1. What is the projected Compound Annual Growth Rate (CAGR) of the Aerospace Grade 3D Printing Additive Manufacturing?

The projected CAGR is approximately XX%.

Aerospace Grade 3D Printing Additive Manufacturing

Aerospace Grade 3D Printing Additive ManufacturingAerospace Grade 3D Printing Additive Manufacturing by Type (Plastics Material, Ceramics Material, Metals Material, Others, World Aerospace Grade 3D Printing Additive Manufacturing Production ), by Application (Airplane, Aerospace, Others, World Aerospace Grade 3D Printing Additive Manufacturing Production ), by North America (United States, Canada, Mexico), by South America (Brazil, Argentina, Rest of South America), by Europe (United Kingdom, Germany, France, Italy, Spain, Russia, Benelux, Nordics, Rest of Europe), by Middle East & Africa (Turkey, Israel, GCC, North Africa, South Africa, Rest of Middle East & Africa), by Asia Pacific (China, India, Japan, South Korea, ASEAN, Oceania, Rest of Asia Pacific) Forecast 2026-2034

MR Forecast provides premium market intelligence on deep technologies that can cause a high level of disruption in the market within the next few years. When it comes to doing market viability analyses for technologies at very early phases of development, MR Forecast is second to none. What sets us apart is our set of market estimates based on secondary research data, which in turn gets validated through primary research by key companies in the target market and other stakeholders. It only covers technologies pertaining to Healthcare, IT, big data analysis, block chain technology, Artificial Intelligence (AI), Machine Learning (ML), Internet of Things (IoT), Energy & Power, Automobile, Agriculture, Electronics, Chemical & Materials, Machinery & Equipment's, Consumer Goods, and many others at MR Forecast. Market: The market section introduces the industry to readers, including an overview, business dynamics, competitive benchmarking, and firms' profiles. This enables readers to make decisions on market entry, expansion, and exit in certain nations, regions, or worldwide. Application: We give painstaking attention to the study of every product and technology, along with its use case and user categories, under our research solutions. From here on, the process delivers accurate market estimates and forecasts apart from the best and most meaningful insights.

Products generically come under this phrase and may imply any number of goods, components, materials, technology, or any combination thereof. Any business that wants to push an innovative agenda needs data on product definitions, pricing analysis, benchmarking and roadmaps on technology, demand analysis, and patents. Our research papers contain all that and much more in a depth that makes them incredibly actionable. Products broadly encompass a wide range of goods, components, materials, technologies, or any combination thereof. For businesses aiming to advance an innovative agenda, access to comprehensive data on product definitions, pricing analysis, benchmarking, technological roadmaps, demand analysis, and patents is essential. Our research papers provide in-depth insights into these areas and more, equipping organizations with actionable information that can drive strategic decision-making and enhance competitive positioning in the market.

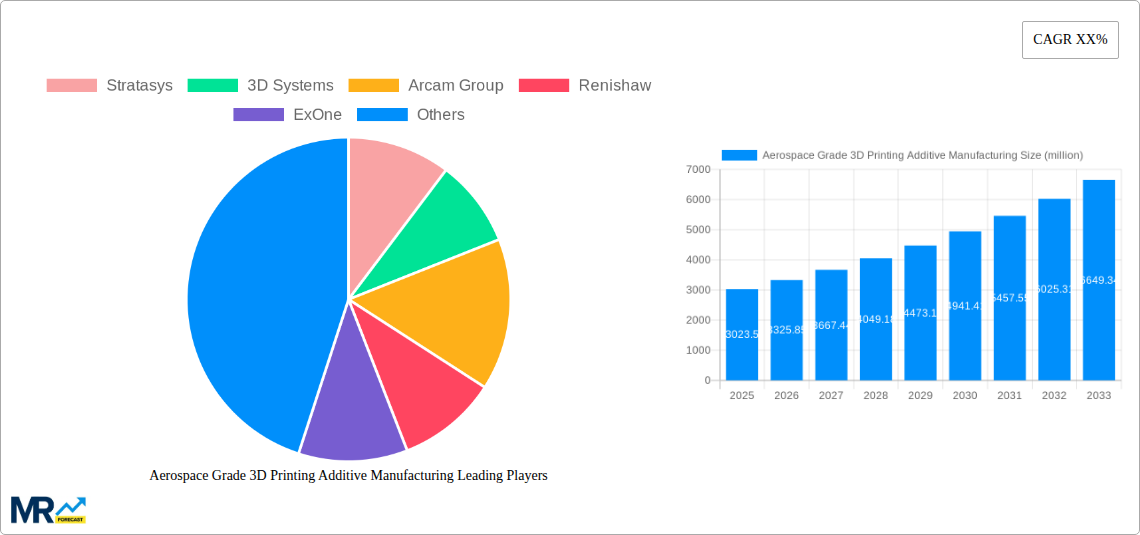

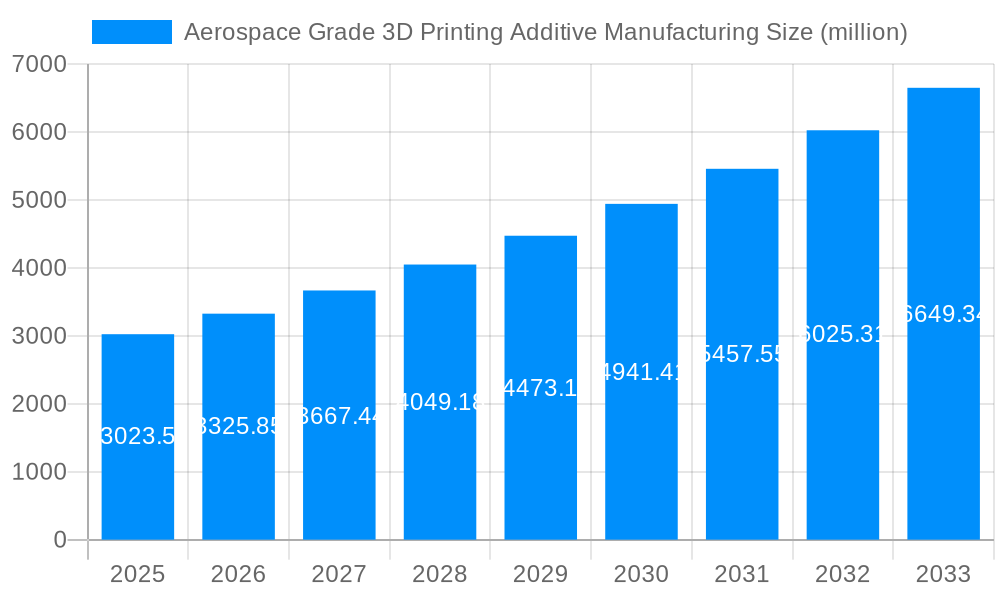

The Aerospace Grade 3D Printing Additive Manufacturing market is experiencing robust growth, driven by the increasing demand for lightweight, high-strength components in aircraft and spacecraft. The market, valued at $3023.5 million in 2025, is projected to witness significant expansion over the forecast period (2025-2033). Key drivers include the rising adoption of additive manufacturing for prototyping and production, the need for improved fuel efficiency in aerospace vehicles, and the desire for customized component designs. Furthermore, advancements in materials science, specifically in high-performance polymers and metal alloys suitable for aerospace applications, are fueling market expansion. While high initial investment costs and potential scalability challenges might act as restraints, the long-term benefits of reduced production time, material waste, and improved component performance are overcoming these hurdles. Leading players like Stratasys, 3D Systems, and others are actively investing in R&D to enhance material properties, process efficiency, and expand their product portfolios to cater to the growing demand. The market segmentation is likely diverse, encompassing various printing technologies (e.g., Selective Laser Melting, Stereolithography), materials (e.g., titanium alloys, aluminum alloys, polymers), and application areas (e.g., engine components, airframes, spacecraft parts). Regional growth will likely be distributed across North America, Europe, and Asia, mirroring the existing aerospace manufacturing hubs. The sustained focus on innovation and collaboration across the aerospace and additive manufacturing industries promises continued expansion throughout the forecast period.

The substantial growth potential is further amplified by the industry's shift towards digitalization and the increasing use of data analytics for process optimization. This facilitates improved design iterations, reduced production errors, and enhanced quality control. Moreover, government initiatives supporting the adoption of advanced manufacturing technologies, coupled with the rising demand for unmanned aerial vehicles (UAVs) and space exploration missions, contributes to the expanding market. However, regulatory hurdles regarding material certification and quality assurance processes remain a factor to be addressed. Despite these challenges, the overall outlook for Aerospace Grade 3D Printing Additive Manufacturing remains positive, with continued market expansion projected throughout the forecast period, driven by the compelling advantages of this technology in the aerospace sector.

The aerospace grade 3D printing additive manufacturing market is experiencing explosive growth, projected to reach several billion dollars by 2033. This surge is driven by the industry's increasing demand for lightweight, high-strength components, complex geometries, and reduced production lead times. The historical period (2019-2024) witnessed significant adoption of additive manufacturing (AM) techniques, particularly in prototyping and the creation of low-volume, high-value parts. The estimated year (2025) showcases a market already exceeding hundreds of millions of dollars, poised for significant expansion in the forecast period (2025-2033). Key market insights reveal a shift from primarily using AM for prototyping towards serial production of flight-critical components. This trend is further fueled by advancements in materials science, resulting in improved mechanical properties and certification compliance for AM-produced parts. The market is witnessing a convergence of technologies, with hybrid manufacturing processes combining AM with traditional subtractive methods becoming increasingly prevalent. This integration enhances efficiency and allows for the production of complex parts with superior accuracy. Furthermore, the development of robust quality control measures and standardization efforts is bolstering industry confidence in the reliability of AM-produced aerospace components. This combination of technological advancements, regulatory support, and increased acceptance by aerospace manufacturers is driving the substantial growth predicted for the coming decade. The market is segmented by various printing technologies (e.g., laser powder bed fusion, directed energy deposition), materials (e.g., titanium alloys, aluminum alloys, polymers), and applications (e.g., aircraft engines, airframes, satellites). Competition is fierce among established players and emerging startups, fostering innovation and pushing the boundaries of what's possible with AM in the aerospace sector.

Several key factors are driving the rapid expansion of aerospace-grade 3D printing. Firstly, the inherent ability of additive manufacturing to create complex geometries unattainable through traditional methods significantly reduces part count and simplifies assembly processes, leading to substantial cost savings and improved efficiency. Secondly, the production of lightweight components using AM is crucial for enhancing fuel efficiency and reducing emissions, aligning perfectly with the industry's growing sustainability focus. This translates to millions of dollars in savings across the entire aerospace manufacturing lifecycle. Thirdly, the increased demand for customized and personalized products within the aerospace sector is readily met by the flexibility of AM. Small-batch production and rapid prototyping capabilities allow for quicker turnaround times and efficient adaptation to specific design requirements, particularly important for niche applications and specialized aircraft. Finally, ongoing advancements in materials science, specifically in developing high-performance aerospace-grade alloys suitable for AM, are expanding the range of applications and boosting the reliability of additively manufactured components. These improvements further reduce the risks associated with adopting this technology, incentivizing wider adoption within the industry. The continuous development of software and hardware, alongside improved automation, are also contributing to the overall growth of this market segment.

Despite the significant potential, several challenges hinder widespread adoption of aerospace-grade 3D printing. The high initial investment costs associated with acquiring advanced AM systems and the need for specialized expertise to operate and maintain them present a significant barrier to entry, particularly for smaller companies. Strict regulatory requirements and certification processes for AM-produced flight-critical components demand extensive testing and validation, adding to the time and cost involved in bringing new products to market. Concerns regarding part consistency, repeatability, and the potential for defects within AM-produced parts remain, although significant progress is being made in addressing these issues through advanced process control and quality assurance methodologies. The limited range of materials currently suitable for aerospace applications and the relatively slow build speeds compared to traditional manufacturing methods also pose challenges. Furthermore, the lack of standardization across different AM technologies and materials makes it difficult to compare and benchmark the performance of different systems and processes, leading to uncertainty among potential adopters. Overcoming these challenges requires continued research and development, standardization efforts, and collaboration among industry stakeholders to build trust and confidence in the reliability and safety of AM-produced aerospace components.

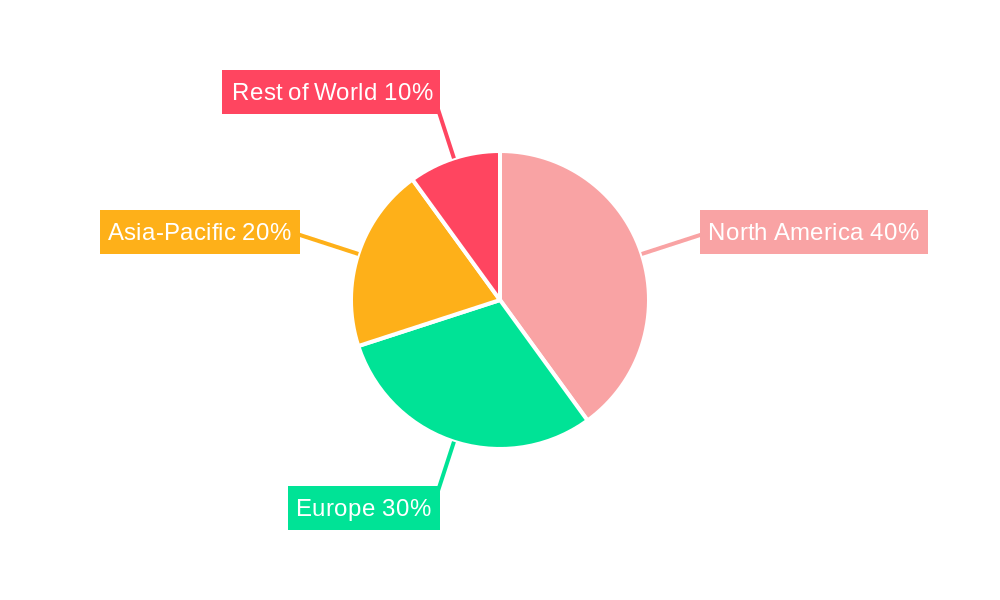

The aerospace grade 3D printing additive manufacturing market is geographically diverse, with several key regions exhibiting strong growth.

North America: The US, in particular, holds a leading position due to a strong aerospace industry, significant investments in R&D, and a well-established ecosystem of AM technology providers and service bureaus. This region accounts for a substantial portion of the overall market value, projected to be in the hundreds of millions of dollars in 2025 and growing significantly thereafter. Extensive government support and a focus on domestic manufacturing bolster this region's prominence.

Europe: Significant advancements in AM technology and a robust aerospace manufacturing sector position Europe as a crucial market. Countries like Germany, France, and the UK are key players, contributing millions of dollars annually to the market. European collaborations and investments in research initiatives further solidify the region’s strong market position.

Asia-Pacific: Rapid industrialization and growth in the aerospace sector across countries like China, Japan, and South Korea are driving the demand for AM technologies. The region's growth is expected to accelerate, reaching a substantial portion of the global market by 2033. While currently smaller than North America and Europe, its growth trajectory is remarkably steep.

Segments: The segment focused on aircraft engine components is projected to dominate due to the significant advantages of AM in creating intricate internal cooling channels and lightweight turbine blades, leading to fuel efficiency gains worth millions of dollars annually in fuel savings for airlines. The titanium alloy materials segment also enjoys a significant share, as titanium's high strength-to-weight ratio makes it ideal for aerospace applications. Lastly, the laser powder bed fusion (LPBF) technology segment holds a considerable market share due to its precision and ability to produce complex, high-quality parts. These segments are expected to maintain their dominance throughout the forecast period, driving substantial growth in the overall market.

Several factors will propel the growth of the aerospace grade 3D printing industry further. These include the continued development of high-performance materials suitable for AM, advancements in printing technologies to improve speed and accuracy, increasing government funding for research and development in this area, and the rising adoption of Industry 4.0 technologies facilitating better integration and automation within the manufacturing process. Furthermore, growing collaboration between aerospace companies and AM technology providers will accelerate innovation and enable the wider adoption of AM in aerospace manufacturing. This synergistic approach fosters trust and helps to address concerns about reliability and certification.

This report provides a comprehensive overview of the aerospace grade 3D printing additive manufacturing market, including detailed analysis of market trends, driving forces, challenges, key players, and future growth prospects. The report covers various segments of the market, offering detailed insights into each segment’s growth potential and market share. It provides valuable information for stakeholders across the value chain, including manufacturers, suppliers, researchers, investors, and government agencies involved in aerospace manufacturing. The data presented in this report offers a crucial foundation for informed decision-making in this rapidly expanding market, expected to reach billions within the next decade.

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of XX% from 2020-2034 |

| Segmentation |

|

Note*: In applicable scenarios

Primary Research

Secondary Research

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence

The projected CAGR is approximately XX%.

Key companies in the market include Stratasys, 3D Systems, Arcam Group, Renishaw, ExOne, Optomec, SLM Solutions, EnvisionTEC, VoxelJet AG, Sciaky Inc, GE, Formlabs, eos gmbh, Orion AM, AON3D, .

The market segments include Type, Application.

The market size is estimated to be USD 3023.5 million as of 2022.

N/A

N/A

N/A

N/A

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4480.00, USD 6720.00, and USD 8960.00 respectively.

The market size is provided in terms of value, measured in million and volume, measured in K.

Yes, the market keyword associated with the report is "Aerospace Grade 3D Printing Additive Manufacturing," which aids in identifying and referencing the specific market segment covered.

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

To stay informed about further developments, trends, and reports in the Aerospace Grade 3D Printing Additive Manufacturing, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.