1. What is the projected Compound Annual Growth Rate (CAGR) of the 3D Television?

The projected CAGR is approximately XX%.

MR Forecast provides premium market intelligence on deep technologies that can cause a high level of disruption in the market within the next few years. When it comes to doing market viability analyses for technologies at very early phases of development, MR Forecast is second to none. What sets us apart is our set of market estimates based on secondary research data, which in turn gets validated through primary research by key companies in the target market and other stakeholders. It only covers technologies pertaining to Healthcare, IT, big data analysis, block chain technology, Artificial Intelligence (AI), Machine Learning (ML), Internet of Things (IoT), Energy & Power, Automobile, Agriculture, Electronics, Chemical & Materials, Machinery & Equipment's, Consumer Goods, and many others at MR Forecast. Market: The market section introduces the industry to readers, including an overview, business dynamics, competitive benchmarking, and firms' profiles. This enables readers to make decisions on market entry, expansion, and exit in certain nations, regions, or worldwide. Application: We give painstaking attention to the study of every product and technology, along with its use case and user categories, under our research solutions. From here on, the process delivers accurate market estimates and forecasts apart from the best and most meaningful insights.

Products generically come under this phrase and may imply any number of goods, components, materials, technology, or any combination thereof. Any business that wants to push an innovative agenda needs data on product definitions, pricing analysis, benchmarking and roadmaps on technology, demand analysis, and patents. Our research papers contain all that and much more in a depth that makes them incredibly actionable. Products broadly encompass a wide range of goods, components, materials, technologies, or any combination thereof. For businesses aiming to advance an innovative agenda, access to comprehensive data on product definitions, pricing analysis, benchmarking, technological roadmaps, demand analysis, and patents is essential. Our research papers provide in-depth insights into these areas and more, equipping organizations with actionable information that can drive strategic decision-making and enhance competitive positioning in the market.

3D Television

3D Television3D Television by Type (Non-glass Free, Glass-Free, World 3D Television Production ), by Application (Household, Commercial, World 3D Television Production ), by North America (United States, Canada, Mexico), by South America (Brazil, Argentina, Rest of South America), by Europe (United Kingdom, Germany, France, Italy, Spain, Russia, Benelux, Nordics, Rest of Europe), by Middle East & Africa (Turkey, Israel, GCC, North Africa, South Africa, Rest of Middle East & Africa), by Asia Pacific (China, India, Japan, South Korea, ASEAN, Oceania, Rest of Asia Pacific) Forecast 2025-2033

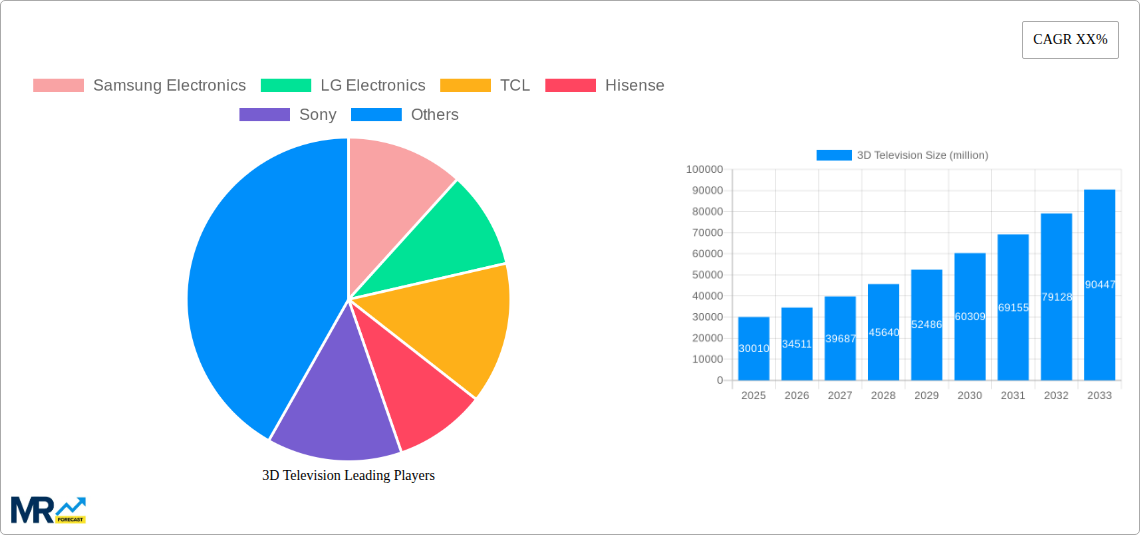

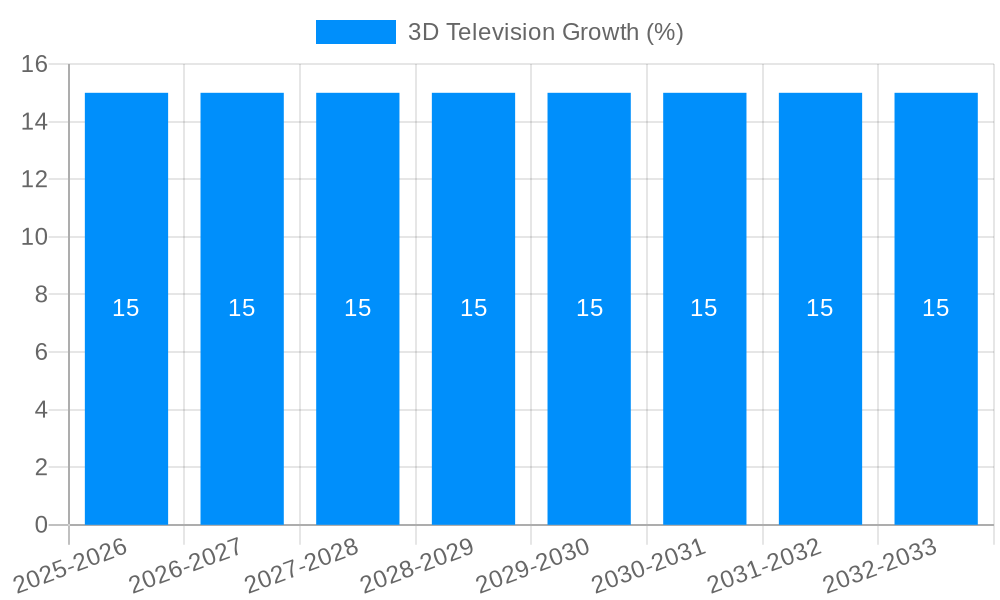

The global 3D television market is poised for significant growth, with a projected market size of $30,010 million by 2025 and an impressive Compound Annual Growth Rate (CAGR) of approximately 15% during the forecast period of 2025-2033. This expansion is primarily fueled by advancements in display technologies, particularly the increasing prevalence of glass-free 3D televisions, which eliminate the need for cumbersome eyewear and offer a more immersive viewing experience. The shift towards enhanced home entertainment, coupled with growing consumer interest in unique visual experiences, acts as a major catalyst. Furthermore, the adoption of 3D televisions in commercial applications, such as advertising, simulations, and educational institutions, is expected to contribute substantially to market penetration. Key players like Samsung Electronics, LG Electronics, and Sony are actively investing in research and development to innovate and capture market share. The market's trajectory indicates a strong recovery and renewed interest in 3D viewing technology, driven by its ability to deliver a deeper, more engaging content consumption.

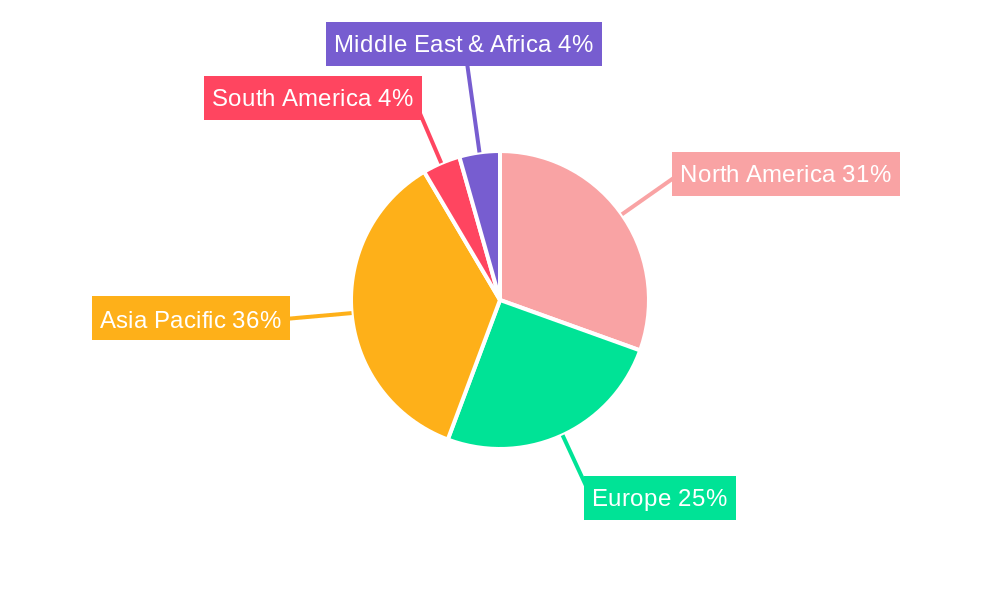

The market segmentation reveals a dynamic landscape with distinct growth opportunities. The "Glass-Free" segment is anticipated to be a primary growth driver, addressing past limitations of 3D technology and appealing to a broader consumer base. In terms of application, both household and commercial sectors are expected to see substantial uptake. North America and Asia Pacific are projected to lead the market, owing to high disposable incomes, a strong consumer appetite for cutting-edge technology, and the presence of major manufacturing hubs. However, challenges such as content availability and the perceived cost premium of 3D televisions, especially in the earlier years, could act as restraints. Despite these hurdles, the increasing availability of 3D content across various platforms and the ongoing technological refinements are expected to overcome these limitations, solidifying the 3D television market's upward trend. The study period from 2019 to 2033, with a base year of 2025, highlights a robust recovery and sustained expansion for this evolving technology.

This comprehensive report offers an in-depth analysis of the global 3D television market, charting its trajectory from 2019 to 2033. With 2025 designated as the base and estimated year, the study meticulously examines the historical performance (2019-2024) and provides robust forecasts for the future (2025-2033). The report delves into the intricate landscape of 3D television, exploring its technological advancements, market dynamics, and the evolving consumer appetite for immersive viewing experiences. It highlights the interplay between innovative companies and the segmented market, ultimately aiming to equip stakeholders with actionable intelligence for strategic decision-making in this dynamic sector.

The 3D television market is experiencing a nuanced evolution, driven by a persistent desire for more engaging and lifelike entertainment. While initial widespread adoption faced hurdles, the underlying appeal of three-dimensional visuals continues to fuel innovation and market segmentation. One of the most significant trends observed is the shift towards Glass-Free 3D television. This technological leap addresses a primary consumer pain point – the discomfort and inconvenience associated with wearing active or passive 3D glasses. Manufacturers are investing heavily in autostereoscopic displays, enabling viewers to perceive depth without any external eyewear. This advancement alone is poised to unlock significant market potential by making 3D viewing more accessible and less intrusive for a broader audience. The World 3D Television Production is projected to see substantial growth in this segment, with an estimated market size in the tens of millions of units annually by 2025, potentially exceeding hundreds of millions by 2033.

Furthermore, the report will dissect the market segmentation based on Application, distinguishing between Household and Commercial use. While household adoption has seen fluctuating demand, commercial applications, particularly in sectors like gaming arcades, educational institutions, and specialized retail displays, are demonstrating consistent interest. The immersive nature of 3D content is particularly valuable in these environments for enhanced engagement and experiential marketing. The integration of 3D capabilities into larger display formats, such as professional signage and simulation systems, is also a growing trend. As content creation for 3D continues to expand, driven by advancements in filmmaking and video game development, the demand for 3D televisions capable of rendering these experiences with fidelity is expected to rise. The report anticipates a considerable investment in research and development, aiming to improve resolution, refresh rates, and color accuracy for 3D displays, thereby enhancing the overall viewing quality and further stimulating market growth. The interplay between technological innovation and content availability will be a critical determinant of the market's overall expansion in the coming years.

Several powerful forces are collectively propelling the 3D television market forward, signaling a resurgence of interest in immersive visual experiences. Foremost among these is the relentless pursuit of technological innovation, particularly the advancement of Glass-Free 3D displays. This breakthrough is significantly reducing barriers to adoption, such as the inconvenience and cost of 3D glasses. As autostereoscopic technology matures and becomes more affordable, it unlocks the potential for widespread integration into mainstream consumer electronics. Coupled with this is the growing availability of compelling 3D content. The gaming industry, in particular, is a significant driver, with an increasing number of titles developed with native 3D support. This not only appeals to a dedicated gaming audience but also spills over into broader consumer interest, creating a demand for televisions capable of rendering these visually rich experiences.

Beyond gaming, advancements in virtual reality (VR) and augmented reality (AR) technologies are indirectly fostering a greater appreciation for depth and immersion in visual media. As consumers become accustomed to the spatial qualities of VR/AR, the desire for similar engaging experiences on their televisions grows. This creates a positive feedback loop, encouraging content creators to produce more 3D films, documentaries, and live event broadcasts. Moreover, the World 3D Television Production is being significantly influenced by a growing understanding of the benefits of 3D in specific commercial applications. Industries such as healthcare (surgical simulations), education (interactive learning modules), and retail (enhanced product visualization) are recognizing the value proposition of 3D displays for improved engagement, training, and customer experience, contributing to a sustained demand. The increasing affordability of 3D television sets, particularly from emerging manufacturers, is also making these immersive technologies more accessible to a wider consumer base, acting as another significant propellant for market expansion.

Despite the promising advancements and driving forces, the 3D television market is not without its considerable challenges and restraints that have historically hampered widespread adoption. A primary impediment remains the "content gap." While the volume of 3D content has been increasing, it still lags significantly behind traditional 2D content in terms of sheer availability and diversity across various genres and platforms. Consumers are often hesitant to invest in 3D technology if they perceive a limited library of compelling programs to watch. Furthermore, the historical perception of 3D television as a gimmick or a technology that causes visual fatigue and discomfort, often associated with early iterations of active shutter glasses, continues to linger. Although modern Glass-Free 3D technology significantly mitigates these issues, overcoming these ingrained negative perceptions requires sustained marketing efforts and consistent delivery of superior viewing experiences.

Another notable restraint is the cost factor. While prices have been decreasing, 3D televisions, especially those with advanced Glass-Free 3D capabilities, often command a premium over their 2D counterparts. This price difference can be a significant deterrent for budget-conscious consumers, particularly in price-sensitive markets. The fragmentation of 3D standards and playback technologies in the past also contributed to consumer confusion and a lack of universal compatibility, although this has somewhat diminished with the maturation of the technology. For Commercial applications, the initial investment in 3D display infrastructure and specialized content creation can also be substantial, limiting its adoption to sectors with a clear and immediate return on investment. Finally, the ongoing dominance and ubiquity of 2D content and display technologies create a powerful inertia that the 3D market must constantly work to overcome.

The global 3D television market is poised for significant growth, with specific regions and market segments expected to lead this expansion. Among the most influential segments driving the World 3D Television Production will be Glass-Free 3D technology. The inherent advantages of this technology – eliminating the need for cumbersome eyewear, reducing potential discomfort, and offering a more seamless viewing experience – directly address the primary pain points that hindered earlier 3D adoption. As manufacturing processes mature and economies of scale are realized, the cost of Glass-Free 3D televisions is expected to become more competitive, making them an attractive option for a broader consumer base. By 2025, the market share of Glass-Free 3D units within the overall World 3D Television Production is projected to be in the tens of millions, with a strong upward trend towards hundreds of millions by 2033.

In terms of regional dominance, Asia Pacific, particularly China, is anticipated to be a key market. This is driven by several factors:

Beyond Asia Pacific, North America will also remain a significant market, driven by early adopters of technology, a strong demand for premium entertainment experiences, and a well-established content ecosystem. The increasing integration of 3D capabilities into gaming consoles and the growing popularity of immersive gaming will further fuel demand in this region. The Household application segment will continue to be the largest driver of the overall market, with advancements in Glass-Free 3D making it more appealing for home entertainment. However, the Commercial segment, particularly in sectors like digital signage, automotive displays, and specialized simulation training, is expected to witness a higher percentage growth rate due to its unique ability to leverage the immersive qualities of 3D for enhanced engagement and effectiveness, contributing to a substantial portion of the World 3D Television Production value chain.

The 3D television industry is poised for sustained growth, propelled by several key catalysts. The most significant is the continuous advancement and increasing affordability of Glass-Free 3D display technology, which directly addresses consumer concerns about comfort and convenience. This innovation is expected to broaden the appeal of 3D viewing significantly. Furthermore, the expanding ecosystem of 3D content, particularly in video gaming and the growing interest from the film and broadcast industries in creating immersive visual narratives, acts as a crucial growth catalyst. As more high-quality 3D content becomes readily available, the demand for 3D televisions capable of rendering these experiences will naturally escalate.

This report offers unparalleled comprehensiveness, providing a detailed market analysis from 2019 to 2033. It dissects the global 3D television landscape, examining key trends, driving forces, and the challenges that have shaped its evolution. With a sharp focus on the transformative impact of Glass-Free 3D technology and its role in boosting World 3D Television Production, the report presents in-depth insights into market segmentation for both Household and Commercial applications. It meticulously details regional market dynamics, identifies growth catalysts, and profiles leading industry players. Stakeholders will gain a strategic advantage through the actionable intelligence provided, enabling informed decision-making in this evolving and promising sector.

| Aspects | Details |

|---|---|

| Study Period | 2019-2033 |

| Base Year | 2024 |

| Estimated Year | 2025 |

| Forecast Period | 2025-2033 |

| Historical Period | 2019-2024 |

| Growth Rate | CAGR of XX% from 2019-2033 |

| Segmentation |

|

Note*: In applicable scenarios

Primary Research

Secondary Research

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence

The projected CAGR is approximately XX%.

Key companies in the market include Samsung Electronics, LG Electronics, TCL, Hisense, Sony, Skyworth, Foxconn (Sharp), Xiaomi, Vizio, Haier, Panasonic, Chonghong, Konka, Videocon Industries.

The market segments include Type, Application.

The market size is estimated to be USD 30010 million as of 2022.

N/A

N/A

N/A

N/A

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4480.00, USD 6720.00, and USD 8960.00 respectively.

The market size is provided in terms of value, measured in million and volume, measured in K.

Yes, the market keyword associated with the report is "3D Television," which aids in identifying and referencing the specific market segment covered.

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

To stay informed about further developments, trends, and reports in the 3D Television, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.