1. What is the projected Compound Annual Growth Rate (CAGR) of the Advanced Aerospace Composite Materials?

The projected CAGR is approximately 12%.

Advanced Aerospace Composite Materials

Advanced Aerospace Composite MaterialsAdvanced Aerospace Composite Materials by Type (Metal Matrix Composites, Ceramic Matrix Composites, Polymer Matrix Composites), by Application (Aircraft, Space, Others), by North America (United States, Canada, Mexico), by South America (Brazil, Argentina, Rest of South America), by Europe (United Kingdom, Germany, France, Italy, Spain, Russia, Benelux, Nordics, Rest of Europe), by Middle East & Africa (Turkey, Israel, GCC, North Africa, South Africa, Rest of Middle East & Africa), by Asia Pacific (China, India, Japan, South Korea, ASEAN, Oceania, Rest of Asia Pacific) Forecast 2026-2034

MR Forecast provides premium market intelligence on deep technologies that can cause a high level of disruption in the market within the next few years. When it comes to doing market viability analyses for technologies at very early phases of development, MR Forecast is second to none. What sets us apart is our set of market estimates based on secondary research data, which in turn gets validated through primary research by key companies in the target market and other stakeholders. It only covers technologies pertaining to Healthcare, IT, big data analysis, block chain technology, Artificial Intelligence (AI), Machine Learning (ML), Internet of Things (IoT), Energy & Power, Automobile, Agriculture, Electronics, Chemical & Materials, Machinery & Equipment's, Consumer Goods, and many others at MR Forecast. Market: The market section introduces the industry to readers, including an overview, business dynamics, competitive benchmarking, and firms' profiles. This enables readers to make decisions on market entry, expansion, and exit in certain nations, regions, or worldwide. Application: We give painstaking attention to the study of every product and technology, along with its use case and user categories, under our research solutions. From here on, the process delivers accurate market estimates and forecasts apart from the best and most meaningful insights.

Products generically come under this phrase and may imply any number of goods, components, materials, technology, or any combination thereof. Any business that wants to push an innovative agenda needs data on product definitions, pricing analysis, benchmarking and roadmaps on technology, demand analysis, and patents. Our research papers contain all that and much more in a depth that makes them incredibly actionable. Products broadly encompass a wide range of goods, components, materials, technologies, or any combination thereof. For businesses aiming to advance an innovative agenda, access to comprehensive data on product definitions, pricing analysis, benchmarking, technological roadmaps, demand analysis, and patents is essential. Our research papers provide in-depth insights into these areas and more, equipping organizations with actionable information that can drive strategic decision-making and enhance competitive positioning in the market.

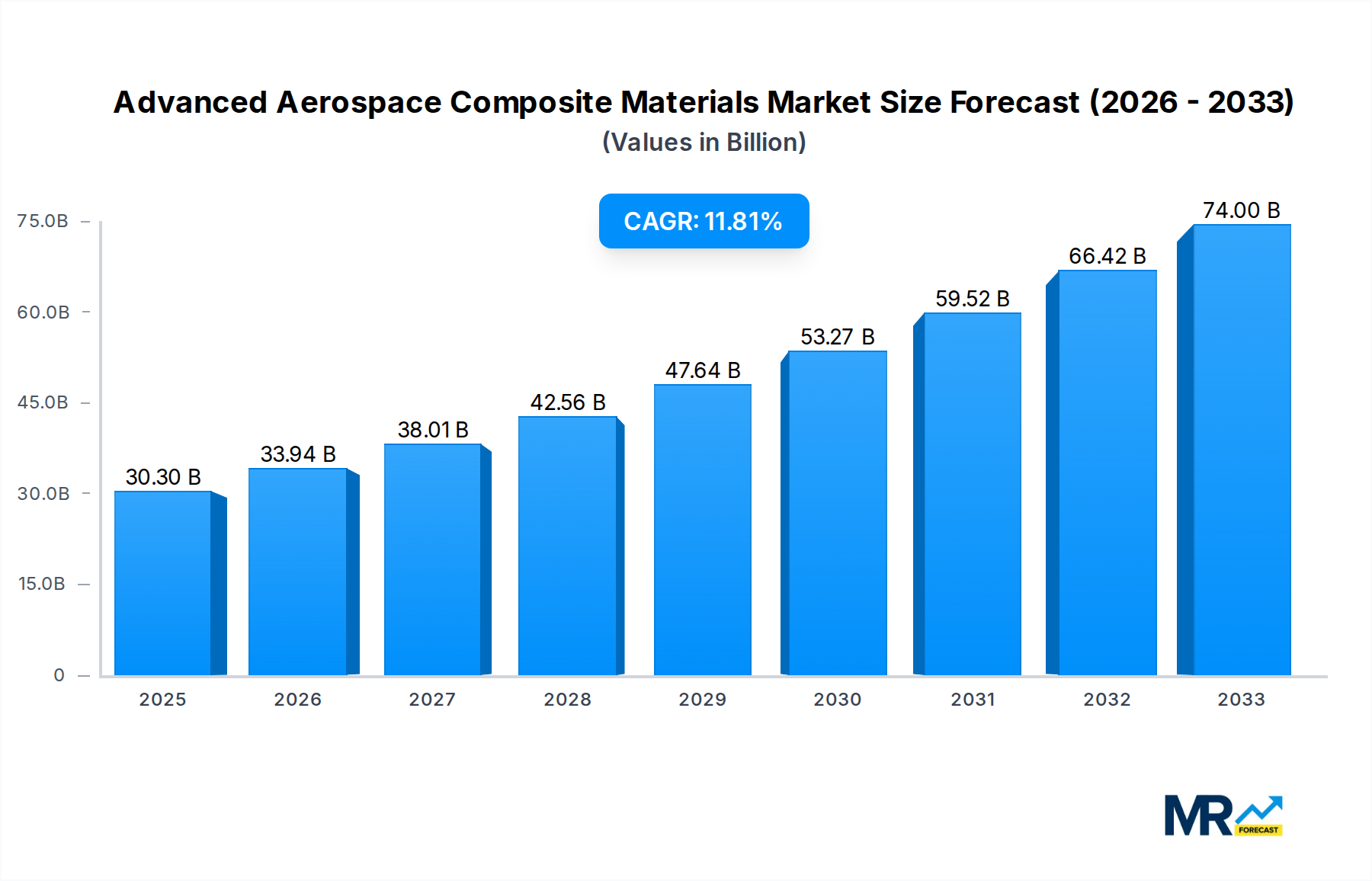

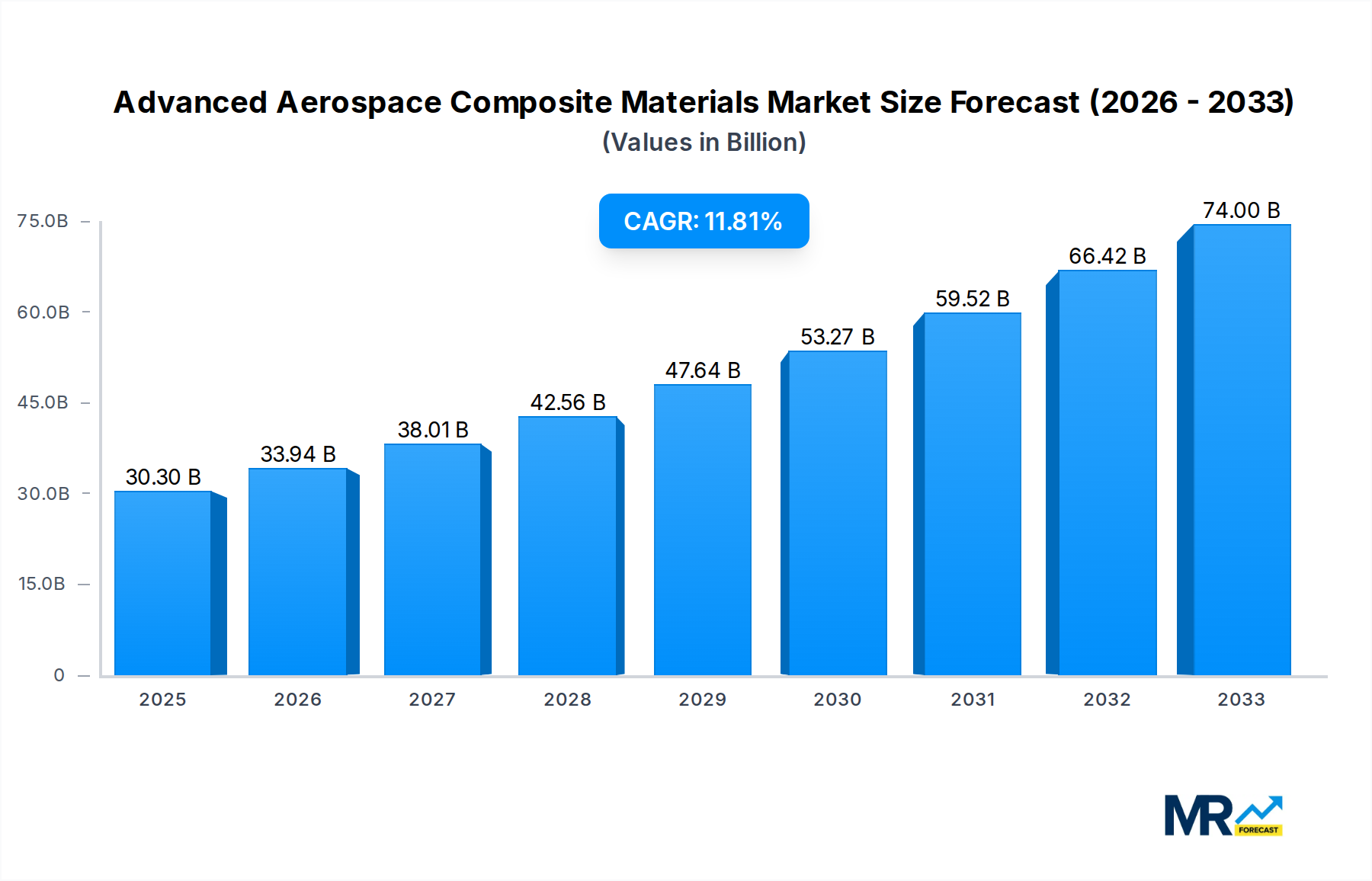

The global market for Advanced Aerospace Composite Materials is poised for significant expansion, driven by an increasing demand for lightweight, high-strength materials in the aerospace industry. With an estimated market size of USD 15,500 million in 2025, the sector is projected to grow at a Compound Annual Growth Rate (CAGR) of 8.5% from 2025 to 2033, reaching approximately USD 29,600 million by the end of the forecast period. This robust growth is largely fueled by the continuous drive for fuel efficiency, reduced emissions, and enhanced performance in aircraft and spacecraft. The inherent advantages of composite materials, such as superior strength-to-weight ratios, corrosion resistance, and design flexibility, make them indispensable for modern aerospace applications, from commercial airliners to advanced defense systems and burgeoning space exploration initiatives.

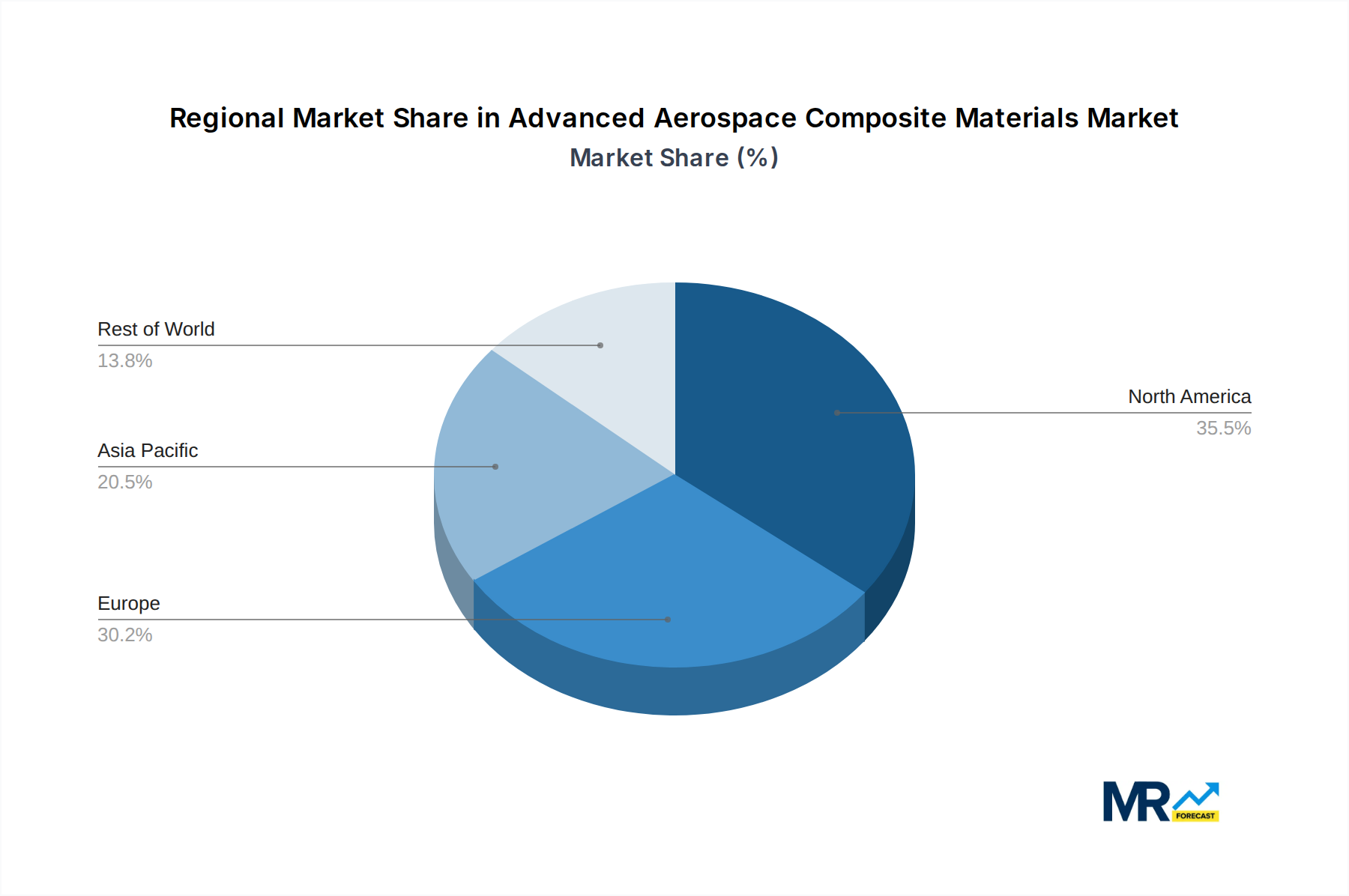

The market is characterized by a dynamic interplay of technological advancements and evolving application needs. Polymer Matrix Composites currently dominate the landscape due to their versatility and cost-effectiveness, finding extensive use in aircraft structures. However, Metal Matrix Composites and Ceramic Matrix Composites are gaining traction, particularly for high-temperature applications in engines and critical structural components where extreme performance is paramount. Key players like Toray Advanced Composites, Hexcel, and Solvay are at the forefront of innovation, investing heavily in research and development to create next-generation materials. Geographically, North America and Europe represent mature markets with a substantial installed base of aircraft, while the Asia Pacific region is emerging as a high-growth area, propelled by increasing aircraft production and a growing defense sector. Despite the positive outlook, supply chain complexities and the high cost of raw materials and manufacturing processes present ongoing challenges that the industry is actively working to overcome.

The advanced aerospace composite materials market is poised for substantial expansion, driven by an insatiable demand for lighter, stronger, and more fuel-efficient aircraft and spacecraft. Our analysis, spanning from 2019 to 2033, with a base year of 2025, reveals a dynamic landscape shaped by continuous innovation and evolving industry needs. During the historical period of 2019-2024, the market witnessed steady growth, fueled by the increasing adoption of composites in commercial aviation and defense sectors. The estimated year of 2025 stands as a pivotal point, projecting a market value in the tens of billions of dollars, with the forecast period of 2025-2033 anticipating an accelerated growth trajectory. Polymer Matrix Composites (PMCs) currently dominate the market, owing to their versatility, cost-effectiveness, and proven track record in aerospace applications. However, Metal Matrix Composites (MMCs) and Ceramic Matrix Composites (CMCs) are gaining traction, particularly in high-temperature applications and structural components where extreme performance is paramount. The burgeoning space exploration sector, coupled with the development of next-generation aircraft like eVTOLs and hypersonic vehicles, is creating new avenues for material innovation. Industry developments are heavily focused on enhancing material properties such as fracture toughness, fatigue resistance, and impact survivability, while simultaneously addressing challenges related to manufacturing scalability and end-of-life recycling. The push towards sustainable aviation is also influencing material selection, with an increasing emphasis on recyclable and bio-based composites. Key market insights indicate that the integration of advanced manufacturing techniques, such as additive manufacturing and automated fiber placement, will be crucial for unlocking the full potential of these materials. The competitive landscape is characterized by a blend of established aerospace giants and agile, specialized composite manufacturers, all striving to secure a share of this rapidly expanding market. The overall sentiment within the industry is one of optimistic anticipation, as advanced aerospace composite materials continue to redefine the boundaries of what is possible in aerospace engineering. The market's growth is not merely incremental but transformative, promising significant leaps in performance, efficiency, and sustainability for the aerospace sector.

The advanced aerospace composite materials market is experiencing robust growth, propelled by a confluence of critical factors that are fundamentally reshaping the aerospace industry. Foremost among these is the unrelenting pursuit of enhanced fuel efficiency. As fuel costs remain a significant operational expense for airlines and a crucial consideration for space missions, the inherent lightweight nature of composites offers a compelling solution. Replacing heavier metallic components with advanced composite structures can lead to substantial weight reductions, directly translating into lower fuel consumption and reduced emissions. This economic and environmental imperative is a powerful driver for increased composite adoption across all segments of the aerospace sector. Furthermore, the continuous evolution of aircraft and spacecraft designs demands materials that can meet increasingly stringent performance requirements. Composites excel in providing superior strength-to-weight ratios, exceptional stiffness, and excellent fatigue resistance, enabling the creation of more aerodynamic and structurally robust vehicles. This allows for the development of larger aircraft, faster spacecraft, and more agile aerial vehicles capable of withstanding extreme operational conditions. The growing emphasis on innovation within the aerospace industry, spurred by advancements in computational modeling, manufacturing technologies, and material science, also plays a vital role. Researchers and engineers are consistently pushing the envelope to develop new composite formulations and architectures that offer even better performance characteristics, opening up new application possibilities and further fueling market expansion.

Despite the optimistic outlook, the advanced aerospace composite materials market faces several significant challenges and restraints that could temper its growth trajectory. A primary concern is the high cost of raw materials and manufacturing processes. Advanced composite materials, particularly those incorporating high-performance fibers like carbon or ceramic, can be considerably more expensive than traditional metallic alloys. The intricate manufacturing processes involved, often requiring specialized equipment and highly skilled labor, further contribute to elevated production costs. This can pose a barrier to widespread adoption, especially for cost-sensitive applications or emerging markets. Another critical challenge revolves around repair and maintenance. Unlike metals, composite structures often require specialized techniques and expertise for repair, which can be more time-consuming and costly. The development of standardized, efficient, and cost-effective repair methodologies remains an ongoing area of research and development. Material characterization and certification also present hurdles. Ensuring the long-term durability, reliability, and structural integrity of composite components under various environmental conditions and operational stresses requires extensive testing and rigorous certification processes. This can lead to extended development cycles and add to project costs. Furthermore, recycling and end-of-life management of composite materials present an environmental challenge. While research into effective recycling methods is progressing, the current infrastructure and technologies for large-scale composite recycling are still developing, raising concerns about waste management and sustainability. Finally, availability of skilled workforce is a constraint, as specialized knowledge is required for the design, manufacturing, and maintenance of composite structures.

The Aircraft segment within the Advanced Aerospace Composite Materials market is projected to dominate in terms of market share and growth over the study period of 2019-2033, with a strong emphasis on the Polymer Matrix Composites (PMCs) type. This dominance is particularly evident in regions with established and expanding aerospace manufacturing hubs, such as North America and Europe.

North America (particularly the United States) is expected to remain a leading region due to its robust aerospace industry, encompassing major aircraft manufacturers like Boeing and Lockheed Martin, as well as a significant presence of Tier-1 suppliers and research institutions. The region's commitment to defense spending and the continuous development of new commercial aircraft programs, including advancements in narrow-body and wide-body jets, directly translates to a substantial demand for lightweight and high-performance composite materials. The application of PMCs, such as carbon fiber reinforced polymers (CFRPs), in primary and secondary aircraft structures – including fuselages, wings, empennages, and interior components – is well-established and continuously expanding. The estimated market value for PMCs in the Aircraft segment in North America alone is expected to reach billions of dollars by 2025 and grow significantly through 2033.

Europe, with its strong aerospace manufacturing base, including companies like Airbus and Dassault Aviation, also plays a pivotal role. The region's emphasis on sustainable aviation and the development of fuel-efficient commercial aircraft further bolsters the demand for advanced composites. Similar to North America, PMCs are the cornerstone of composite usage in European aircraft manufacturing. The region is also a hub for material innovation and research, contributing to the advancement of PMC technologies and their applications.

The Aircraft segment's dominance stems from several factors:

While Metal Matrix Composites (MMCs) and Ceramic Matrix Composites (CMCs) are finding niche applications in demanding areas like engine components and high-temperature structures, their market penetration in terms of overall volume and value within the aerospace sector is still secondary to PMCs. The Space segment is also a significant contributor, with composites crucial for satellites, launch vehicles, and spacecraft due to their lightweight and high-strength properties. However, the sheer volume of aircraft production globally ensures that the Aircraft segment, driven by PMCs, will remain the largest and most influential segment within the advanced aerospace composite materials market for the foreseeable future. The total market value for these segments, across all regions, is projected to be in the tens of billions of dollars.

The advanced aerospace composite materials industry is fueled by several potent growth catalysts. The increasing global demand for air travel, especially in emerging economies, directly translates into a need for more aircraft, driving the adoption of lightweight composite structures. Furthermore, the relentless push for fuel efficiency and reduced emissions, mandated by environmental regulations and consumer preference, makes composites an indispensable material choice. The ongoing advancements in material science and manufacturing technologies are also crucial, leading to the development of composites with enhanced properties and more cost-effective production methods. Finally, the expansion of space exploration initiatives and the development of next-generation aerospace vehicles, such as hypersonic aircraft and reusable launch systems, create new and demanding applications for high-performance composites.

This report offers an exhaustive examination of the advanced aerospace composite materials market, providing deep insights into its multifaceted landscape. Our comprehensive coverage extends from the historical performance during 2019-2024 to projections through 2033, with a foundational analysis based on the 2025 base and estimated year. We delve into the intricate trends shaping the market, the compelling driving forces that propel its growth, and the significant challenges and restraints that necessitate strategic navigation. The report meticulously analyzes key regions and dominant segments, offering a detailed understanding of market dynamics. Furthermore, it highlights the critical growth catalysts that are accelerating industry expansion and profiles the leading players and their strategic initiatives. Through this extensive analysis, stakeholders will gain a profound understanding of the market's current state and future trajectory, enabling informed decision-making and strategic planning in this vital sector of the aerospace industry.

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 12% from 2020-2034 |

| Segmentation |

|

Note*: In applicable scenarios

Primary Research

Secondary Research

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence

The projected CAGR is approximately 12%.

Key companies in the market include ACP Composites, Advanced Composite Materials, Inc, Advanced Custom Mfg, Arris Composites, Collins Aerospace, Hexcel, Mitsubishi Rayon, Northrop Grumman, Owens Corning, Park, Reliant Worldwide Plastics, SGL Group, Solvay, Teijin, Toray Advanced Composites, .

The market segments include Type, Application.

The market size is estimated to be USD XXX N/A as of 2022.

N/A

N/A

N/A

N/A

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3480.00, USD 5220.00, and USD 6960.00 respectively.

The market size is provided in terms of value, measured in N/A and volume, measured in K.

Yes, the market keyword associated with the report is "Advanced Aerospace Composite Materials," which aids in identifying and referencing the specific market segment covered.

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

To stay informed about further developments, trends, and reports in the Advanced Aerospace Composite Materials, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.