1. What is the projected Compound Annual Growth Rate (CAGR) of the Aluminum Alloy Automotive Sheet?

The projected CAGR is approximately 7.82%.

Aluminum Alloy Automotive Sheet

Aluminum Alloy Automotive SheetAluminum Alloy Automotive Sheet by Application (Passenger Car, Commercial Vehicle), by Type (Cast Aluminum, Rolled Aluminum, Extruded Aluminum), by North America (United States, Canada, Mexico), by South America (Brazil, Argentina, Rest of South America), by Europe (United Kingdom, Germany, France, Italy, Spain, Russia, Benelux, Nordics, Rest of Europe), by Middle East & Africa (Turkey, Israel, GCC, North Africa, South Africa, Rest of Middle East & Africa), by Asia Pacific (China, India, Japan, South Korea, ASEAN, Oceania, Rest of Asia Pacific) Forecast 2026-2034

MR Forecast provides premium market intelligence on deep technologies that can cause a high level of disruption in the market within the next few years. When it comes to doing market viability analyses for technologies at very early phases of development, MR Forecast is second to none. What sets us apart is our set of market estimates based on secondary research data, which in turn gets validated through primary research by key companies in the target market and other stakeholders. It only covers technologies pertaining to Healthcare, IT, big data analysis, block chain technology, Artificial Intelligence (AI), Machine Learning (ML), Internet of Things (IoT), Energy & Power, Automobile, Agriculture, Electronics, Chemical & Materials, Machinery & Equipment's, Consumer Goods, and many others at MR Forecast. Market: The market section introduces the industry to readers, including an overview, business dynamics, competitive benchmarking, and firms' profiles. This enables readers to make decisions on market entry, expansion, and exit in certain nations, regions, or worldwide. Application: We give painstaking attention to the study of every product and technology, along with its use case and user categories, under our research solutions. From here on, the process delivers accurate market estimates and forecasts apart from the best and most meaningful insights.

Products generically come under this phrase and may imply any number of goods, components, materials, technology, or any combination thereof. Any business that wants to push an innovative agenda needs data on product definitions, pricing analysis, benchmarking and roadmaps on technology, demand analysis, and patents. Our research papers contain all that and much more in a depth that makes them incredibly actionable. Products broadly encompass a wide range of goods, components, materials, technologies, or any combination thereof. For businesses aiming to advance an innovative agenda, access to comprehensive data on product definitions, pricing analysis, benchmarking, technological roadmaps, demand analysis, and patents is essential. Our research papers provide in-depth insights into these areas and more, equipping organizations with actionable information that can drive strategic decision-making and enhance competitive positioning in the market.

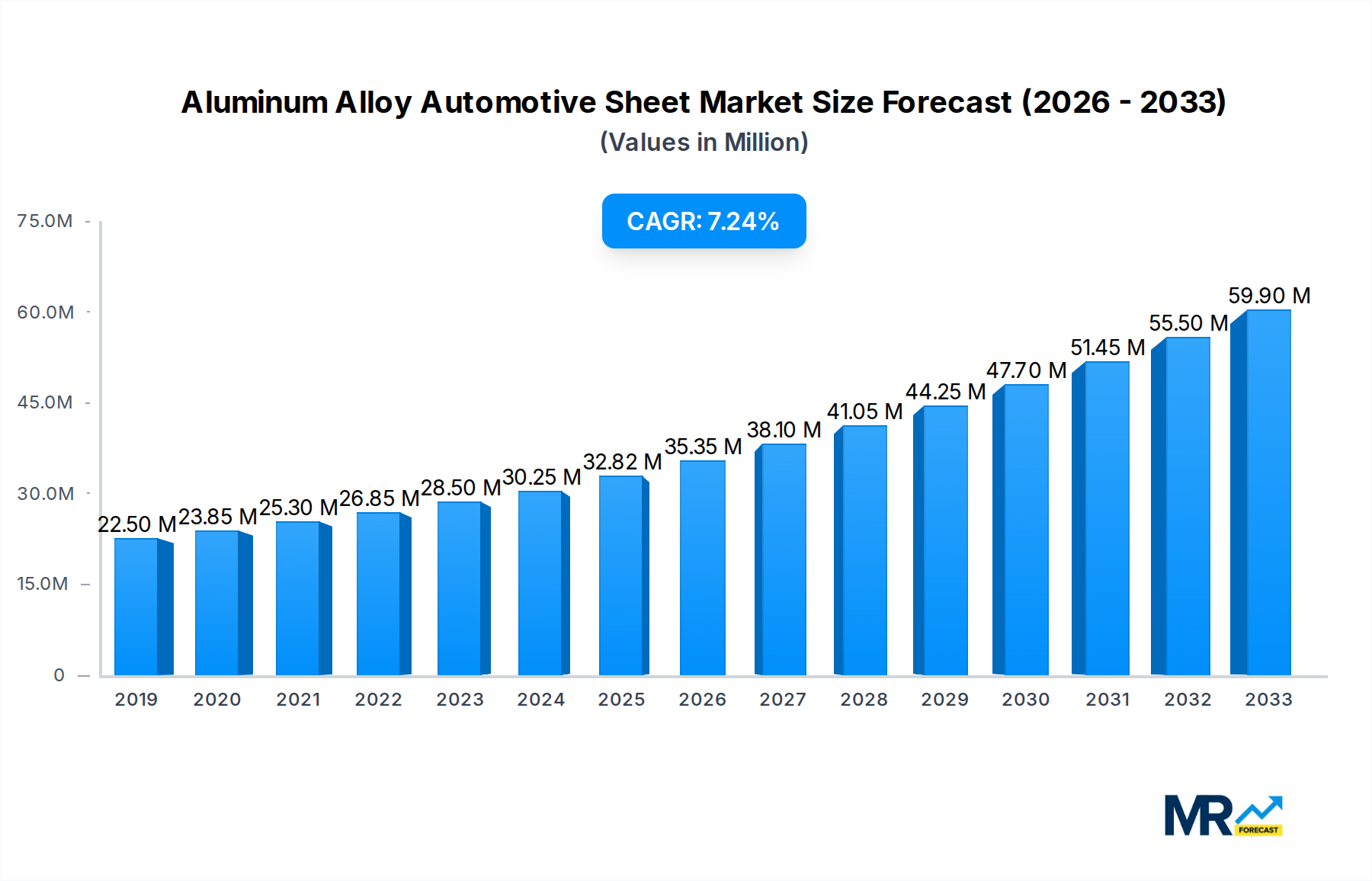

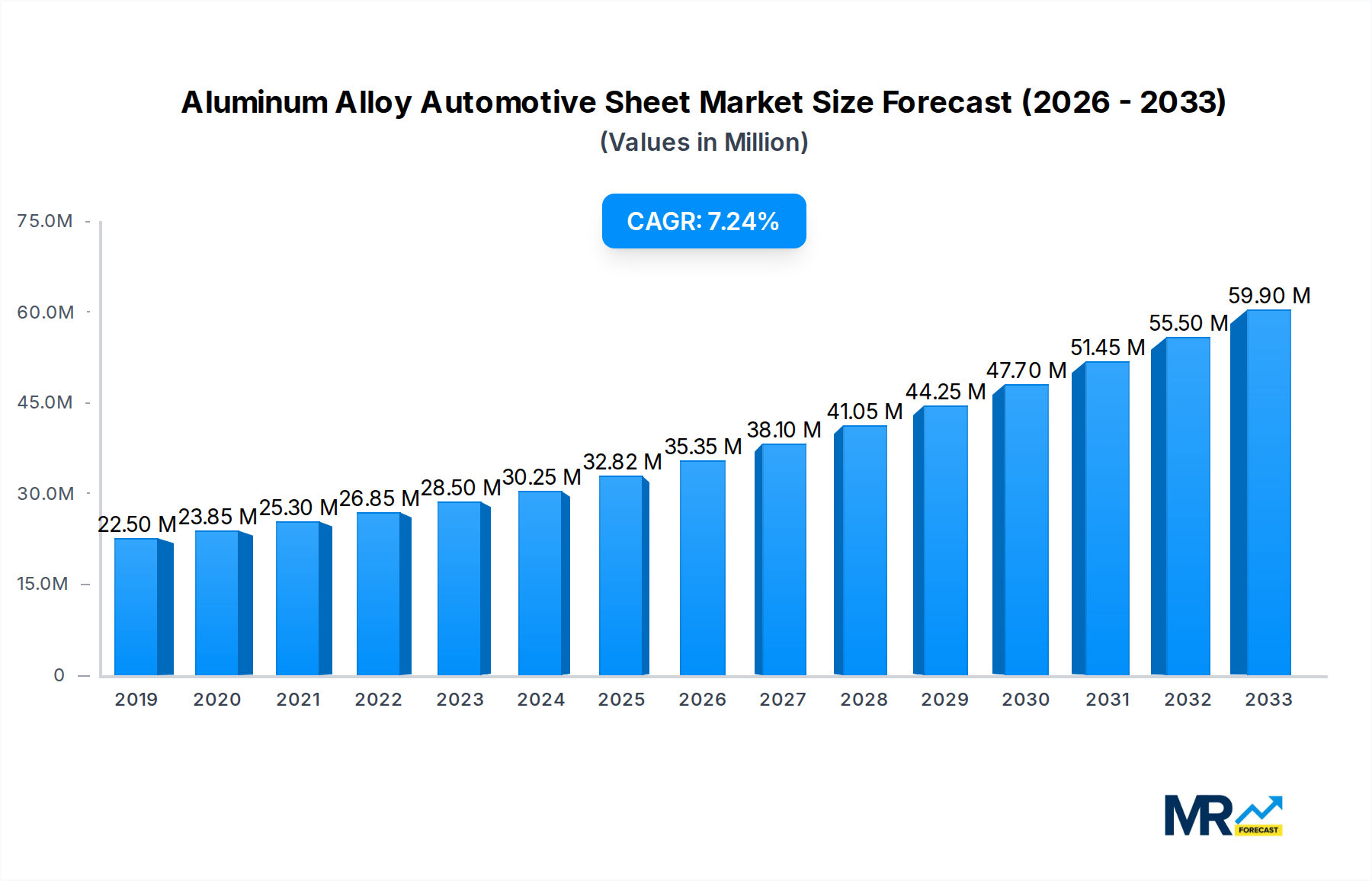

The global Aluminum Alloy Automotive Sheet market is poised for robust expansion, projected to reach approximately $32.82 billion in value by 2025 and continue its upward trajectory with a Compound Annual Growth Rate (CAGR) of 7.82% through 2033. This substantial growth is primarily fueled by the automotive industry's relentless pursuit of lighter, more fuel-efficient, and environmentally friendly vehicles. Aluminum alloy sheets are instrumental in achieving these goals, offering a compelling alternative to traditional steel components. The increasing regulatory pressures for reduced emissions and enhanced fuel economy, coupled with growing consumer demand for sustainable mobility solutions, are significant drivers. Furthermore, advancements in manufacturing technologies and the development of higher-strength aluminum alloys are broadening their applicability across various vehicle segments, including passenger cars and commercial vehicles, thereby expanding market opportunities.

The market is segmented by application into Passenger Cars and Commercial Vehicles, with Passenger Cars currently dominating due to the higher production volumes and the widespread adoption of lightweighting strategies in this segment. By type, the market encompasses Cast Aluminum, Rolled Aluminum, and Extruded Aluminum, with Rolled and Extruded Aluminum sheets being particularly critical for automotive body panels, structural components, and chassis elements. Key players such as ALCOA, Constellium, Norsk Hydro, and Novelis are at the forefront of innovation, investing heavily in research and development to produce advanced aluminum alloys that meet the stringent performance and safety requirements of the automotive sector. Emerging trends include the increasing use of advanced high-strength aluminum alloys (AHSS) and the integration of aluminum into electric vehicle (EV) platforms to offset battery weight and improve range. While the market exhibits strong growth potential, factors such as the fluctuating prices of raw materials and the established infrastructure for steel production present some restraints, though these are increasingly being outweighed by the compelling benefits of aluminum.

Here is a unique report description for Aluminum Alloy Automotive Sheet, incorporating your specified requirements:

The global aluminum alloy automotive sheet market is poised for remarkable expansion, projected to reach an estimated $35.2 billion in 2025, and further surging to $52.8 billion by the end of the forecast period in 2033, exhibiting a robust compound annual growth rate (CAGR) of 5.2% during the 2025-2033 forecast period. This upward trajectory is fundamentally driven by the automotive industry's unwavering commitment to lightweighting, a critical strategy for enhancing fuel efficiency and reducing emissions. The historical period, from 2019 to 2024, laid a strong foundation for this growth, with consistent adoption of aluminum alloys across various vehicle platforms. The base year of 2025 represents a pivotal point where advancements in alloy formulations and manufacturing techniques are becoming increasingly sophisticated, enabling greater application possibilities. We foresee a significant shift towards advanced high-strength aluminum alloys (AHSS) that offer superior mechanical properties without compromising on formability, a key concern for automotive manufacturers. The passenger car segment, in particular, will continue to be the dominant application, accounting for a substantial portion of the market share. However, the commercial vehicle sector is expected to witness accelerated growth as regulations on emissions and fuel economy become more stringent, pushing truck and bus manufacturers to explore lightweighting solutions. The evolution of rolling technologies, including advanced hot and cold rolling processes, is crucial in producing sheets with precise thickness and mechanical properties, meeting the exacting demands of automotive structural components. Furthermore, the integration of intelligent manufacturing systems and the increasing adoption of digital twin technologies in production lines will optimize efficiency and reduce waste, contributing to the overall market expansion. The emphasis on sustainability and recyclability of aluminum alloys will also play a pivotal role, aligning with global environmental goals and consumer preferences for eco-friendly vehicles. This growing environmental consciousness is not just a trend but a fundamental driver shaping the future of automotive material choices. The study period, spanning from 2019 to 2033, encapsulates this dynamic transformation, highlighting the long-term potential of aluminum alloy automotive sheets to revolutionize vehicle design and performance.

The sustained and escalating demand for aluminum alloy automotive sheets is primarily fueled by a confluence of powerful drivers that are fundamentally reshaping the automotive landscape. At the forefront is the global imperative to reduce vehicular emissions and enhance fuel economy. Governments worldwide are implementing increasingly stringent environmental regulations, compelling automakers to aggressively pursue lightweighting strategies. Aluminum alloys, with their exceptional strength-to-weight ratio, are the material of choice for achieving significant weight reductions compared to traditional steel. This weight optimization directly translates into improved fuel efficiency for internal combustion engine vehicles and extended range for electric vehicles. The burgeoning electric vehicle (EV) market is a particularly potent growth catalyst. The need to offset the weight of heavy battery packs necessitates lightweight body structures, chassis components, and other assemblies, making aluminum alloys indispensable. Furthermore, advancements in alloy development have unlocked new possibilities, offering a broader spectrum of mechanical properties, improved corrosion resistance, and enhanced formability, thereby expanding their applicability in increasingly complex vehicle designs. The growing consumer preference for more fuel-efficient and environmentally conscious vehicles also exerts a considerable influence, pushing manufacturers to adopt lighter and more sustainable materials. This synergistic interplay of regulatory pressures, technological innovation, and consumer demand creates a compelling environment for the continued dominance of aluminum alloy automotive sheets.

Despite the overwhelmingly positive outlook, the aluminum alloy automotive sheet market is not without its impediments. A significant challenge lies in the higher initial cost of aluminum alloys compared to conventional steel. While life-cycle cost benefits often outweigh this initial premium, it can still pose a barrier, particularly for budget-conscious vehicle segments or manufacturers operating on tighter margins. The complex manufacturing processes associated with forming and joining aluminum alloys also present a hurdle. Specialized tooling, advanced welding techniques (such as friction stir welding), and robust joining methods are often required, necessitating significant investment in new equipment and training for production facilities. Recycling infrastructure and efficiency remain a concern, although considerable progress is being made. Ensuring a consistent supply of high-quality recycled aluminum that meets stringent automotive specifications requires further optimization of collection, sorting, and reprocessing technologies. Repair and maintenance expertise for aluminum-intensive vehicles can also be a limiting factor. While many repair shops are adapting, a widespread lack of specialized knowledge and equipment can lead to higher repair costs and longer turnaround times, potentially impacting consumer acceptance. Finally, the availability and volatility of raw material prices, particularly for primary aluminum, can introduce an element of unpredictability into market dynamics and affect long-term pricing strategies for alloy manufacturers. Addressing these challenges proactively will be crucial for unlocking the full potential of this dynamic market.

Dominant Segments: Passenger Car and Rolled Aluminum

The Passenger Car segment is projected to continue its reign as the dominant application for aluminum alloy automotive sheets. This is underpinned by several key factors that resonate deeply with the evolution of personal transportation:

Complementing the application dominance, the Rolled Aluminum type is expected to lead the market in terms of volume and value:

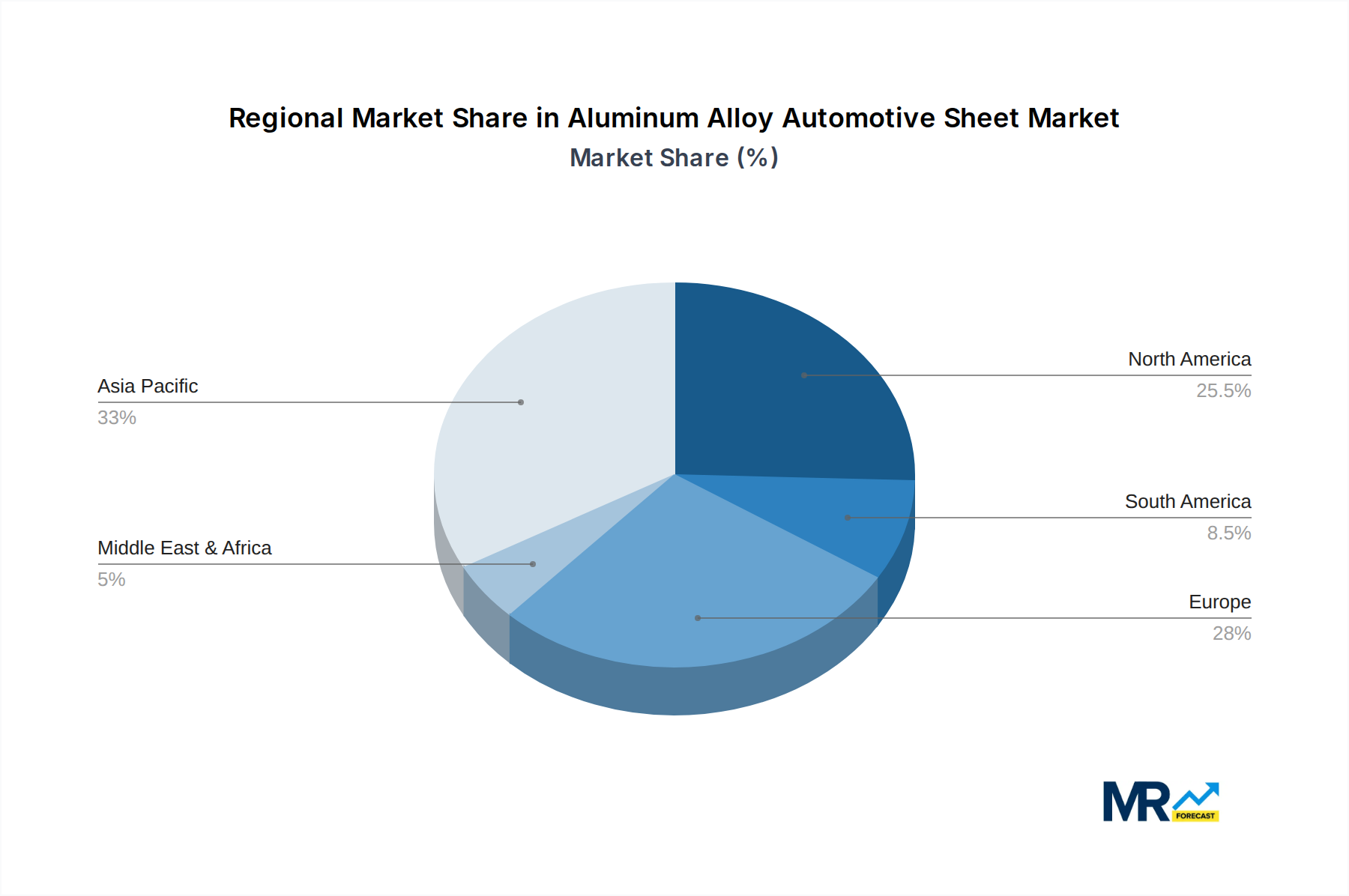

Dominant Region: Asia-Pacific

The Asia-Pacific region is poised to dominate the aluminum alloy automotive sheet market, driven by its unparalleled position as the world's largest automotive manufacturing hub and its accelerating adoption of advanced automotive technologies.

The aluminum alloy automotive sheet industry is experiencing significant growth catalysts. The accelerating global shift towards electric vehicles, driven by environmental regulations and consumer demand, is a paramount catalyst. EVs necessitate lightweighting to offset battery weight and extend range, making aluminum indispensable. Furthermore, ongoing advancements in aluminum alloy formulations, leading to enhanced strength-to-weight ratios and improved formability, are expanding their applicability in complex vehicle designs. Supportive government policies promoting sustainable transportation and manufacturing also play a crucial role.

This comprehensive report delves into the intricate dynamics of the global aluminum alloy automotive sheet market, offering an in-depth analysis from 2019 to 2033. It meticulously examines market size, segmentation by application (Passenger Car, Commercial Vehicle) and type (Cast Aluminum, Rolled Aluminum, Extruded Aluminum), and provides a detailed forecast from 2025 to 2033. The report highlights key industry developments, identifying the driving forces such as the push for lightweighting and EV adoption, alongside significant challenges like cost and manufacturing complexity. It further pinpoints the dominant regions and segments poised for substantial growth, offering strategic insights for stakeholders. The report also profiles leading players and their contributions to the evolving market landscape, providing a holistic view of this critical sector within the automotive value chain.

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 7.82% from 2020-2034 |

| Segmentation |

|

Note*: In applicable scenarios

Primary Research

Secondary Research

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence

The projected CAGR is approximately 7.82%.

Key companies in the market include ALCOA, Constellium, Norsk Hydro, Aleris, Novelis, Kobe Steel, UACJ, Weifangnyuan Aluminium Industry, Northeast Light Alloy, Southwest Aluminum (Group), Jiangsu CAIFA Aluminum, Jiangsu Alcha Aluminum, .

The market segments include Application, Type.

The market size is estimated to be USD XXX N/A as of 2022.

N/A

N/A

N/A

N/A

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3480.00, USD 5220.00, and USD 6960.00 respectively.

The market size is provided in terms of value, measured in N/A and volume, measured in K.

Yes, the market keyword associated with the report is "Aluminum Alloy Automotive Sheet," which aids in identifying and referencing the specific market segment covered.

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

To stay informed about further developments, trends, and reports in the Aluminum Alloy Automotive Sheet, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.