1. What is the projected Compound Annual Growth Rate (CAGR) of the Anodized Aluminum Cookware?

The projected CAGR is approximately 2.2%.

MR Forecast provides premium market intelligence on deep technologies that can cause a high level of disruption in the market within the next few years. When it comes to doing market viability analyses for technologies at very early phases of development, MR Forecast is second to none. What sets us apart is our set of market estimates based on secondary research data, which in turn gets validated through primary research by key companies in the target market and other stakeholders. It only covers technologies pertaining to Healthcare, IT, big data analysis, block chain technology, Artificial Intelligence (AI), Machine Learning (ML), Internet of Things (IoT), Energy & Power, Automobile, Agriculture, Electronics, Chemical & Materials, Machinery & Equipment's, Consumer Goods, and many others at MR Forecast. Market: The market section introduces the industry to readers, including an overview, business dynamics, competitive benchmarking, and firms' profiles. This enables readers to make decisions on market entry, expansion, and exit in certain nations, regions, or worldwide. Application: We give painstaking attention to the study of every product and technology, along with its use case and user categories, under our research solutions. From here on, the process delivers accurate market estimates and forecasts apart from the best and most meaningful insights.

Products generically come under this phrase and may imply any number of goods, components, materials, technology, or any combination thereof. Any business that wants to push an innovative agenda needs data on product definitions, pricing analysis, benchmarking and roadmaps on technology, demand analysis, and patents. Our research papers contain all that and much more in a depth that makes them incredibly actionable. Products broadly encompass a wide range of goods, components, materials, technologies, or any combination thereof. For businesses aiming to advance an innovative agenda, access to comprehensive data on product definitions, pricing analysis, benchmarking, technological roadmaps, demand analysis, and patents is essential. Our research papers provide in-depth insights into these areas and more, equipping organizations with actionable information that can drive strategic decision-making and enhance competitive positioning in the market.

Anodized Aluminum Cookware

Anodized Aluminum CookwareAnodized Aluminum Cookware by Type (Pot, Pan, Other), by Application (Residential, Commercial), by North America (United States, Canada, Mexico), by South America (Brazil, Argentina, Rest of South America), by Europe (United Kingdom, Germany, France, Italy, Spain, Russia, Benelux, Nordics, Rest of Europe), by Middle East & Africa (Turkey, Israel, GCC, North Africa, South Africa, Rest of Middle East & Africa), by Asia Pacific (China, India, Japan, South Korea, ASEAN, Oceania, Rest of Asia Pacific) Forecast 2025-2033

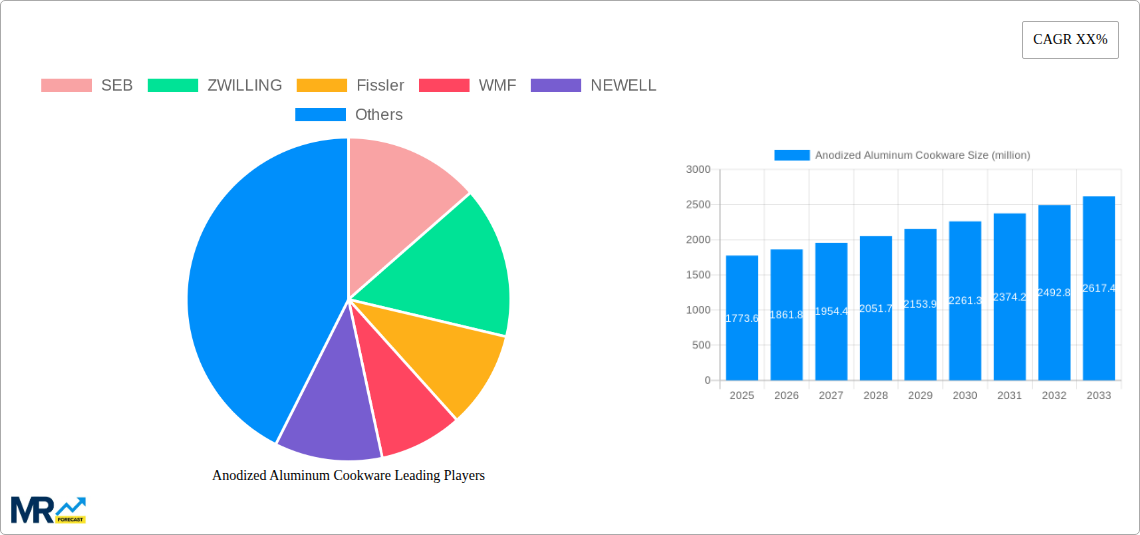

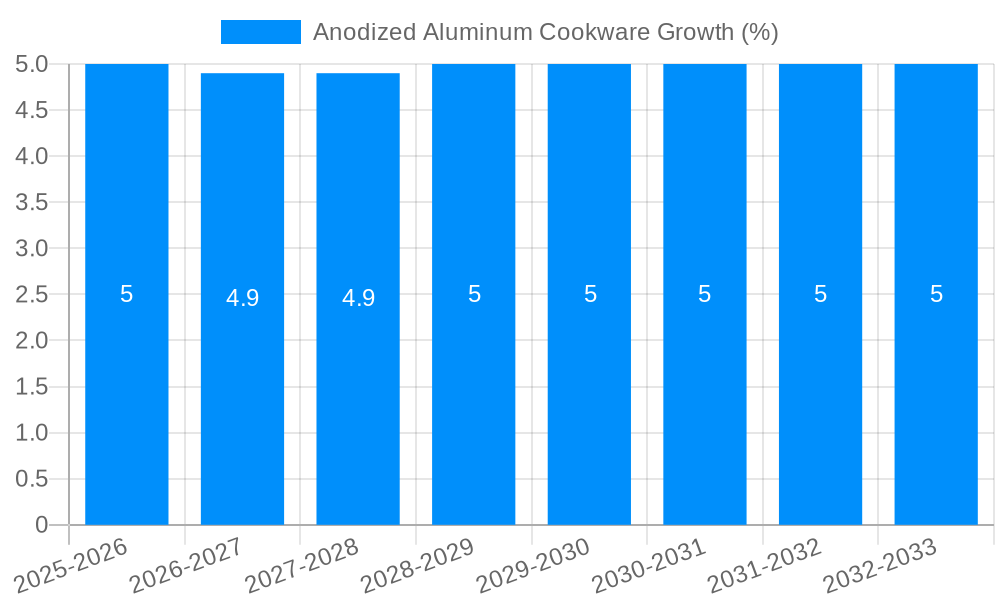

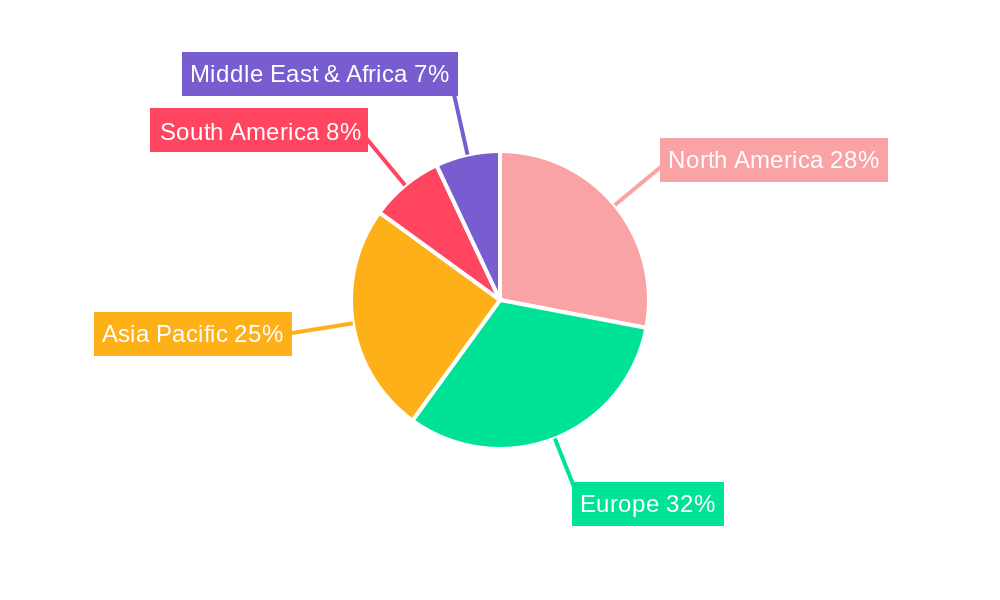

The global anodized aluminum cookware market, valued at $1522.8 million in 2025, is projected to experience steady growth, driven by increasing consumer preference for durable, lightweight, and non-stick cookware. The 2.2% CAGR indicates a consistent, albeit moderate, expansion over the forecast period (2025-2033). Key growth drivers include the rising demand for healthier cooking options, facilitated by the even heating and non-stick properties of anodized aluminum. Furthermore, the increasing popularity of home cooking, fueled by changing lifestyles and a growing awareness of food quality, further propels market growth. The market is segmented by type (pots, pans, others) and application (residential, commercial), with the residential segment dominating due to higher household penetration. Major players like SEB, Zwilling, and Fissler compete through innovation in design, material, and features, catering to diverse consumer needs and preferences. While the market enjoys steady growth, potential restraints include the emergence of alternative materials like stainless steel and ceramic cookware, and fluctuating raw material prices impacting manufacturing costs. Geographical expansion into developing economies with rising disposable incomes presents substantial opportunities for market players. The North American and European markets currently hold significant shares but the Asia-Pacific region, particularly China and India, shows significant potential for future growth due to expanding middle classes and increasing urbanization. Strategic partnerships, product diversification, and focusing on sustainable manufacturing practices will be crucial for sustained success in this competitive landscape.

The competitive landscape is characterized by a mix of established global brands and regional players. Established brands leverage their strong brand reputation and distribution networks, while regional players focus on localized preferences and cost-effective production. Innovation in design, such as the integration of ergonomic handles and stackable designs, plays a vital role in enhancing product appeal. The emphasis on durability and longevity, coupled with the introduction of eco-friendly manufacturing processes, contributes to market growth. Understanding consumer preferences related to specific features such as even heat distribution, scratch resistance, and ease of cleaning remains critical for manufacturers to maintain a competitive edge. Future trends indicate an increased demand for cookware sets, multi-functional cookware, and specialized cookware for specific cuisines, all of which present lucrative opportunities for expansion within the anodized aluminum cookware market.

The global anodized aluminum cookware market exhibited robust growth throughout the historical period (2019-2024), exceeding several million units in sales. This upward trajectory is projected to continue, with estimations indicating a market value surpassing several billion dollars by 2033. Key market insights reveal a strong consumer preference for durable, lightweight, and non-reactive cookware, attributes inherent to anodized aluminum. The rising demand for healthy cooking methods, coupled with the increasing popularity of home cooking, particularly during and post-pandemic lockdowns, significantly boosted market growth. Furthermore, the versatility of anodized aluminum cookware, suitable for various cooking techniques (from stovetop to oven), contributes to its widespread appeal. The market is witnessing a shift towards premium, multi-layered anodized aluminum cookware, offering enhanced durability and superior heat distribution. This trend is largely driven by the increasing disposable incomes in emerging economies and a growing awareness of the long-term benefits of investing in quality cookware. The market also shows potential for expansion through innovative product design, incorporating features such as ergonomic handles, stackable designs, and integrated temperature indicators. The shift towards sustainable practices, particularly in manufacturing and material sourcing, is another emerging trend that will shape the future direction of this market, attracting environmentally-conscious consumers. Overall, the anodized aluminum cookware market is poised for consistent growth, driven by a confluence of consumer preferences, technological advancements, and evolving lifestyles.

Several key factors fuel the expansion of the anodized aluminum cookware market. The inherent properties of anodized aluminum – its exceptional durability, lightweight nature, and resistance to corrosion and scratching – make it a highly desirable material for cookware. This translates to longer product lifecycles and reduced consumer replacement costs, attracting budget-conscious buyers. The non-reactive surface prevents interaction with food, ensuring food safety and preserving the flavor of dishes. The even heat distribution provided by anodized aluminum results in consistent cooking, leading to superior culinary outcomes. This attribute is particularly valued by professional chefs and cooking enthusiasts alike. Moreover, the relatively low manufacturing cost of anodized aluminum cookware compared to other high-end materials makes it an accessible option for a wide range of consumers. The increasing popularity of online retail channels expands market reach and facilitates direct-to-consumer sales, further boosting market penetration. Finally, the rising disposable incomes in developing countries and the growing adoption of modern kitchen appliances and culinary practices provide a fertile ground for the continued expansion of this market segment.

Despite its positive attributes, the anodized aluminum cookware market faces certain challenges. Competition from alternative materials such as stainless steel, cast iron, and ceramic cookware presents a significant hurdle. These materials often offer unique properties, such as superior heat retention (cast iron) or perceived aesthetic appeal (stainless steel), attracting specific consumer segments. Concerns regarding the potential leaching of aluminum into food, although largely mitigated by high-quality anodization processes, persist among some consumers, impacting market perception. Furthermore, the durability of the anodization layer itself, especially with harsh cleaning methods or prolonged use, can be a concern. Fluctuations in aluminum prices affect the cost of production and can influence retail pricing, potentially reducing market competitiveness. Finally, the increasing focus on sustainability and the environmental impact of manufacturing processes necessitates the adoption of eco-friendly production methods within the industry. Addressing these challenges will require continuous improvement in material science, manufacturing techniques, and marketing strategies to maintain and improve market share.

The residential segment accounts for the lion's share of the anodized aluminum cookware market, driven by increasing household penetration and the growing popularity of home cooking. Within the residential sector, pots and pans comprise the largest segment, due to their essential role in everyday cooking.

This growth within the residential segment is propelled by factors such as:

The commercial sector, although smaller compared to the residential segment, shows steady growth fueled by demand from restaurants, hotels, and catering services. These establishments seek cookware that offers durability, ease of cleaning, and consistent cooking performance. The "other" segment, which includes specialty cookware such as woks and specialized baking pans, also shows potential for growth, driven by diverse culinary preferences and expanding food culture.

Several key factors are set to propel the growth of the anodized aluminum cookware industry in the coming years. These include continued innovation in product design and functionality, expanding into emerging markets with rising disposable incomes, strategic partnerships and collaborations to enhance distribution networks, and a growing focus on sustainable manufacturing practices appealing to environmentally-conscious consumers.

This report provides a comprehensive analysis of the anodized aluminum cookware market, encompassing historical data, current market trends, and future projections. It offers valuable insights into key market drivers, challenges, and growth opportunities. The report also includes detailed profiles of leading players, helping stakeholders to understand the competitive landscape. This data-driven analysis empowers businesses to make informed decisions and capitalize on the expanding opportunities within this dynamic market.

| Aspects | Details |

|---|---|

| Study Period | 2019-2033 |

| Base Year | 2024 |

| Estimated Year | 2025 |

| Forecast Period | 2025-2033 |

| Historical Period | 2019-2024 |

| Growth Rate | CAGR of 2.2% from 2019-2033 |

| Segmentation |

|

Note*: In applicable scenarios

Primary Research

Secondary Research

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence

The projected CAGR is approximately 2.2%.

Key companies in the market include SEB, ZWILLING, Fissler, WMF, NEWELL, Cuisinart, Vinod, Meyer Corporation, China ASD, Linkfair, Guanhua, Anotech, Homichef, De Buyer, Gers Equipement, Giza, Saften Metal San, OMS, Le Creuset, KUHN RIKON, Nuova H.S.S.C., Scanpan, BERNDES, Maspion, Neoflam, TTK Prestige, Hawkins Cookers, Nanlong, Sanhe Kitchenware, Cooker King, .

The market segments include Type, Application.

The market size is estimated to be USD 1522.8 million as of 2022.

N/A

N/A

N/A

N/A

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3480.00, USD 5220.00, and USD 6960.00 respectively.

The market size is provided in terms of value, measured in million and volume, measured in K.

Yes, the market keyword associated with the report is "Anodized Aluminum Cookware," which aids in identifying and referencing the specific market segment covered.

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

To stay informed about further developments, trends, and reports in the Anodized Aluminum Cookware, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.