

Note*: In applicable scenarios

Primary Research

Secondary Research

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence

The projected CAGR is approximately XX%.

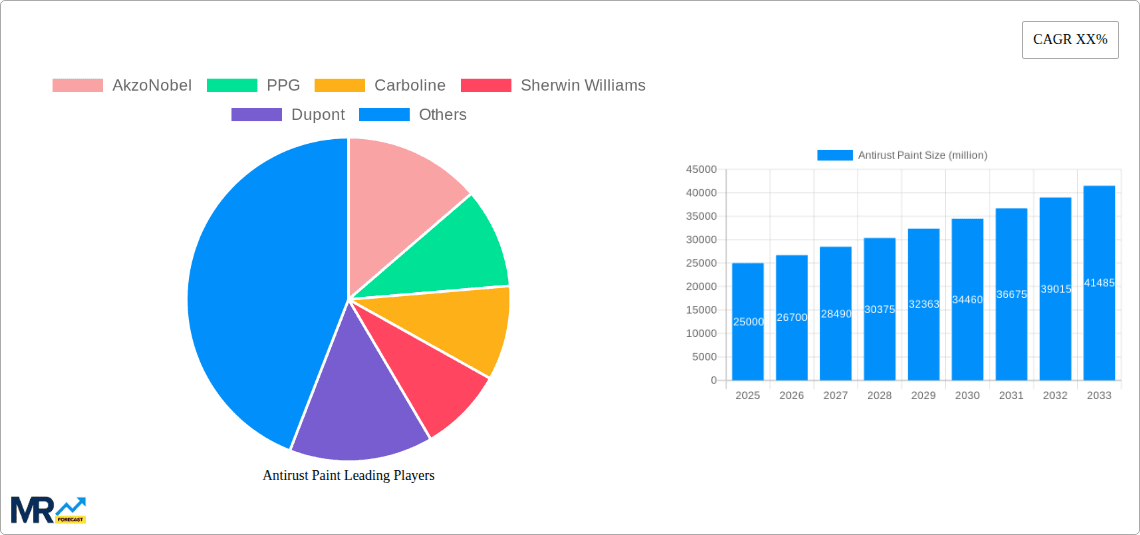

Key companies in the market include AkzoNobel, PPG, Carboline, Sherwin Williams, Dupont, BASF, Hempel, Kansai Paint, Nippon Paint, Jotun, CMP, Guangzhou Pearl River Chemical, JiangSu Lanling Group, Wuhan Shuanghu Paint, Hunan Xiangjing Paint, Hanghzhou Great Bridge, Shijiazhuang GOLDENFISH Paint, Tianjin Beacon Paint, Northwest Yongxin chemical, Chongqing Sanxia Paints, SCC, China Paint (Shenzhen), Beijing BSS, .

The market segments include Application, Type.

The market size is estimated to be USD XXX million as of 2022.

N/A

N/A

N/A

N/A

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3480.00, USD 5220.00, and USD 6960.00 respectively.

The market size is provided in terms of value, measured in million and volume, measured in K.

Yes, the market keyword associated with the report is "Antirust Paint," which aids in identifying and referencing the specific market segment covered.

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

To stay informed about further developments, trends, and reports in the Antirust Paint, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.